Last week, NZ First leader Winston Peters announced his party’s bold proposal to make KiwiSaver compulsory by supporting employers through tax cuts and raising the contribution rates to 10% of wages.

This was politically significant as it puts savings reform at the centre of our economic policy debate. Peters is correct in stating that New Zealand should become a rich asset-owning country through high domestic savings rather than desperately try to rely on foreign direct investment for growth.

Deeper and more broad-based domestic capital markets provide stability and reduce vulnerability to external shocks.

Unfortunately, compared to other advanced economies, New Zealand is woefully behind in the area of retirement income, domestic savings and use of private funds to increase our investment in assets such as hospitals and infrastructure.

As one of the many young Kiwis who left to go to Australia, I am stunned by our Trans-Tasman neighbour’s financial wealth. It greatly exceeds NZ, even after adjusting for their larger population size.

Australia’s Sovereign Wealth Fund, called The Future Fund, has NZ$350 billion in assets under management.

Meanwhile, their compulsory superannuation system is world-leading. Total accumulated funds are currently NZ$4.6 trillion. It is expected to become the second-largest savings pool in the world by 2050 and is 35 times larger than total KiwiSaver balances. Every Australian has an account. Individually their balance averages 10 times the balance in one of ours.

Astonishingly, around 20% of Kiwis don’t have a KiwiSaver account, and no savings at all.

The Australian scenario would not have been possible without solid and competent political leadership. Former Australian Prime Minister Paul Keating introduced Compulsory Superannuation in 1991 to “reduce the future reliance on the age pension, and over time, give ordinary people a better retirement”. Employer contributions started at a compulsory 3% of wages per year and gradually increased to the 12% where they sit today.

Thanks to compulsory superannuation, Australia is the only country across the OECD expected to have its government old age pension spending decrease from 2.3% of GDP today to 2% of GDP by 2060. By contrast, New Zealanders’ demand on the public purse to fund our pay-as-you-go pension system is projected to rise from 4.9% to 7.7% of GDP by 2060.

There is a common theme that emerges from such comparisons. Countries that create strong compulsory savings systems can reduce the fiscal burden of public pensions and also create pools of capital which they then have available to invest in the country’s national development.

After leaving NZ to study for a master’s degree in Singapore, I was amazed to learn about the city-state’s unorthodox social security and public asset system. Its development is deeply rooted in Singapore’s national savings schemes. The country’s Central Provident Fund requires citizens to save up to 20% of their wages – with another 17% provided by their employers. It currently has NZ$834 billion under management.

Singapore’s Sovereign Wealth Funds manage more than NZ$570 billion through Temasek Holdings and NZ$1.3 trillion through the Government Investment Corporation.

Singapore’s economy is expected to continue remaining the crown jewel of Southeast Asia. It is a capital exporting nation with a current account surplus and net zero debt.

Australia and Singapore have both taken the path of focusing on long-term capital accumulation through use of sovereign wealth funds and compulsory saving schemes. It is time New Zealand follows suit.

Many older Kiwis know about how former Prime Minister Sir Robert Muldoon made an awful mistake by abolishing the compulsory superannuation scheme set up under Norman Kirk in 1974.

Peter’s new savings proposals may mark the new beginning of a bipartisan agenda for NZ’s future public asset development.

Politicians across the spectrum support this transition. Labour’s David Parker said in his valedictorian speech, “[Australia’s] universal work-based savings [is] why those clever Aussies own their banks plus ours, our insurance companies, and much more. It’s why their infrastructure is better, their current account deficit lower, their net international liabilities lower, and their growth rate higher.”

Former National Party Commerce Minister Andrew Bayly also understood the vitality of higher domestic savings. He said, “One largely untapped source is the $109 billion of capital held by KiwiSaver providers… By comparison in Australia, I understand roughly 15% of its $3.8 trillion pension fund industry is invested in alternative assets, such as private equity and infrastructure.”

Now, NZ First has proposed a policy to ensure KiwiSaver becomes a major economic vehicle for our future economy. There are gripes about the fiscal costs of the tax cuts needed to buttress compulsion – including me – but the idea behind the policy is sound.

New Zealand stands at a crossroads. Our low domestic savings rate, combined with our ageing population, poses a long-term fiscal challenge that cannot be ignored.

The late Harvard economist Martin Feldstein’s words still ring true, “The problem with the current system is that retirees’ benefits are financed on a ‘pay-as-you-go’ basis, by taxing concurrent employees. The obvious solution is to shift to a privatised system of pre-funding those benefits through mandatory contributions to individual accounts.”

Many analysts argue that foreign capital can drive investment, but as other nations have now successfully demonstrated, mandatory savings systems supplemented by Sovereign Wealth Funds strengthen not only financial stability but also productivity and national independence.

As far as I know, there are no options to addressing long-term fiscal debt problems for a country like NZ other than by hiking taxes, printing money, defaulting, or cutting public services, or by promoting domestic savings through policies that support schemes like KiwiSaver and our Super Fund.

Which one do you prefer?

Leonard Hong is an economist based in Perth, Australia who has a Master’s degree in International Political Economy from the Nanyang Technological University, Singapore (2024) with the support of the Prime Minister’s Scholarship for Asia. He is a Leadership Network Member of the Asia NZ Foundation.

The assessment of the long-term fiscal position of the United States by Harvard’s Martin Feldstein in 1997 can be applied to most of the developed world today. The ‘pay-as-you-go’ comprehensive social security system that became popular during the early period of the Keynesian Consensus supporting retirement income and healthcare is already unsustainable. Unfortunately, because of the inevitable trend of population ageing, long-term unfunded liabilities – financial obligations from governments to citizens with insufficient funds to cover future projected costs – states will be required to spend far more on healthcare and pension (Goodhart and Pradhan, 2020). In response, various governments pursued a myriad of policy options – and failed so far – to tackle this inevitable trend, including tweaks in the system including increasing the retirement age, indexation of pension and in some cases compulsory private savings towards self-provision.

The crucial question is how to accomplish and resolve this looming problem. Some suggest imposing significant tax increases – such as capital and wealth taxes favoured by the left – or cutting expenditures to an extent that undermines the poorest members of our society without an alternative safety net – which is the libertarian argument. The former option supported by the Green Party will push capital out of the nation, undermine our economy, and at best raise barely any revenue. The latter commonly from the ACT Party does not provide any alternative solutions beyond the status quo. Sentimental push from economists towards “faster productivity growth” is not a solution either (Wilkinson, 2024). In my view, there is no alternative but to prioritise raising domestic savings in New Zealand (NZ) towards supporting economic development. New unorthodox thinking and economic approach is required to resolve the challenges facing New Zealand, beyond the left-right political divide.

In response to the relatively interesting – but flawed – analysis by economist Michael Reddell (2025), this essay seeks to counter the arguments provided on the topic of savings. These were the following main arguments and points from Reddell’s article:

Economic growth has been stagnant and some analysts – including Leonard Hong – have argued for higher domestic savings and Reddell questions their conclusions.

Compulsory savings have not led to significant productivity gains and believes other variables are more important to economic success.

Reddell argues that Australia’s spending on retirement income is still relatively high for the old age pension – which is means-tested – and national savings has not risen to the extent he anticipated and productivity is nowhere near the level of the United States.

Singapore’s national savings did not play as much of a major role in the city-states’ substantial part in their economic success, but rather more from its global competitiveness and low tax settings.

The role of foreign capital and domestic capital on economic growth is still under debate, and Professor Robert MacCulloch’s argument on the “Feldstein-Horioka puzzle” is interesting, but not entirely convincing.

Savings rates are often a response to investment opportunities rather than a cause; therefore, Reddell questions the notion that low domestic savings constrain investment in countries like New Zealand.

I broadly support the idea of mandatory savings – mainly because of its pragmatism and simplicity but also the positive spillover effects as outlined from my previous academic work examining Singapore’s economic model centred around the development of public assets (Hong, 2024). Furthermore, numerically higher domestic savings increase the capital available for investment, which translates to investment in infrastructure, businesses, and innovation, and therefore higher productivity. Other scholars provided potential and feasible alternatives based on mandatory savings across various nations such as Singapore, Chile, Sweden, and Australia (Feldstein, 1998; Kotlikoff and Burns, 2004; Ferguson, 2008; Micklethwait and Wooldridge, 2014; Chia, 2016; Douglas and MacCulloch, 2018).

These are the main reasons why I have repeatedly called for a bipartisan political approach to public asset development, in the form of both supporting our KiwiSaver and our sovereign wealth fund, the NZ Superannuation Fund (NZ SuperFund). New alternative state investment vehicles in the form of institutions such as the Accident Compensation Corporation have also provided social and economic benefit to the NZ public. In contrary to Reddell – and others – I will argue that higher domestic savings, supported by a structured compulsory savings system, is essential for New Zealand’s long-term economic prosperity.

Productivity and the Role of Domestic Savings?

The productivity puzzle in NZ has been widely examined across society. Former NZ Prime Minister John Key suggested the cause of our productivity woes was our “geography” – which is in line with Jared Diamond’s (1997) argument on what mainly distinguishes rich and poor countries. Other scholars including Nobel laureates Acemoglu and Robinson (2012) highlighted the quality of political and economic “institutions”. Huntington and Harrison (2000) provided a cultural perspective on economic development and productivity, especially on aspects of work ethic, meritocracy and openness to innovation. I broadly agree with all these theories – especially the institutional argument – but the point is that the debate on what improves productivity has always a puzzle for scholars and policymakers. I am strongly convinced that higher domestic savings – complemented by overseas investment – boosts economic growth and productivity.

Australia’s Productivity

Reddell mentions that Australia’s compulsory superannuation systems set up by Paul Keating has not led to higher net national savings as anticipated despite the policy mandating private savings for retirement on the public. To his credit, it is true that savings have not been as high, but this is attributed to the ‘substitution’ incentive for Australians to borrow more money under the assumption their wealth will accumulate through their superannuation (Connolly and Kohler, 2004). This was previously examined by many behavioural economists such as Daniel Kahneman (2011) on the ‘present and status quo biases.’ However, by in large, academic studies in Australia show that compulsory superannuation still led to increases in net savings broadly (Ruthbah and Pham, 2020).

Despite the relatively mediocre net savings, Reddell points out that Australia is much wealthier than NZ with a much higher GDP per capita of around USD$20,000 stating, “Australia is, by the way, the most culturally and behaviourally similar country to New Zealand in the world.” (Isn’t the fact that the author of this essay is working in Australia somewhat ironic?). His comparison between Australia and the United States may not fully account for the unique factors that influence their economies, such as the role of the US dollar as the world’s reserve currency. Furthermore, if the United States government followed Martin Feldstein’s advice of “large-scale compulsory saving”, perhaps they would not be in such a dire fiscal situation of US$37 trillion of net government debt – culminated from the unnecessary and costly wars in the Middle East.

In relation to the comparisons with NZ, there are two major variables in my view that distinguish the two countries – iron ore and the superannuation funds sector. The former, we have limited control over – although depending on the agenda of NZ Resources Minister Shane Jones – but the latter, there is greater potential for reform.

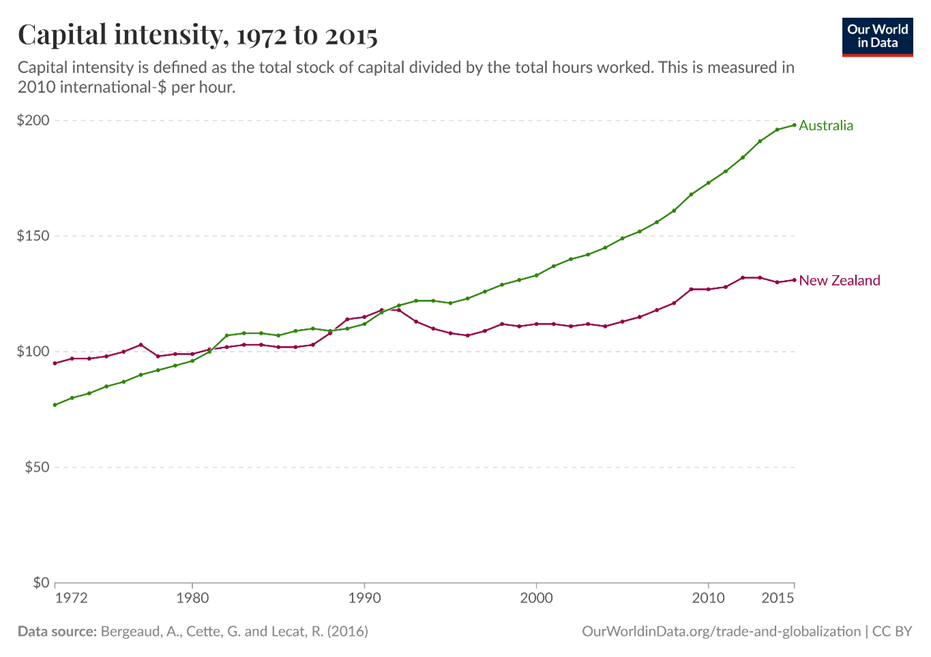

Figure 1: Capital Intensity, 1972 to 2015

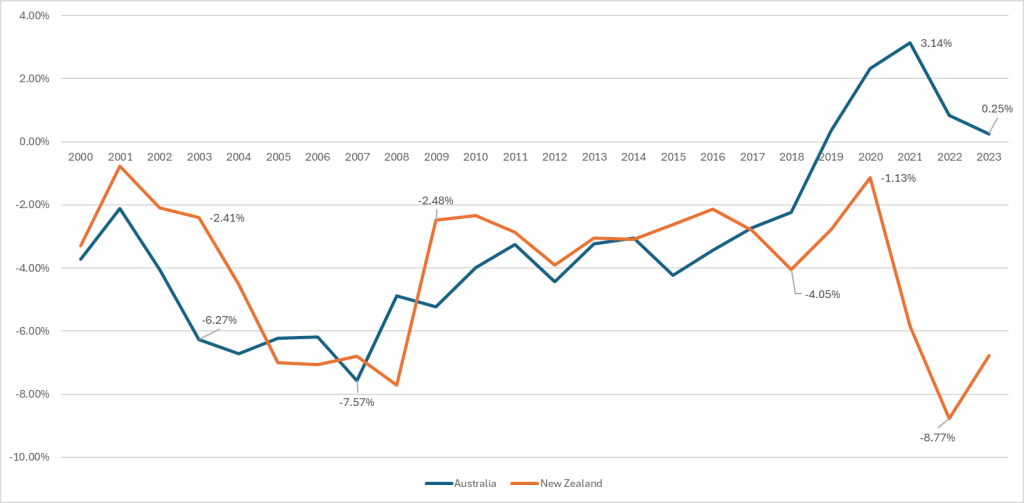

The superannuation system now manages more than AUD$4.1 trillion under management which is the fourth largest savings pool in the world which comprises of 150% of Australia’s GDP – which is expected to become the second largest savings pool by 2050. This is remarkable for the 55th largest nation in the world. This pool of capital translated to rapid increases in capital intensity for the Australian economy. As shown in Figure 1, from World in Data, the specific critical juncture was from 1991, which was when Australian Prime Minister Paul Keating decided to introduce Compulsory Superannuation to “to reduce the future reliance on the age pension, and over time, give ordinary people a better retirement.” (Keating, 2013). He had the foresight and prescience to understand that demographic pressure was inevitable. Therefore, setting up a mandatory savings scheme would allow the system to transfer more from a ‘pay-as-you-go’ system towards a ‘self-provision’ based system. To Keating’s credit, the call on the budget from the old age pension dropped from 5% of GDP in 1991 down to around 1% in 2023. Secondly, in stark contrast to NZ, Australia recently had some periods of current account surpluses starting in 2019 without needing the begging bowl to foreign investors being capital poor. However, as shown by Figure 2, there is not much difference between Australia and NZ with both countries, and I concede that this is probably the weakest point of comparison in my analysis. The differences in economic scale, trade composition, and external sector dynamics significantly influence their respective balance of payments. Although I do consider the historical hypotheticals if Keating’s original plan of raising the compulsory savings rate beyond the 9.5% to 15% was actualised, especially given that Coalition governments have frequently prioritised tax cuts over further superannuation expansion (the Morrison government did eventually raise it to 12%).

Figure 2: Australia vs NZ – Balance of Payments in Proportion to GDP, 1989 to 2023 (World Bank Data)

I am not arguing that in the short-run a current account surplus or deficit is inherently good or bad – in the long run possibly – but it is clear that Keating’s policies led to the structural transformation of Australia’s economy. Despite later Coalition governments pursuing tax cuts over further superannuation expansion, much of the accumulated savings under Keating’s framework were directed toward domestic investment, funding major infrastructure projects such as the Port of Melbourne and Transurban Toll Roads. For higher productivity focusing on capital markets, NZ can only grow by boosting both domestic savings and allowing more foreign capital into the country which will consist of cutting actual red-tape to FDI through supply-side reforms – which Reddell strongly agrees with me – and ramping up domestic savings through KiwiSaver – or other private saving investment vehicles (MacCulloch, 2024). The current National Coalition government’s emphasis has been on attracting overseas investment whilst broadly ignoring the problem of domestic savings so far.

Singapore’s Productivity

Reddell rightly praises Singapore’s economic miracle with the city-state having one of the highest per capita GDP in the world. However, he claimed that “it would be very hard indeed to argue that national savings played any very substantial part in Singapore’s economic emergence.” I believe this perspective overlooks a critical component of Singapore’s economic strategy, which was deeply rooted in their national savings system as a fundamental part of economic policy for current Singaporean politicians (Lee, 2024). Whilst the Central Provident Fund (CPF) was set up in the 1950s, it was an inherent part of the Singapore government’s fiscal strategy. Lee Kuan Yew (2000, p.97) stated he not only maintained the compulsory nature of the system but regularly raised the contribution rates to “avoid placing the burden of the present generation’s welfare costs onto the next generation.” Furthermore, according to Lee (2000, p.102-103), the critical aspect is to ensure bare minimum fiscal pressure on the state to avoid the ‘buffet syndrome’, a fact which Reddell omitted when publishing his article:

Through the CPF system, Singaporeans have access to a comprehensive self-financing social security fund comparable to any old-age pension system or entitlement system in the Western world without transferring the burden to the next generation of workers (Micklethwait and Wooldridge, 2014; Chia, 2016; Douglas and MacCulloch, 2018). The Singaporean government understood the importance that every generation should contribute to their own pension and every individual should save for their own without burdening the state. CPF has a major role on Singapore’s economy – Reddell is incorrect. The whole entire purpose was fiscal discipline which is important for long-term economic growth and macroeconomic stability (Reinhart and Rogoff, 2009).

Secondly, Reddell cites comprehensive data concerning Singapore’s current account position and national savings record in proportion of GDP from the International Monetary Fund. The question from him was the notion that the Singapore government relied on current account deficits in the early period of the 1970s and 1980s for its growth. Indeed, it is true and there is a specific reason. The East Asian Miracle – particularly in Singapore – shows that savings and investment are not separate, but interconnected variables in driving economic development.

Reddell should have considered the extensive work by development economists on the East Asian Miracle, where the initial phase of development focused on attracting foreign capital to acquire the necessary talent, business expertise, and technological spillovers that enabled these countries to build their own capabilities in the long run. This approach, championed by various economists that studied the East Asian developmental state model (Stiglitz, 1996; Chang, 2003; Rodrik, 2015; Haggard, 2018). While these nations initially relied on foreign investment, they eventually became capital-exporting economies after reaching a certain level of development and establishing competitive domestic companies and ‘national champions’. High domestic savings were critical in fostering capital formation for the Four Asian Tigers, which, in turn, led to productive investment and long-term growth.

Figure 3: Singapore Government’s NIRC and Budget Deficits/Surpluses (S$ Millions)

Furthermore, Reddell didn’t mention the importance of sovereign wealth funds for Singapore, but it is relevant to the argument in this essay – it was covered extensively across my postgraduate dissertation. Singapore relies heavily on endowment funds provided by the Government Investment Corporation (GIC) and Temasek Holdings, called Net Investment Returns Contribution (NIRC). For example, in the 2024 Budget, the Singapore government received S$23 billion through the NIRC, comprising 18% of the revenue – 3.4% of GDP. This fiscal mechanism has many benefits since it allows the state to be ‘developmental’ such as public investments in infrastructure, housing, and education, but also tax breaks for new start-ups, capital allowance on depreciable assets, 250% tax deduction on R&D expenses, low corporate tax rate of 17%. The pro-business settings – including tax breaks that Reddell gives a fair bit of credit to Singapore – was possible because of their net zero debt position with massive amount of financial assets – worth US$1.9 trillion owned by the public. As shown in Figure 3 – which is from my dissertation – seven of the ten last government budgets saw the NIRC contribute an overall surplus, despite eight budgets having a primary structural deficit.

Conclusion

In conclusion, I disagree with the premise of the article that was published by Michael Reddell. I fully support Martin Feldstein’s remarks from 1997 that the “obvious solution is to shift to a privatised system of pre-funding those benefits through mandatory contributions to individual accounts.” I do not see another alternative policy approach to tackle this looming macroeconomic problem. The mainstream economic approach currently tinkers around the edges. The status quo – even with the NZ SuperFund – will be fiscally inadequate as highlighted by the NZ Treasury’s Long Term Fiscal Position forecasts. I suggest that moving to a hybrid system like Australia with a means-tested old-age pension would be the next step by incrementally raising the minimum contribution rates to KiwiSaver – either employee or employer – as highlighted by the Retirement Commission (Katz, 2024). Andrew Coleman (2024) recently highlighted the major issue of designing the new system towards “intergenerational neutrality” without harming the younger generation to continue to pay for retirees and at the same time build a nest-egg for their future. This major issue of intergenerational fairness is a very tricky and puzzling problem for transitioning from our current ‘pay-as-you-go’ system towards a social security system based on ‘self-provision.’

Both examples of Australia and Singapore show that high domestic savings matter to a large extent on both macroeconomic stability and economic performance. I also do not see ‘domestic savings’ in a similar way to Reddell that “savings themselves are endogenous.” Savings are not entirely endogenous but can be nudged and supported through policies that incentivise individuals and households towards more private savings and investment. The fact is that NZ has one of the lowest domestic household savings across the developed world is worrisome. Therefore, reversing the trend is critical, not only for our long-term fiscal position but also our economic prospects in the future. We should be attempting to emulate parts of what Australia and Singapore have done, instead of labelling such policy proposals as ‘paternalistic’ or ‘authoritarian’.

Reddell’s statement that “retirement income policy should be approached on its own terms, with a focus on individuals and their own ability to manage retirement,” is a simple classically liberal philosophical position. The only difference from my end is suggesting that people mandatorily save rather than forcefully pay high tax rates! The state already compels the public to pay income tax, and GST, so what is the difference between taxes and being compelled to save money? A high return on private savings is achieved by investing in high-performing investments with compound interest, whereas taxes are simply a means of generating revenue for the state.

NZ is currently discussing the importance of attracting more foreign direct investment. I broadly agree that we need to make it easier for capital from overseas to invest into NZ equities, companies, land, industrial development, housing supply and our chronic infrastructure deficits highlighted by the Infrastructure Commission. However, there is a limit to this strategy as higher concentration of foreign capital also risks financial instability and tends to lead to slower growth than countries that have higher proportion of domestic savings (Prasad et al, 2007; Cavallo et al, 2016). And this idea was partially supported by Reddell who concluded in the latter part of his article stating:

Indeed, higher domestic savings by-in-large would have a positive effect on the current account, put less demand on the NZ dollar, support more exports and allow more Kiwis to accumulate foreign reserves and become a capital exporting nation.

The notion of having more savings on an individual and household level makes sense as a financial buffer and social insurance during times of personal difficulty. The prudent decision is to limit credit card debt and refrain from buying unnecessary items or making “vanity” purchases of luxury goods with credit cards. If every Kiwi behaved and understood finance like Warren Buffett and Charlie Munger, then we would not be having these policy discussions. Unfortunately, most of the NZ public do not have the appetite let alone the long term orientation or foresight to consider making sound financial decisions. If we apply this logic on a macroeconomic level, most of the readers will be able to comprehend as to why a lot of people – including myself – are advocating for mandatory savings. Former NZ Commerce Minister Andrew Bayly was pursuing important policies to kickstart financial education across our school system and I hope new Minister Scott Simpson completes the job. The average balance of NZ$38,000 for KiwiSaver is utterly woeful and nowhere enough to save for retirement – let alone purchasing a house.

I decided to respond in a comprehensive manner with this essay because Reddell is one of the most well-known economic commentators and analysts in NZ, and I have tremendous respect for his work. His compelling research with Dr Don Brash and Dr Bryce Wilkinson for the 2025 Taskforce was very useful with insightful economic suggestions. Anyone interested in economic policy should have a read – as well as his excellent blog. The debate regarding domestic savings is a necessary one, but I am confident that history will prove people such as myself to be correct in the long run.

NZ stands at a crossroads. Our low domestic savings rate, combined with an ageing population, poses a long-term fiscal challenge that cannot be ignored. Some may argue that foreign capital broadly can drive investment, but the examples of Australia and Singapore demonstrate that a comprehensive mandatory savings system not only strengthens financial stability but also boosts productivity and national resilience. In my humble opinion, there is no economic policy alternative to addressing the long-term fiscal debt problem, economic growth and productivity problems besides developing more public assets and boosting domestic savings through policies that support schemes such as KiwiSaver and the NZ SuperFund.

References

Acemoglu, Daron., & Robinson, James. (2012). Why Nations Fail: The Origins of Power, Prosperity, and Poverty. New York: Crown Publishing Group.

Cavallo, Eduardo., Eichengreen, Barry., & Panizza, Ugo. (2016). “Can Countries Rely on Foreign Saving for Investment and Economic Development?” IDB Working Paper No. IDB-WP-718. Retrieved from https://ssrn.com/abstract=2956698

Chang, Ha-Joon. (2003) Kicking Away the Ladder: Development Strategy in Historical Perspective. London: Anthem Press.

Chia, Ngee-Choon. (2016). Singapore Chronicles – Central Provident Fund. Singapore. Straits Time Press.

Feldstein, Martin. (Ed.). (1998). Privatizing Social Security. Chicago: The University of Chicago Press.

Ferguson, Niall. (2008). The Ascent of Money: A Financial History of the World. London: The Penguin Press.

Goodhart, Charles., & Pradhan, Manoj. (2020). The Great Demographic Reversal: Ageing Societies, Waning Inequality and an Inflation Revival. London: Palgrave Macmillan.

Haggard, Stephen. (2018). Developmental States: Elements in the Politics of Development. New York: Cambridge University Press.

Harrison, Lawrence., & Huntington, Samuel. (Ed.). (2000). Culture Matters: How Values Shape Human Societies. New York: Basic Books.

Hong, Leonard. (2024). “Lessons from Singapore on getting the Government’s books in shape without paying more tax.” The New Zealand Herald.

Hong, Leonard. (2024). “Savings and Sovereignty: Comparative Political Economy on Fiscal Discipline and Public Asset Management between Singapore and New Zealand.” Postgraduate Dissertation for NTU.

Kahneman, Daniel. (2011). Thinking, Fast and Slow. New York: Farrar, Straus and Giroux.

Kotlikoff, Laurence., & Burns, Scott. (2004). The Coming Generational Storm: What You Need to Know about America’s Economic Future. Cambridge: MIT Press.

“In recent years it has become evident that the consensus upholding this system is facing increasing pressures, from within and from without… It’s imperative that we act urgently to defend the liberal international order.” — President-Elect Joe Biden in 2017.

The Liberal World Order is one of the most used phrases in international relations scholarship. It’s a repetitive term, but a significant one, considering the fact that it affects everyone around the world. The United States began the Liberal International Order with the end of World War II and the defeat of the Nazis. With Franklin Roosevelt’s vision, the Western superpower set up international institutions and created long sustaining alliances for a greater multilateral and tolerant global society. Without the liberal world order and brilliant American leadership in the likes of Roosevelt, Eisenhower, Kennedy, and Reagan, New Zealand and other allied nations would have not been able to thrive during the Cold War period. Regional and international institutions such as GATT, WTO, IMF, the World Bank, European Union, and NATO provided security and economic cooperation among allied nation-states.

And yet, there are a lot of people in New Zealand that criticise America for its role as the leader of the world. In fact, many of them want to see its role reduced substantially. I agree with that statement somewhat, I’ve been very critical of their nonsensically hawkish interference in the Middle East, its naive attempts at forcefully spreading liberal democracy around the world. Its eastward expansion of NATO and the EU was also a great mistake that resulted in the military retaliation of the Russians. America’s neoconservatives and liberal hawks that were fundamentalist on the ‘end of history’ ultimately created all this mayhem.

However, if they mean America’s leadership getting entirely compromised and allowing authoritarian governments to enter that space – such as Communist China – then my answer is an absolute ‘no’. As President-Elect Biden noted, “it’s imperative that we act urgently to defend the liberal international order”. The Thucydides’ Trap is incoming at this stage in history and the US-China geopolitical contest will be the defining historical turning point for global liberal democracy. As John Mearsheimer noted before, this security competition will continue even under the Biden Administration and beyond.

So what is the point of this post? My message to New Zealanders in this blog is simple, America matters for the western world and in fact democracy itself. They have to win, and it is imperative that they do. I say this, despite knowing America’s complicated history.

In many ways, America is somewhat a hypocritical concept – it started as the first constitutional republic against the British monarchy. It set out laws for equal opportunity…but for only white men, and simultaneously set out a brilliant Federal system of power by instituting checks and balances. Constitutional amendments were made for free speech and inquiry… but also allowed slavery. It also intervened in smaller nations and participated as a colonial power during the Imperial era. Then slavery was banned under Abraham Lincoln, and racial equality was not legally achieved until the 1960s, under Lyndon Johnson’s Civil Rights Act and Voting Rights Act… and also escalated the Vietnam War. They defeated the Soviets and ended Communist authoritarianism with the Berlin Wall falling. The American Pentagon stupidly intervened in Iraq and Afghanistan after 9/11. Then elected the first African American President, Barack Obama (whom I personally admire). Then the recent events that happened in Washington is another example of historical irony at work. It is clear that President Trump and his cronies led the world to a more chaotic, less democratic and hyper-partisan society. America as the beacon of freedom or just arrogance? In short, both. The American experiment is indeed full of both hypocrisies and social progress. Even today, many social science scholars such as Cornel West suggest that the nation has not lived up to its ideals, for instance, the inadequacy of equal opportunity for all. These are all empirically and historically accurate.

However, what separates America in contrast to other countries around the world is that it’s the first serious societal experiment in human history. The United States is like the ‘Republic City’ in the television cartoon, The Legend of Korra. The nation is defined entirely by civic values rather than on race, ethnicity, culture, background, or creed. You become American by embracing its liberal democratic values, its identity based on its historical strife against the British monarchy, its constitutional values, and individual liberty. It’s a nation created out of migration and a sociological result as a historical derivative of European enlightenment.

Diversity matters to many Americans, but what is unique is the tolerance towards others, the ability to fight for freedom around the world. Liberalism is the key symbol of America and that’s the beauty of it. As Francis Fukuyama mentioned in his column last year:

Liberalism was simply a pragmatic tool for resolving conflicts in diverse societies, one that sought to lower the temperature of politics by taking questions of final ends off the table and moving them into the sphere of private life. This remains one of its most important selling points today.

Indeed, liberalism allows for diversity. Other liberal democracies like New Zealand, Australia, the EU etc, need the United States for the sake of soft power. America as a symbol is still a liberal democracy with its political institutions stable. Even though there has been a rise of neopatrimonialism in their political process which has undermined the state to be held accountable to its people. Rent-seeking behaviour among some plutocrats has undermined Americans’ trust towards its politicians and state institutions. We witnessed such examples through the 2008 global financial crisis and the federal government’s response to Covid-19.

Historically the United States has been a success story so far, but it needs to sort its own domestic affairs out. We already have incoming challenges such as AI, automation, climate change and geopolitical tensions, that will cause more drastic disruption to the world. But those challenges cannot be solved if America’s civil society and political polarisation continues. The world needs America to be the genuine liberal captain it was when it led the liberal international order after WWII. As liberals, we have to preserve our values of freedom, justice, equality and liberal democracy in the face of rising China and revival of national populism. We cannot continue this trend of a global ‘democratic recession’.

As a liberal democrat – in the classical sense – I’m hoping that the new Biden Administration would bring some common sense back in the White House. The Electoral College just confirmed Joe Biden’s victory in the 2020 US Presidential election – He will be the next President. It’s a sigh of relief for many (including me) after President Trump’s tumultuous, chaotic, and unpredictable 4-year term. Although I criticised the Democrats in a previous post, that doesn’t mean I don’t want to Biden Administration to do well.

They have a huge task ahead. The Liberal World Order and America matter to all of us.

It is clear that so far both sides of politics have failed to address the ongoing problem of housing unaffordability. It’s been more than five years since the leaders of both major political parties acknowledged the housing crisis. Now, it’s 2020 and housing has become even more unaffordable with prices increasing by 19.8% with the median price of $725,000. Despite Covid-19 ‘supposedly’ cutting aggregate demand, how on earth did this phenomenon occur? It’s caused by multifaceted reasons which I will explore by sections:

Migration and Foreign Investment – Not the core factor

There is a fundamental misunderstanding of the housing crisis. Many New Zealanders believe that migration flow and population growth are the core reasons for growing housing prices. On face value, that is correct. Growing demography does mean growing housing demand. However, this would not be a problem if the growing demand is matched by a growing supply. Anti-developmental sentiments from central and local government artificially restricted land supply and housing development. In fact, migration is critical to our prosperity (especially those that are young with high skills and educated). The housing crisis is a supply problem rather than a demand problem.

Foreign investment and speculation are also conjectured by many in the public as the cause of housing hyperinflation. This is also incorrect. Much of the housing inflation is caused by local New Zealanders purchasing property and spurring up demand. In fact, only 3% of housing purchases were from foreigners between January and February 2016. Whilst further should be done to see the extent of the speculation over a long period of time, such evidence suggests that the effects are minimal.

Housing Supply < Housing Demand = Price increase

The core reason for the housing crisis is simply because growth in demand has exceeded growth in supply. One of the core fundamental economic principles is supply and demand. Housing has become extremely expensive because we have not built enough housing in New Zealand to address growing demand. In 1974, New Zealand was building 34,400 annually. However, because of the oil crisis in the 1980s and our unsustainable fiscal position, new annual dwellings dropped to 15,000 in that era. The current government have made some changes that resulted in a growing supply with 24,100 houses built in 2019. We need to note that the population in NZ was 3 million and now just over 5 million. Population growth and demographic ageing do mean that there is consequently excess demand. My research paper released in the new few months will explore this.

In the last three years, the current government has attempted to curb aggregate demand and expand supply with Kiwibuild. There has been progress with better infrastructure financing to aid local councils and important changes to the National Policy Statement on Urban Development. This removes unnecessary regulations that so far prevented intensification. On the negative side, the government passed new laws such as the ban of foreign buyers (with the exception of Singaporeans and Australians), extended the bright-line test to 5 years, amended the Overseas Investment Act, and tried to legislate a new capital gains tax. For supply, Kiwibuild was a colossal failure with only 548 houses being built. There has been some definite progression in contrast to the previous government, but also multiple failures.

The Reserve Bank’s Impact in Housing

The global Covid-19 pandemic has forced many central banks around the world towards expansionary monetary policies. The Reserve Bank of New Zealand (RBNZ) is no exception. Under Adrian Orr, the bank committed to $100 billion of quantitative easing and also cut the OCR rates to 0.25%. This is unprecedented regarding the scale of the policy (a third of our GDP). These two decisions alone will raise the returns from investment in housing and increase pressure on house prices. Low-interest rates mean cheaper mortgages incentivise investors and consumers into the housing market. These policies led to higher equity and asset prices. Although, some of their policies are completely understandable considering Covid-19’s impact on employment and the economy. However, regardless of the pandemic, this level of quantitative easing is unprecedented. Saying this, it is undeniable that RBNZ’s policies have made a significant contribution to greater aggregate housing demand.

Lacking incentives for local government

One of the key reasons for the current state of the housing market is because of poor local government incentives. Much of the infrastructure financing is imposed on the local councils, meanwhile, the revenue is centralised to government officials in Wellington. The current system gives far too much political leverage for those in central government, rather than allowing local officials to make important decisions on urban development. There are questions on whether the centralisation of such power into a larger government institution such as the Super City of Auckland Council led to efficient outcomes.

New Zealand’s current system does not incentivise local councils to grow but slows down development. Local government officials don’t want more people in their area, because that means greater demand for water, schools, housing, local parks, and other public infrastructure to accommodate growing demand. Meanwhile, the central government does not allocate funds based on proportionality, but rather on ‘democratic means’ of serving respective electorates and other political factors. The finance gets imposed on the councils with growing demand, but not given the finance from the central government. For example, more than 40% of newly arrived migrants settle in Auckland rather than other regions that need people. Auckland Council currently has growing debt and it wants to tackle that problem rather than expand urban development outwards. The same applies to many other local councils across the country. Without sufficient revenue provided by the central government, why would they want to grow? They would not want to free enough brownfield nor greenfield areas for housing development because all the costs are imposed on them.

To address these problems for New Zealand’s local governments, I advocate for ‘localism’ as it provides greater political leverage to local governments and decentralises decision-making. Countries such as Germany and Switzerland follow this form of local administration. In the United States, Houston in Texas also has a very decentralised governance system. At the federal level, they simply set out basic regulatory frameworks and for the implementation of policies, they leave it to local councils.

For instance, let’s take the case of Essen and Dortmund – the two regions have a competitive and cooperative governance arrangement. The reason is that the tax revenue created is tied to the number of residents in their area. It is essentially a form of a ‘means-test’ requirement for local officials to get their revenue. Because of the incentives to have more residents in their area, the government understands that they need to have good institutions, a clean and green environment, affordable housing and sound public infrastructure. the two cities needed to allow enough land supply available in their area to deal with growing demand. If certain residents leave their regions, they lose tax revenue consequently. In essence, a solid local structure that incentivises competition. Currently, both Essen and Dortmund have affordable housing. Since the 1980s, prices have only risen by 10% in the last 30 years. Simply by changing the tax incentives with a decentralised local government system, it leads to more optimal urban development that matches growing demand with sufficient supply.

Germany’s economic system is a strongly Keynesian-oriented system with high levels of taxation, a generous welfare system and a decentralised form of governance. Localism is neither a right nor left policy subscription, but an example that has worked in these areas. Experimentation in New Zealand wouldn’t be a bad start and we can learn from these international examples. I am not advocating for the de-amalgamation of Auckland Council, but rather changing the tax structure so that local councils get the incentives. Decentralisation of command towards district councils, for instance, is a potential alternative without removing the Super City’s institutional arrangement. As stated by renowned American investor Charlie Munger stated,

“I think I’ve been in the top 5 per cent of my age cohort all my life in understanding the power of incentives, and all my life I’ve underestimated it.”

Basic economics is about incentives. Incentivising local government to grow public infrastructure and push for housing development requires the officials to have the incentives. This will help the expansion of supply – both housing and infrastructure.

Conclusion

These are the many reasons why housing is unaffordable. Housing is an extremely complicated subject but this post attempted to explore fundamental factors as to why house prices increased in New Zealand despite housing demand ‘supposedly’ very low under the current era of Covid-19. It is clear that housing supply has not expanded fast enough to accommodate growing demand. RBNZ’s policies have exacerbated the problem fueling investment into the property market, and the current set-up of local governments prevents them from wanting to expand development because most of the costs are imposed on them, rather than the central government.

It is imperative for the new Labour government to push for the expansion of housing and land supply rather than continuing to just curb growing housing demand.

It was in 2016 when I first watched and observed the outcomes of a US Presidential election. I detested Hillary Clinton back then – I still do now – but I didn’t expect Donald Trump to win, yet he did. Following on from Brexit, this was another shock to the American Establishment and symbolic of the rise of national populism. Back then, I was a hardcore social democrat, and I was disappointed and sad that America lost the opportunity to elect a 21st-century version of Franklin Delano Roosevelt, Bernie Sanders. I consider myself a moderate centrist today, but that’ll be discussed in another blog post.

The world witnessed four years of a Republican White House and boy it was a period of pure entertainment and a complete mess. Now it’s 2020 and the Democrats have selected an old, weak and out of touch politician – Joe Biden – as their candidate. Throughout 2019 and 2020, I felt that the liberal establishment learnt absolutely nothing from 2016, and it shows. Despite the polls suggesting that it will be a landslide for Biden, they were completely wrong. The US election is still an ongoing dispute and it is still too close to call for either of the candidates. The rustbelt states such as Michigan, Pennsylvania, Wisconsin have moved back towards the Democrats, but only because of Trump’s incompetency regarding Covid-19. They have lost seats in the House and also the Senate is in the strong hands of the Republicans. If Trump didn’t have to deal with Covid-19, the President may have indeed had a landslide victory against Biden.

The question is why did the Democrats perform so poorly despite the expectation? The Americans have faced a period of complete chaotic governance by the Trump Administration but many still voted for him. The fact of the matter is that many Americans are sick and tired of political correctness, wokeness, and identity politics. And this is taking into account Trump’s disastrous policies. Many people including Sam Harris, Andrew Sullivan, Eric Weinstein, Paul Graham, and Niall Ferguson and others have previously warned centre-left people about this form of politics.

One prominent scholar that understood this problem for the Democrats was Stanford’s Francis Fukuyama. He covered this topic of identity politics in his book, ‘Identity: The Demand for Dignity and the Politics of Resentment’. The core thesis of the book surrounds the concept of ‘thymos’. Fukuyama described it as “part of the soul that craves recognition or dignity.” Fukuyama says that the thymos of blue-collar, white Americans was not recognised by the political and economic establishment in America in 2016. The craving of status and recognition is not a new phenomenon, which is evident from the cultural movements of the 1960s – the civil rights movement of African Americans, Women, LGBT, and even the environmental movement. These movements were legitimate and necessary but extended far beyond its necessity up until 2016. Because that sense of dignity was ignored by the Democrats, but recognised by Trump in the form of nationalist sentiment and protectionist economic policies, they switched to him. Even with his racial rhetoric, many didn’t care, they were just glad someone wanted to talk about the negative externalities caused by globalisation. The former core of the Democratic Party was on socioeconomic issues, but it moved on entirely into cultural matters, even in 2020.

Another scholar regarding this is Charles Murray. His book ‘Coming Apart: The State of White America, 1960–2010’, explored the economic consequences of globalisation and how there is a growing gap between white working-class Americans and the urban white-collar class. The sad state of working-class America was largely ignored by the liberal establishment. The state of white America is increasingly divided along economic lines, not cultural lines. The Democrats didn’t even talk about this topic in 2016, nor did they refer to it in 2020. The Party has taken the votes of traditional blue-collar Democrats for granted.

Hence many former voters of Obama switched to Trump. This is why they lost 2016, and may only just marginally win 2020 because of Covid-19. Instead of trying to legitimately deal with the adverse consequences of globalisation, and help those people that lost their jobs to China and Mexico, their mantra was focused on intersectionalism, transgender bathrooms, and the dangers of white supremacy. Think about it, if you are a former worker of a manufacturing factory in Pennsylvania, and you lost your job, got divorced and on unemployment benefits, and the Democrats are talking about 50/50 quotas, gender pronouns, refugee rights, global governance and so on – you would feel politically unrecognised. They ignored the former core base that has voted for them from the 1930s to the 1990s. The embodiment of woke politics is symbolised by Democratic politicians like Stacey Abrams, Kamala Harris (the unlikable Vice-Presidential candidate), Alexandra Ocasio-Cortez and others.

George Mason University Professor Alex Tabarrok’s Tweet sums this phenomenon quite well:

My takeaway is that a large number of people HATE the cultural left (not the econ left) and are willing to put up with almost anything, including incompetence, chaos, corruption and bad policy, to signal their views loud and clear.

The Democrats need to move on from identity politics and move back to the core economic issues of our time – this also applies to the New Zealand Labour Party and the Greens by the way. The world is witnessing the rise of a new technological revolution and developments in Artificial Intelligence and automation. This will disrupt the international labour market significantly. This will be far more pervasive than the Industrial Revolution and exponentially more consequential. We also have global warming and climate change that requires vigorous economic and scientific analysis to legitimately solve this international problem. We also have an ongoing geopolitical competition with the West and China. Are Democrats taking these challenges seriously? In my eyes, the answer is ‘No’. The economic left of the party needs to regain control of the narrative and the cultural left need to understand that this style of woke politics will drive more voters towards the right. There is a legitimately strong case for competent centre-left politics that can try to correct structural dislocation of manufacturing work and increasingly precarious jobs (including repetitive white-collar jobs too). I see politicians such as Andrew Yang and Tulsi Gabbard as the potential embodiment of the Democratic Party’s future (coincidently they are American minorities as well).

The Democrats have so far been absolutely hopeless. Regardless of what the 2020 election outcomes will be, they need to take socioeconomic issues far more seriously. As a fan and admirer of the United States, I hope they sort their domestic affairs out.

With the ongoing Covid-19 pandemic, the Sino-American relationship is worsening. Tensions are heating as President Trump recently imposed sanctions on China’s largest chipmaker, SMIC.

American actions are becoming a self-fulfilling prophecy towards direct conflict. The world is getting closer to falling for the Thucydides Trap. As foreign policy experts continue to reiterate the inevitabilities of a New Cold War, will conflict be the destiny of the two great powers?

Harvard’s Stephen Walt and Dani Rodrik offered a third alternative in their paper ‘Constructing A New World Order’. The aim is to set an international institutional framework that creates as much stability and cooperation as possible.

First, the authors reject the ‘deep integration’ goals of the liberal internationalists. Rejuvenating multilateralism and hyper-globalisation are well-intended policies. But it creates unintended consequences that undermine the economic stability of western liberal democracies. China would also be unwilling to further integrate into the global trading system from its state-led developmental model.

Second, they disregard the hard-line hawkish approach advocated by the Trump Administration. The current decoupling strategy against China creates ‘beggar-thy neighbour’ effects on other nations. This also prevents mutually beneficial cooperation occurring with the Chinese, especially regarding global public health, improving nuclear security, and addressing climate change.

The goal is setting a pragmatic and realistic approach within the Sino-American relationship. The international system should allow the nation-states to set their own foreign and economic policies.

There are four categorisations of policies that fit within their institutional theory. There is Universal Agreement; Cooperative Negotiations; Autonomous Policy; and Multilateral Governance.

Indeed, Walt and Rodrik’s ‘Modus Vivendi’ international system is a pragmatic institutional mechanism. But, can Uncle Sam stay committed to mutually beneficial cooperation and reduce the risk of falling for the Thucydides Trap?

The Sino-American competition will shape the next few decades of the world order. As both powers strive to compete for power and international influence, the goal for the world is to keep the competition away from a hot war within bounds.

Institutionalising a set of rules on foreign and trade policies could help assuage great power politics. This could also incentivise foreign policymakers from both sides towards restraint as both a peaceful international order and continued globalisation is critical for small powers like New Zealand.

The leaders of the two great powers in the system are two egomaniacs. Their recklessness may make a third alternative for the international system as impossible. But let us hope for the best.

Political discussions in liberal democracies are supposed to be about the battle of ideas, heterodox exchanges, and civil debates. Politicians and leaders present their arguments for a better and productive society through public discourse.

However, recent scandals in Parliament have indicated that it is not really the case. People have forgotten that politicians do not operate under the guises of morality, but manoeuvre based on strategy within established rules of the game — the game of survival in politics. Politics is rife with clever duplicity and manipulation.

Every member of Parliament has two main interests in mind — maintaining power and being perceived as a noble, honest fellow. As Machiavelli once said, “Everyone sees what you appear to be, few really know what you really are.”

Should the public expect more ‘Machiavellian’ behaviour as the election campaign goes underway? If so, what can we learn and observe from the late 15th century philosopher’s wisdom?

Political marketing to Machiavelli is a seductive tool and the use of charming to mislead the public. “It is double pleasure to deceive the deceiver” and “one who deceives will always find those who allow themselves to be deceived.” — A tool the Prime Minister utilises to perfection with her omnipresent slogan, ‘Be Kind’.

Regarding the competence of our leadership, he states that “the first method for estimating the intelligence of a ruler is to look at the men he has around him.” If you do not have a competent team, pointless blunders will hit the spotlight, shown by recent resignations.

Unfortunately, public policy will not be the driver of electoral success. Machiavelli states that “princes have accomplished most who paid little heed to keeping their promises, but who knew how to manipulate the minds of men craftily.” Cunning political strategies are the best ways to preserve or gain power.

Machiavelli always maintained the importance of being effective without being impotently pure. Regarding leadership, he recommends that “Whosoever desires constant success must change his conduct with the times.”

What are the ultimate lessons? Even under liberal democracies, politicians will always use cunning deception to attain or maintain power. Machiavelli was a republican and an astute observer of human nature, that politicians will always strive to serve their main interests — this is just reality.

We must understand that despite the imperfections of our system, liberal democracy still allows us to have a voice in contrast to autocracies. Multiparty systems still provide a check and balance of power on the leadership and their potential to abuse it.

Self-interests are the norms of politics, but if we genuinely want to have competent and effective leadership, the public must understand this aspect of human nature — effective politics require some level of Machiavellianism.

New Zealanders have witnessed partisan nonsense from both sides of the House of Representatives during the Covid-19 pandemic. Ranging from Hamish Walker’s disgraceful letter about quarantine arrivals, Michelle Boag’s woeful decisions, David Clark’s resignation as Health Minister, and in addition blunderous border management by few incompetent Cabinet Ministers. Whilst such partisanship is not surprising to me in politics, the severity of some of these scandals leaves a nasty taste in my mouth. Instead of focusing on the main task of keeping our team of 5 million safe from Covid-19, many politicians in Parliament would rather shoot cheap shots at one another. During the midst of all of this, the centre-left Labour Party will almost certainly win the election and the main key asset for this instrumental task is the Prime Minister herself.

Why do I think the Prime Minister will win? Multifaceted reasons. I’ve known the Prime Minister for a few years beginning in 2016 when I volunteered for the NZ Labour Party initially as a young undergraduate at The University of Auckland. She has always had the personal charm and likability to woo, charm, and make people feel important. I am sure the late Dale Carnegie would approve of her social competence. Without her, the Labour Party would still be in opposition under Andrew Little or some other Labour leader in another universe. Jacinda was the only person that would have had the abilities and leadership qualities to lead Labour to victory, which she did in the 2017 General Election. It was no wonder that for years people touted her as the next leader of New Zealand before. Now as the incumbent, I expect her to win.

Why do I think the Prime Minister will win? Multifaceted reasons. I’ve known the Prime Minister for a few years beginning in 2016 when I volunteered for the NZ Labour Party initially as a young undergraduate at The University of Auckland. She has always had the personal charm and likability to woo, charm, and make people feel important. I am sure the late Dale Carnegie would approve of her social competence. Without her, the Labour Party would still be in opposition under Andrew Little or some other Labour leader in another universe. Jacinda was the only person that would have had the abilities and leadership qualities to lead Labour to victory, which she did in the 2017 General Election. It was no wonder that for years people touted her as the next leader of New Zealand before. Now as the incumbent, I expect her to win.

Jacinda is the most charismatic, likeable, and respectable politician that I have personally witnessed. The masterful political marketing on social media, her genuine smile and exceptional communication skills are nothing short of remarkable. If there was a textbook that I would use for my hypothetical communication class, I would use her as the main role model. I know rarely anyone besides her in the Labour Party with this kind of talent. Some may even claim that she was born for the role…perhaps. This is the key factor that will win her the election. Simply put, the New Zealand public really likes her. The Covid-19 pandemic also may have helped her in the polls, as incumbents tend to do better during crises. Evidenced by President George W. Bush’s approval rating skyrocketing to above 88% during 9/11. But the personable qualities of the Prime Minister helped the Labour Party to climb well above National today. Her identity also shaped her likeability, especially for a small, young and progressive country like Aotearoa. As a female who is young, attractive, relatable, and extremely charismatic, she had all the cards that helped her seem relatable.

In contrast, National has not had anyone on a similar level as Ardern since Sir John Key. Although Simon Bridges is very good when you meet him privately, however, on television and social media, he didn’t have that key spark required to get people on your side. His negative approval rating and his image as a bitter, resentful person hasn’t helped. Although his successor Todd Muller has a positive net approval rating but is someone known as a simple ‘boring old white guy’. Neither does he have personal social competence equal to the Prime Minister and I expect him to be out once the election is over. Until National find a person as equally sociable as Jacinda, they will struggle for years to come. The Key/English years are over, and they must find a long term solution to this missing gap in National’s leadership. The other alternative is for the current leadership self-improve themselves on the basis of mimicking Jacinda’s abilities. The rebuilding stage needs to happen now. For now, they can hope for at least 35% to save most of the caucus, but the pinnacle difference between the two major parties is charisma and charm of the leadership.

Why do I think the Prime Minister will win? Multifaceted reasons. I’ve known the Prime Minister for a few years beginning in 2016 when I volunteered for the NZ Labour Party initially as a young undergraduate at The University of Auckland. She has always had the personal charm and likability to woo, charm, and make people feel important. I am sure the late Dale Carnegie would approve of her social competence. Without her, the Labour Party would still be in opposition under Andrew Little or some other Labour leader in another universe. Jacinda was the only person that would have had the abilities and leadership qualities to lead Labour to victory, which she did in the 2017 General Election. It was no wonder that for years people touted her as the next leader of New Zealand before. Now as the incumbent, I expect her to win.

However, the Labour Party have a clear competence problem within its hierarchy. The Prime Minister has been exceptional as a communicator throughout the pandemic, illustrated in her excellent press conferences with Dr. Ashley Bloomfield. But you cannot run a country well without a great team. There is a reason people like Clare Curran and David Clark were targeted by the opposition – they were incompetent. Period.

Although there are a few very competent Ministers such as Grant Robertson, David Parker, Kris Faafoi, and the new Health Minister Chris Hipkins — on top of his three additional portfolios. After the election, they need to build a broadly new cabinet with the competence, skillsets and abilities to keep New Zealand safe, not just from Covid-19, but also from our precarious economic position. The Prime Minister may be able to rely on her sociability for now, but she must be far more decisive in either sacking or removing incompetent people in Cabinet. As Machiavelli once said, “He who wishes to be obeyed must know how to command.” I’m glad to see the addition of Epidemiologist Dr. Ayesha Verrell in Parliament soon and I know she will make a good contribution for New Zealanders. Hopefully, Ardern realises soon that incompetence will get punished in the next poll in 2023.

The Prime Minister has this in the bag, for now. But until the actual election results, we won’t find out until October.

Singapore, South Korea and Taiwan deserve praise for fighting Covid-19.

While Singapore and South Korea were hit with a second outbreak, their robust containment measures have kicked back in to stop rapid spread of the virus once more. As New Zealand ponders how to prepare for a future pandemic, it should look to East Asia.

Vietnam and Hong Kong also showed early success against the coronavirus, but the New Zealand Government has focused its attention on those first three countries.

The common factor for their success was their experience with the SARS pandemic in 2003 and MERS in 2015. They built better epidemiological and quarantine systems along with border controls, high-level diagnostic testing and rapid contact tracing capacities. They also regularly disinfect public spaces and encourage the public use of masks.

In the last few weeks, another outbreak of Covid-19 makes it appear Singapore’s performance was a complete failure, but it was not. These new community cases constitute only 7% of the total count and more accurately reflect human error in monitoring a handful of migrant dormitories than a systemic failure of the city-state’s response plans.

Further north, South Korea recovered quickly from an initial outbreak in March. The government’s ‘smart-city data hub’ allowed it to quickly locate cases again after a second outbreak occurred in Seoul bars. So far, a total of 1982 possible cases have been rapidly traced by this system, keeping the average number of fresh daily cases low at 23.

Stanford University’s Jason Wang said Taiwan’s response was among the best in the world. Its timely border controls for flights coming from China began on December 31, 2019 – a full month before other nations thought about similar controls. By March 20, Taiwan only had 27 new cases. Once again, a digital surveillance system was critical in tracking down and isolating individuals with the virus.

New Zealand’s Covid-19 containment performance was impressive. But, as Kiwi epidemiologists have emphasised, its contact tracing system still has plenty of room for improvement. As South Korea and Singapore have shown, there is still a real risk of a second outbreak from even one new superspreader.

That’s why it is an imperative that New Zealand take this opportunity to repair and prepare its contact tracing capacity to ensure the country holds onto its hard-won gains. Those three East Asian states offer plenty of great examples to get this done.