This is a good review by Michael Reddell on my co-authored report. As he pointed out, we agree with the Goodhart/Pradhan hypothesis on the demographic implications on the global financial system.

At 11am the New Zealand Initiative released their latest report, by Bryce Wilkinson and Leonard Hong, under the title “Walking the Path to the Next Financial Crisis”. It comes complete with a Foreword from former Reserve Bank chief economist (and former Board chair) Arthur Grimes, under the title “A short walk?”, foretelling doom and repeating his recent attacks on the Reserve Bank’s conduct of monetary policy over the last 20 months, ending with the ominous – and printed in bold – declaration “This time is not different”.

The Initiative was kind enough to send me an embargoed copy yesterday. Perhaps the first thing that rather surprised me – in a document that is really quite critical of both monetary and fiscal policy and aspects of the way the Bank does other things – is that the acknowledgements include thanks to a Reserve Bank MPC member (Bob Buckle) for “valuable feedback…

The world’s major economies are walking into the next global financial crisis. Moreover, their authorities do not seem willing to change direction. They fear that raising interest rates or cutting government budget deficits risks precipitating the collapse they seek to avoid.

Those are the major conclusions of our report we released last Thursday.

In response to the Global Financial Crisis over a decade ago – and then again to Covid-19 – worldwide, major central banks have eased monetary policy settings to an extraordinary and potentially destabilising degree.

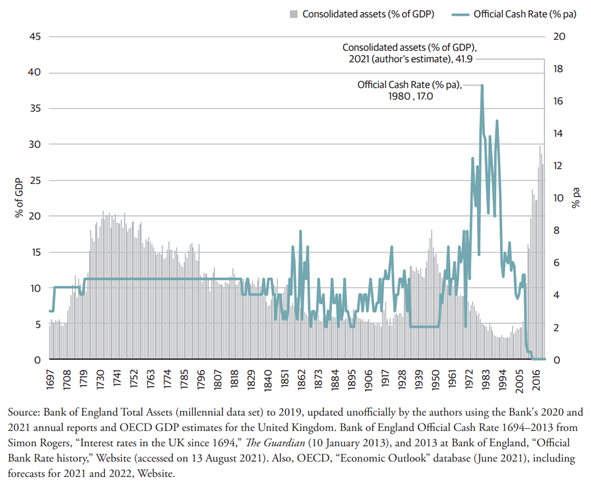

The Bank of England is the world’s oldest central bank. Never since 1697 has its control interest rate been as low as it is today (0.1% pa). Never has its balance sheet relative to gross domestic product (GDP) been as bloated from creating money as it is today. (See the following figure)

The US Federal Reserve, the European Central Bank, and the Bank of Japan have progressively also adopted historically extreme levels for monetary policy settings.

Simultaneously, many governments have pushed their public debt ratios up to an extraordinary degree. Federal public debt held by the public was a historic high relative to GDP at the end of World War II. Congress’s Office of Management and Budget now forecasts that this high will be exceeded in 2024 – a war-time like debt in peace time. This is unprecedented, and it is because of large ongoing budget deficits. The US Federal government’s projected fiscal deficit for 2021 is an astonishing 16.7% of GDP.

In September, US Treasury Secretary Janet Yellen warned the US was heading for sovereign default if the government’s debt ceiling was not lifted. Eventually, Congress agreed to increase the limit, but this merely kicks the debt can down the road – again.

In Europe, a condition set in 1992 for monetary union was that member countries’ gross public debt ratios should not exceed 60% of GDP. According to the latest official forecasts, only 7 of 22 countries will comply in 2021. All the largest economies now exceed 60%. The debt ratios for the seven worst cases exceed 100% – for Italy it is a crippling 166%.

Italy’s high debt ratio is a serious risk to the stability of the Euro currency block. This is because its economy looks to be too large for the rest of Europe to bail out.

Lower interest rates invite governments to borrow more. The utter perversity of the current situation is epitomised by the fact that the Eurozone’s overall government net financial indebtedness has never been higher and the net interest cost lower relative to GDP.

China is also a potential source of instability. Serious debt problems have emerged in its housing market – which accounts for 29% of its economy. This makes it of potential global significance. The debt crisis at Evergrande – the second largest property developer illustrates the concern.

Globally, persistently low interest rates encourage firms and households to borrow excessively to buy assets that would otherwise be over-priced. That contains the seeds for that next crash.

Low interest rates also prolong the existence of “zombie” companies that should be wound up. Healthy companies could use their resources more productively.

High public debt ratios not backed by assets of comparable value give governments a conflict of interest. As economic managers, government should be leaning against excessive borrowing rather than fuelling it by low interest rates and quantitative easing.

Being heavily indebted compromises government’s willingness to act.

This problem of excessive borrowing and over-priced assets has been made worse by the signal the major central banks have been sending to investors – that the authorities will ‘do whatever it takes’to prevent any major collapse.

Professor Arthur Grimes, former chair of the Reserve Bank’s board, wrote the foreword to the report. He succinctly identified that perverse incentive problem:

“Governments, central banks and private sector financial institutions have together created the seeds of the next crisis on the assumption that policy actions will protect borrowers and lenders from downside risks. The result has been a one-way bet for those positioned for asset price rises, while those who have acted prudently have been left behind.”

The perversity of the current situation is further illustrated by the US. In 2020, it recorded the greatest decline in economic activity (real GDP) in at least 60 years. Its unemployment rate more than doubled.

Yet US household wealth rose by a record amount (26%). In dollar terms, it rose by much more than if households had saved 100 percent of national income in 2020.

So, how could US households overall become far more prosperous amidst the biggest downturn in over 60 years? The answer is capital gains and more money in the bank because of the Federal Reserve’s credit creation and low interest rates. US sharemarkets have boomed along with property prices.

The Initiative’s report traces the path to the current government ‘debt trap’ situation, first under the gold standard and subsequently with fiat money.

There is an optimistic scenario. It requires continuing near zero interest rates; low inflation, strong growth that lifts tax revenues; and firm resolve to reduce government budget deficits.

One can hope, but each step in this scenario looks implausible. Consumer price inflation has emerged this year that can only put upwards pressure on interest rates; pressure that central banks have been resisting.

In the past, periods of excessive debt and money creation have tended to end badly. Our report considers two much less rosy, low growth, high unemployment scenarios and one disastrous one of ‘Great Depression’ dimensions.

We leave it for readers to decide what probabilities to put on these and other possible scenarios. Nor does the report speculate about the timing of the next global crisis.

New Zealanders can only take precautionary measures. Being a small and globally integrated economy, New Zealand cannot prevent the next financial crisis.

Reducing debt to prudent levels is important both for governments and households. A fiscal council could help Parliament to hold government to account for the quality of its spending.

Firms and households should avoid borrowing to excess to buy over-priced assets. A narrower and more prudent focus for the Reserve Bank is desirable.

The temptation in the face of such extremes in the major economies is to hope that somehow this global episode will not end in tears – that “this time really is different”. That is mere wishful thinking.

Dr Bryce Wilkinson and Leonard Hong of The New Zealand Initiative co-wrote Walking the Path to the Next Global Financial Crisis.

Both the global financial crisis (GFC) of 2007-2008 and the Covid-19 pandemic caused disruptions to the world economy.

During the GFC, stock markets plummeted, and millions of people became unemployed. Business and bank failures resulted in financial pain.

Covid-19 did not cause as much economic destruction as experts predicted. So far, at least.

During this recession, bankruptcies declined during the pandemic, while prices of assets such as cryptocurrencies, stocks, and houses reached record levels. The net worth of US households increased by USD$26 trillion in 2020.

These developments are extraordinary and unusual. Usually, recessions mean severe losses rather than wealth gains. Are our current financial circumstances sustainable?

Our new report Walking the path to the next global financial crisis explains how skyrocketing public debt and monetary policy easing threaten global financial stability.

In the wake of the GFC, government bailouts of financial institutions ratcheted up public debt ratios dramatically. That was not reversed before Covid struck.

Governments and central banks in developed economies now face tough choices regarding interest rates and debt.

Raising interest rates or ending quantitative easing could destabilise asset markets and the economy. Governments, meanwhile, struggle to wind down stimulus spending and fear higher interest payments on debt.

By printing money and maintaining low-interest rates, it also fuels consumer price inflation. In New Zealand, consumer price inflation hit 4.9% – the highest level in over a decade. Inflation in the US and the EU is also approaching 6%.

The authorities are not showing a determination to return settings to more normal levels before the next economic shock occurs. They have led investors to believe that the government will underwrite high asset prices such as cryptocurrencies, stocks and housing.

It is now common to hear terms like “too big to fail” and “whatever it takes” in financial market jargon. Such beliefs are dangerous for financial stability.

For the government, it is prudent to repair the roof while the sun is still shining. Financial support packages were necessary during Covid-19. But the government should have a credible plan for reducing net debt to more sustainable levels once the pandemic is over.

The financial well-being of citizens is at greater risk when governments are less financially prudent.

As a small, globally integrated economy, New Zealand cannot prevent the next financial crisis.

We do not know when the next financial crisis will hit. But we can prepare for it when it does.

New Zealand must prepare for the next global financial crisis

New Zealand’s economy suffered less damage from the pandemic than analysts expected.

But new research warns, however, that just as we are emerging from the COVID-19, a new crisis is already on the horizon.

Walking the path to the next global financial crisis highlights the danger of an economic crash which could see asset prices collapse, businesses fail, and KiwiSaver funds and investment portfolios destroyed. Recent homebuyers may find themselves owing more on their mortgage than their home is worth.

According to the report, governments’ and central banks’ responses to the Global Financial Crisis of 2008 laid the groundwork for the next financial crisis.

With zero interest rates and money printing, asset prices have soared, consumer prices have risen, and public debt has reached dangerous levels globally.

The world’s politicians and central bank governors are now struggling to return to more normal policies. The result is an economically perilous future.

Former Reserve Bank of New Zealand chair Arthur Grimes warns in the foreword to the report there may be only a short time before the next financial crisis. “Central bank actions through the pandemic … have placed New Zealand at greater risk of an asset price collapse with ensuing economic pain; the risk is heightened by the unsustainable fiscal and monetary policies globally,” Grimes writes.

The Government must prepare for the next global financial crisis, even though New Zealand is too small to prevent it. The prudent course is to reduce debt, both public and private.

The Covid-19 financial support package has kept Kiwis off of the dole queue and saved many businesses from bankruptcy. However, the government should promptly repay those debts in order to be prepared for the next financial shock.

Failing to prepare now for the next financial crisis could destroy New Zealanders’ nest eggs and threaten their livelihoods.

We’re on a slope where monetary policy has become increasingly ineffective in promoting real economic growth. Every crisis was met with monetary easing that caused debt and other imbalances to accumulate over time, and that caused the next crisis to be bigger than the previous one.

William White, Former Chief Economist of The Bank of International Settlements

Cracks on the Wall in 2021

A few weeks ago, US Secretary of Treasury Janet Yellen announced that the US government is heading towards default if Congress does not lift its ‘debt ceiling’. As we all know from economic history, the default of the United States would be a catastrophic ‘financial Armageddon’. With the US being the largest economy in the world, this is alarming news.

On the other side of the world, China’s second largest property company, Evergrande is facing a debt crisis. The default of Evergrande may have potential spillovers with the residential market being worth 29% of China’s GDP (Rogoff and Yang, 2020). Excess leverage of the Chinese corporate sector does not spell financial confidence. Some are claiming that this is potentially a Chinese ‘Lehman Brother’ bubble bound to pop like the 2007-08 global financial crisis (GFC).

In Europe, since the advent of Covid-19, the European Central Bank bought virtually all the government bonds (quantitative easing) of European countries like Italy and kept its interest rates at zero percent. No private investor is willing to buy government bonds at this stage. The only market players in this area are central banks.

Something strange is happening across the world economy. We are witnessing imminent cracks in the global financial system. It’s difficult to predict what may occur in the next few months or years, but one thing is clear – the global economy is extremely fragile. The net worth of many individuals and households are bound to crash sooner or later.

There are strong correlations between populism (both left and right wing) and the 2007-08 global financial crisis. (By Ingram Pinn for The Financial Times).

Introduction

Virtually everyone understands that getting into excess debt leads to trouble. Whenever someone sees a ‘red’ balance in their bank accounts, they panic and try to do everything they can to either lower their deficits or pay back the debt. Financial circumstances matter to people. Saving before spending is the common wisdom. This logic applies to governments too. Except they have the ‘printing press’ with government-controlled (or owned) central banks to fill their coffers (as lender of last resort), on top of tax revenue.

Whilst it may be true to claim that governments are different to individuals and households, its economic decisions have significant consequences on our livelihoods.

It’s been a year since the Covid-19 pandemic began. In contrast to last year’s 3% economic contraction, the International Monetary Fund (IMF) projects that the world will face positive economic growth of 6% for 2021 (IMF, 2021). It seems that high vaccination rates are allowing cities and regions to get out of lockdowns. The United States, the United Kingdom, the European Union and other parts of the world are opening up to the rest of the world. In hindsight, financial circumstances appear better than 2020.

However, there are serious questions as to whether this will be the case in the medium term. In response to the Covid-19 pandemic, many governments across the developed world have accumulated debt levels well-beyond their annual economic output (Gross Domestic Product – the value of every single thing sold on every single shelf around NZ and the value of every single person who worked for a whole year) and the net worth of these governments are heavily in the negative (considering the assets and liabilities of governments).

Table 1: Net Worth of Governments

Country

2016

United Kingdom

-141

Finland

-109

United States

-69

Austria

-41

Canada

-29

Germany

-22

Australia

-21

Switzerland

12

South Korea

41

New Zealand

46

Norway

384

As of 2016, governments were already under in the heavy negatives (IMF, 2018)

This is an unprecedented level of debt during peacetime. Instead of fiscal surpluses, we have so far witnessed the exact opposite from governments. Unfortunately prudence is not a popular term for government officials. Low interest rates from central banks induced more governments to borrow more money. They decided to get the money now instead of the future. Instant gratification took precedent over delayed gratification.

In addition, central banks across developed economies printed trillions of dollars out of nothing to stimulate the world economy away from the recession. They also lowered its interest rates to zero-bound levels. In essence, central banks have made borrowing extremely cheap for everyone, including governments. But the such low interest rate levels are unprecedented.

Spending has become easier. Saving money is not rewarded. Inflation undermines the real value of the dollars in your bank account. This forced individuals to speculate in the stock market or the housing market for a decent return. Unproductive zombie firms have been propped up without falling, forcefully maintaining low unemployment levels without ‘creative destruction’ (Banerjee and Hofmann, 2018, 2020)

But what happens if these markets face downturns again later? Everyone may lose everything. Can they react in a similar manner to the GFC of 2008 or Covid-19? Are bailouts from governments even feasible? I’m not entirely sure.

This is why governments and central bank policies matter to all of us. This essay will explore the few key variables that culminated into the current state of financial affairs. The moral hazard problem; the public debt precedent set by the 2007-08 GFC; the doubling down of debt with the responses to Covid-19 and finally the potential long-term ramifications of these responses.

In times of uncertainty, policymakers pursued these policies for correct short-term reasons, but the decisions have created unintended consequences for the future. Central Banks cannot raise interest rates, nor can they suck the printed money out of the system for fears of creating a worse recession. They are now stuck at a corner by kicking the ‘recession’ can to the future. In the words of former Federal Reserve economist Bill Dudley, central banks are “running out of fire power” (Dudley, 2020).

The decisions in response to the pandemic were understandable. In the face of uncertainty, it is entirely rational to have pumped money into the economy, and to have spent billions on the wage subsidy and other fiscal programmes across the developed world – including New Zealand.

But the net consequences is that the financial system does not look healthy or sustainable. In contrast to optimistic scenarios, the reality is that the world is at a crisis point.

Overall, the decisions by governments and central banks have created a financial system that is chugging along entirely on the “excessive build-up of debt” (White, 2021). This is unsustainable and a form of a financial crisis will loom the world soon. It is uncertain how this next crisis will occur, but economic history tells us that risk is always present (Reinhart and Rogoff, 2009).

We will explore the reasons why that is the case. The origins of the problem started with the end of the stagflation period under Paul Volcker.

The Rise of Moral Hazard

The only way to contain the economic damage of a financial fire is to put it out, even though it’s almost impossible to do that without helping some of the people who caused it.

Ben Bernanke, Henry Paulson and Timothy Geithner, on their policy responses to the GFC

Moral hazard is a common economic term used to define human behaviour when people get incentivised to take more risks for greater profit at the expense of the other party. Another term for this is the ‘principal-agent problem’. For example, if I have health insurance I have the incentives to be more careless with my health, assuming the insurance company will bail me out when I need heart surgery based on my heart attack. It’s the problem of taking more risk when you are not as personably liable.

On similar grounds, beginning with the Federal Reserve Chairman Alan Greenspan, central banks intervened in the economy whenever there was a downturn in the stock market. In contrast to health insurance where there is a risk premium demanded by these companies, what Greenspan did was essentially bail out investors and financiers for free repeatedly. Under Greenspan, the Federal Reserve intervened by lowering the Effective Federal Funds rate during the 1987 stock market crash, the 1994 Mexican peso crisis, the 1997 Asian Financial Crisis, the collapse of Long Term Capital Management and the dotcom bubble in 2000 (Rudd, 2009). By easing monetary conditions whenever there was a downturn, he propped up the stock market and economic activity. Essentially, the Fed was providing free insurance to investors. During his reign between 1987 and 2006, he was world renowned for presiding over the ‘Great Moderation’ period of moderate economic growth, low unemployment, low inflation and ‘managing’ the global economy well.

But if you continue bailing out the people that fail, they are more likely to make riskier decisions, assuming a massive profit by taking that risk. Why wouldn’t they!? The Fed had their backs. The higher the S&P 500 went, the more riskier investments they made. We see this in the growth of new financial products in the likes of subprime mortgages market (Mortgages lent to people that do not have the collateral, capital or employment to buy homes, but loaned out on the basis of higher risk. These were sliced and diced into non-risky assets into the form of Collaterized Debt Obligations) and credit default swaps (financial instruments purchased on the assumption that other parties will fill for bankruptcy, which is essentially a bet) during this era. This was a timebomb in the residential sector that was bound to fall, but for the medium term, as long as house prices continue to go up, things looked rosy. Then the global financial crisis happened beginning in 2007.

The Road to High Government Debt Levels: GFC 2007-08

New Zealanders might recall the tumultuous period during the 2007-08 GFC. The fall of Lehman Brothers and other financial institutions across the stock market left investors in panic mode. The financial ‘cancer’ of subprime mortgages and CDOs spread to the entire global financial system. Banks such as Northern Rock in England faced bailouts from the British government and the Bank of England. With the help of the Federal Reserve, the United States had to spend USD$1.5 trillion in bailouts and tax cuts to stimulate the economy and stir away from the global recession. It was a transfer of a banking crisis into a public debt crisis.

Alongside the Federal Reserve in the United States, other central banks – such as the ECB, the Bank of England and the Bank of Japan – begun the process of what economists call quantitative easing (the printing of money) and reducing their interest rates to low record levels. This was to save the economy from falling into further recession.

Millions of people lost their homes, life savings and their livelihoods. Many people became unemployed and lost jobs – some even permanently became redundant. It was an extremely unpleasant sight at the time. Alan Greenspan’s reputation had tarnished completely.

It affected the New Zealand economy as well. NZ unemployment jumped from 3.6% in 2007 to 6.1% by 2010. As a response, under both the Fifth Labour government and Fifth National government, we pursued fiscal stimulus programmes. Thanks to our prudent fiscal measures beginning in 1994 to 2008, we were able to respond well. Under John Key’s National government, our government debt levels went up from 5.4% debt to GDP in 2008, to 25.4% of GDP by 2014. The Reserve Bank under then- Governor Alan Bollard dropped interest rates by 5.75% to stimulate the New Zealand economy (Bollard and Ng, 2012). New Zealand did not need to pursue quantitative easing.

According to Ben Bernanke (the former Federal Reserve Chairman and successor to Greenspan), it was imperative for policymakers in American ‘to do everything it takes’ to stop the world economy facing a modern ‘Great Depression’. They bailed out financial institutions bound to fail, they provided liquidity to the US Treasury by purchasing government bonds and rapidly expanded their balance sheets. The total assets of the Fed increased from USD$1 trillion to USD$2 trillion by 2009, and the Federal Funds rates at 0.75 as indicated in Figure 1.

Under Obama, the US Federal government pursued fiscal stimulus programmes such as the American Recovery Reinvestment Act of 2009. This programme alone added USD$840 billion to the budget deficit. As indicated Figure 2, the federal debt held by the public ballooned from 35.7% in 2008 to 75.9% of GDP by 2017, which is more than double before the GFC.

Other economies such as The European Union, the United Kingdom, Japan and other developed economies spent their way out of the problem. The banking crisis originating in American transformed into a public debt crisis across the developed world (except for fiscally prudent nations such as Australia and New Zealand), culminating into a sovereign debt crisis in Europe – also known as the 2011 Euro crisis.

The GFC revealed excess public borrowing. Countries in Europe such as Greece, Portugal, Ireland, Spain and Cyprus were unable to repay or refinance their debt obligations to their bond holders. Many looked to other European Union member states for financial assistance or even bail outs. An extreme example is Greece. The small Southern European country received series of 100 billion euro bailouts from the International Monetary Fund and the European Union (Voigt, 2012). Germany was the most generous of lenders. Yet despite this, Greece defaulted in 2015 (and is currently barely staying afloat with Greek government debt levels remaining well above 100% at 210% of GDP as of 2021). Many European economies are also floating along thanks to the financial support from prosperous economies such as France and Germany, and low interest rates from the European Central Bank.

Figure 3 shows that governments have been induced to borrow more as interest payments continue to decline. The European system is not healthy by any means. Debt levels and leverage are far too high, encouraged by central bank intervention and help from other countries.

Figure 3:

Euro zone general government net interest cost and financial liabilities (OECD, 2021).

In conclusion, the responses to the GFC saved the global economy facing an economic depression. However, this came at a cost. The banking crisis turned into an inevitable public debt (or sovereign debt crisis). In the United States, public debt continued to accumulate with little indication of deleveraging or fiscal restructuring. Meanwhile, Greece created political and economic turmoil in Europe, amalgamating into populist sentiment in Europe. With the Brexit vote in 2016, the European Union and the euro currency’s future remains uncertain.

If the Greek default created such geopolitical turmoil, imagine what the circumstances would be if any of the major G20 economies face financial trouble. In addition, the initial quantitative easing from central banks restarted the economy following the GFC, but it incentivised governments, households, companies to all take more debt rather than less. The world essentially buckpassed the financial crisis to the future as a short-term band aid. Then in 2020, Covid-19 hit the world starting in Wuhan, China, forcing governments and central banks to make drastic decisions.

The Fiscal and Monetary Consequence of Covid-19

The supply shock to the global economy came from a pandemic. Governments and central banks again took swift decisions. The fiscal and monetary responses to Covid-19 were very similar to the GFC, except the scale and size of the quantitative easing from central banks and deficit spending of governments were far larger. For the Euro zone the average gross financial liability levels were close to 120% of GDP. The United was 141% and the United States was 146%. Under President Biden, the US Federal government’s fiscal deficit was 15.9% of GDP for 2021. For the Euro zone on average it was 7.2% and New Zealand was 4.2% deficit (OECD, 2021). Before in 2008, the ratio of global household, corporate and government debt to GDP was 280%. As shown in Figure 4, in response to the pandemic, in 2020, this ratio had grown by 75% to355%(IIF, 2021). The world has now mortgaged our future by getting into more debt now.

Figure 4:

Global Debt Monitor: COVID Drives Debt Surge—Stabilization Ahead? (IIF, 2021)

Governments around the world have never spent this much money in response to a pandemic in peacetime. The deficits created during the 2007-08 GFC look miniscule in comparison.

In monetary policy, the central banks have pumped more money and liquidity into the system than ever before, shown in Figure 5. ‘Trillions’ are being swashed around the global financial system (For context, 1 trillion is five and a half times New Zealand’s GDP). Bank rates are now virtually zero around the world – see Figure 6. The banks have little firepower left to tackle another financial crisis later down the track. Monetary policy has become less effective as a result of all of these responses beginning from the GFC.

When the United States and the rest of the developed world entered zero-bound rates during the GFC, former Bank of Japan Governor Masaaki Shirakawa noted that when Japan was adopting zero bound interest rates and quantitative easing policies beginning in the early 1990s, he never expected other countries such as the United States to follow suit (Shirakawa, 2014).Yet, other central banks did, and they all entered a road of no return.

Conclusion

The global economy has entered a cross road, unable to turn back towards a period of relative normalcy. Starting with the fiscal and monetary responses to the GFC, governments have accumulated record debt, and central banks lowered its rates and printed money to stir the economy away from prolonged recessions. We have kicked the can down the road to an even more precarious future.

Both governments and central banks are stuck into a corner. Governments’ cannot stop spending, because otherwise unemployment rates would erupt; central banks cannot lift rates for the fear of sovereign default and collapses of heavily indebted companies. The public cannot stop buying inflated assets with the ‘fear of missing out’. Rising inflation and low interest rates incentivise people to stop saving and risk their future wealth through speculation. All of these government responses create bad incentives across the whole global economy.

On monetary policy, the late macroeconomist John Maynard Keynes wrote in 1936 that “If, however, we are tempted to assert that money is the drink that stimulates the system to activity, we must remind ourselves that there may be several slips between the cup and the lip.”

The effectiveness of monetary policy has now been nullified with rates close to zero percent. What can central banks do to respond to the next crisis? Bailouts? Further quantitative easing? Economists cannot predict the future, but we can anticipate risks from recent trends.

Contemplating that future is bleak. The era of normalcy following the end of the Cold War seems like a distant past. The period of ‘normal’ interest rates and sustainable debt levels seem implausible at this stage. The trends have been towards more debt, lower rates and more money printing. What will governments and central banks around the world do? And more importantly, when will this madness end? We will soon find out in the near future.

References

Alan Bollard and Tim Ng, “Learnings from the global financial crisis,” Sir Leslie Melville Lecture, Australian National University, Canberra (9 August 2012).

Alan Rappeport, “As debt default looms, Yellen faces her biggest test yet,” The New York Times (23 September 2021).

Bill Dudley, “The Fed Is Really Running Out of Firepower”, Bloomberg (28 October 2020).

Emre Tiftik and Khadija Mahmood, “Global Debt Monitor: COVID Drives Debt Surge—Stabilization Ahead?” Institute of International Finance (17 February 2021).

International Monetary Fund. “IMF Public Sector Balance Sheet Statistics: Database.”

Kenneth Rogoff and Carmen Reinhart, This Time is Different (Princeton University, 2009).

Kenneth Rogoff and Yuanchen Yang. “Has China’s Housing Production Peaked?” China & World Economy 29:1 (2021), 1–31.

Kevin Rudd, “The Global Financial Crisis”, The Monthly (February 2009).

Kevin Voigt, “Eurozone approves new $173B bailout for Greece,” CNN (21 February 2012).

Mark Dittli, “Central banks keep shooting themselves in the foot,” Interview with William White, The Market (6 November 2020).

Masaaki Shirakawa, “Is Inflation (Or Deflation) ‘Always and Everywhere’: A Monetary Phenomenon? My Intellectual Journey in Central Banking,” BIS Paper 77e (2014).

Matt Egan, “‘Financial Armageddon’. What’s at stake if the debt limit isn’t raised,” CNN Business (8 September 2021).

OECD.Stat.

Ryan Banerjee and Boris Hofmann, “Corporate Zombies: Anatomy and Life Cycle,” BIS Working Papers No. 882 (2020)

Ryan Banerjee and Boris Hofmann, “The Rise of Zombie Firms: Causes and Consequences,” BIS Quarterly Review (2018)

The Economist: “How should recessions be fought when interest rates are low?” (21 October 2017).

US Federal Reserve, “Federal Debt Held by the Public as Percent of Gross Domestic Product.”

US Federal Reserve, “Credit and liquidity programs and the balance sheet.”

William White, “It’s Worse than ‘Reverse’: The Full Case Against Ultra Low and Negative Interest Rates,” Working Paper No. 151 (New York: Institute for New Economic Thinking, 2021).

Yardeni, and Mali Quintana. “Central Banks: Monthly Balance Sheets” (Yardeni Research, Inc. 2021).

Over the course of the last two years in Wellington, I have come to realise something. Many people enter politics with the best of intentions, however, they end up becoming a part of the system. In my opinion, the majority in the House of Representatives place poll numbers ahead of effective governance and public administration. And this is failing the public. There appears to be no vision, let alone a direction, for the future of Aotearoa New Zealand from either the government or Opposition.

Those who know me well will recall that I campaigned for Labour four years ago, and at the time I was genuinely enthusiastic about Jacinda’s message of hope, change and progress. I was proud to be part of a movement that fostered change. Solving the problems surrounding the housing market, inequality, education, health, well-being, and climate change was a moral imperative for me.

The Labour Party is now in power. But how well have they done on objective metrics such as Housing? With the exception of our crisis management – such as our containment of Covid-19 – they are worse.

In the past year, house prices have increased by 32%. The inequality gap in wealth and income worsened under the current government than under any of the previous three governments combined. PISA rankings in Math, Science, and Reading have all fallen significantly. We have inadequate public health measures due to a limited number of intensive care units, and our doctors and nurses are not receiving the salaries they deserve. Meanwhile, the Ministry of Health bureaucrats have more money in their coffers without delivering any meaningful results. In spite of government commitments to spend billions on mental health, the situation continues to worsen. With regard to climate change, our oil and gas ban has caused market externalities – we burn more coal to generate electricity, which resulted in higher emissions. This is utterly unacceptable.

Politicians always claim in the media that they tried their best. In a company or in the private sector, if this was the performance result, they would all be severely questioned by the Board of Directors. However, in politics, there is no direct accountability. Failures are not grounds for dismissal, except for the voting system every three years.

However, one of the reasons for government failures have to do with the lack of competition. Currently, the Opposition is in disarray. Instead of proposing public policy solutions of their own, they are fighting among themselves. There is little incentive for the leading party to push for positive change when they are dominating the polls without much being achieved. Essentially, there is no need for them to perform better. Furthermore, the quality of politicians throughout the House is abysmal. The fact that the Minister of Justice, Kris Faafoi, had to remain in politics – despite wanting to leave – tells us much about the lack of talent within the party.

Personally, I really don’t care who is in charge so long as the performances are excellent. In a similar manner to when the CEO of a company changes, where outputs and profits stay high. For this to occur in our political system, we must cultivate more competent and talented individuals across the political spectrum. We need people that care more about ‘policy’ not ‘politics’ in the future. This is essential to the economic growth and well-being of the country.

My article in the week’s Insights newsletter. It is a #3, the third item in the newsletter which is always an attempt at humour. You can sign up to our weekly newsletter here.

One of the finest shows on economic affairs was ‘Clarke and Dawe’. The two satirists collaborated from 1989 until John Clarke’s death 2017. If only this partnership were still around in the era of Covid-19 and quantitative easing. I miss their satire.

So how would Clarke and Dawe explain the current global economic recession today? I wonder…

BD: Thanks for joining, you’re a macroeconomist, correct?

JC: A pleasure to be here. Yes, I am indeed.

BD: As a response to Covid-19, quantitative easing (QE) was used by central banks. How does it work?

JC: Well, it starts at a desk in a central bank. You take the computer out of box, press buttons, click enter. You alert the banking sector and the Treasury, send both an email, and press copy. You buy bonds and send money.

BD: And why did central banks start QE? Isn’t that ‘counterfeit money’? You can’t just print money at will.

JC: They print it digitally. You press buttons with more zeros on the computer – Boom! New dollars, just like that. It’s a free ATM machine, just bigger.

BD: But there is no free lunch, though? What are the financial implications?

JC: Potential inflation, consumer prices could go up. The more money you print like Zimbabwe, the poorer you become.

BD: What do macroeconomists do?

JC: We talk about economics without stories. It’s up, down, left, or right for unemployment, CPI, inflation, GDP etc. Straightforward, really.

BD: Correct, and what about government debt globally?

JC: They’re broke. Particularly the Europeans, the Japanese, and the Americans. Debt levels are above their entire annual economic output.

BD: Right… so what does that mean?

JC: No money. Broke economies were being lent money by other broke economies, but now they are all broke. The only lenders are central banks. It’s a last resort, so to speak.

BD: My goodness. The digital printer machine is out of control, and governments are broke. What’s the next step you think?

JC: Another bail out from central banks, probably. And then a bail-out of the central banks, most likely by themselves.

BD: Correct, an ongoing merry-go-round. Is this sustainable?

JC: Yeah, we might as well be entering clown world.

BD: Correct. That’s a grim end to that story. Thank you for your time.

JC: My pleasure. Oh, I better check the gold price. And where did I leave the key to my safe deposit box?

The political ‘buck passing’ of the responsibility for unaffordable housing by successive governments in New Zealand has created extremely expensive housing markets in cities such as Auckland and Wellington – and a national housing crisis. Auckland is the sixth least affordable city among 92 major global housing markets, according to the 2020 Demographia housing survey. The real price of housing in New Zealand increased by 171% from 2000 to 2019, compared with just 11% in Germany in the same period. Despite former Housing Minister Phil Twyford’s reforms, the government has prioritised supressing demand and targeting financial speculation from overseas. Demand-side solutions are just tinkering at the edges of the problem. Long-term demographic transformations and changing household sizes are affecting overall housing demand. Inflexible housing development is the core problem, and only freeing up enough supply can solve our housing unaffordability and overcrowding.

The projections in this report show that our housing problems are set to worsen. From 2019 to 2038, the annual average additional dwellings needed will increase from 26,246 (‘low’ migration and ‘low’ fertility) to 34,556 (‘medium’ migration and ‘high’ fertility). From 2019 to 2060, we will need 15,319 (‘low’ migration and ‘low’ fertility) and 29,052 (‘medium’ migration and ‘high’ fertility) additional dwellings annually. These figures do not take into account the annual demolition and replacement rate of dwellings and the current undersupply of 40,000. Since 1992, New Zealand has added only 21,445 net private dwellings annually to the housing stock. We are simply not building enough to meet the looming demographic changes and demands.

Our housing needs are also set to rise much faster than population growth. The average annual number of dwellings needed based on just projected population growth, excluding the smaller household size, was between 5,452 (‘low’ migration and ‘low’ fertility) and 21,543 (‘medium’ migration and ‘high’ fertility) to 2060 in our analysis. The difference represents an annual shortfall of 9,867 dwellings for the former and 7,509 for the latter (or 64% and 26%, respectively). This means housing policy using only projected population growth will markedly underestimate future demand.

Covid-19 and the Reserve Bank of New Zealand’s monetary response to the ongoing recession has led to much financial capital flowing into the housing market. Consequently, the national house price average reached $725,000, an increase of 19.8% from October 2019 to October 2020. Low interest rates created incentives for greater borrowing and investments in real assets such as financial stocks and housing. However, if sound institutional arrangements were established and growing supply could meet growing demand, there would be far fewer speculative incentives.

Local councils and Statistics New Zealand already factor demographic changes in their household and dwelling projections, but the effect of the average household size on housing demand is rarely discussed in the public sphere. The aggregate housing demand is based not just on population growth, but also the composition of each household. With household sizes shrinking, fewer people living with many children, and population ageing, we have ‘empty nests’ and ‘crowded houses’.

For this report, we calculated long-term population numbers using the demographic software Spectrum. Based on three fundamental factors – net migration, total fertility, and life expectancy – 36 scenarios were projected to 2060 (and 2038 for dwelling projections). In 33 out of the 36 scenarios, New Zealand’s population in 2060 will be larger than it is today. Under all 36 scenarios, the median age will be higher. The 36 scenarios were further narrowed to the six most plausible based on New Zealand’s recent demographic history. Among the six, the variation in median age and population size by 2060 was vast – the projected population ranged between 5.55 million and 7.26 million, while the median age was between 41.0 and 48.5 years. Even if migration is low (say, 14,000 per annum), New Zealand’s population will still grow substantially over the next few decades.

The current housing crisis is just the tip of the iceberg – if the government does not change course, future generations will face abysmal housing affordability prospects. Stopping migration completely would only produce new problems while doing little to fix the housing problem.

Demographic changes also have long-term implications for fiscal prudence. Under the six most plausible Spectrum scenarios, the dependency rate rose with population ageing, and the number of those over 65 years by at least 23% by 2060. This will result in fewer future taxpayers and more demands on working-age New Zealanders to fund public services such as healthcare and pensions.

Policymakers need to make our economic institutions more versatile so New Zealand can cope with any combination of demographic or household scenarios in the future. New Zealand had net zero migration in 2020 due to Covid-19 related border closures but this did not stop housing inflation. Politicians should stop blaming the housing crisis on migration, land banking investment, and speculation, and instead find policy solutions to free up urban development and housing supply. Faster productivity growth too would help fund additional public services in the long term.

Building now and fast is imperative for the nation’s future economic and social wellbeing.

Click below to download the two-page summary of The Need to Build: The demographic drivers of housing demand.

Up to a million Kiwis live overseas with a right to return to New Zealand. While the country is now effectively free of Covid-19, with cases only in the country’s quarantine facilities, the pandemic rages abroad and is unlikely to abate anytime soon. Even if a vaccine is developed this year, scaling up its production will take time. In the meantime, the Government must scale up its own capabilities and capacity within its managed isolation and quarantine facilities.

This report provides a pathway toward safer scaling-up of border capabilities. It begins from the principle that safe entry should be allowed, and that risky entry must be made safe.

Beginning from that principle, the report argues that the New Zealand border should be reopened to travellers arriving from places that are similarly free of Covid-19. Islands in the Realm of New Zealand depend on travel to and from New Zealand and are currently Covid-free. Taiwan has no community transmission and has pandemic control systems at least as strong as New Zealand’s. Maintaining border restrictions against travel to and from safe places imposes substantial harm. Continued closed borders to the Pacific Islands imposes an onerous humanitarian burden along with economic calamity.

Like kayakers in stormy seas rafting up together for safety, New Zealand should ‘raft up’ with other Covid-free places.

Entry from other locations must be made safe. And while closing borders entirely can feel like the right response when other parts of the world are in dire straits, it is impossible. Too many Kiwis live abroad and may wish to return. The managed isolation and quarantine system must be able to scale up to accommodate those people along with potential non-citizen visitors from similar locations.

This report argues that the Government should shift its approach. Rather than considering charging some arriving Kiwis for their stays in managed isolation, it should instead directly subsidise the stays of returning Kiwis whose stays the Government would wish to support with a voucher system.

Under the proposed voucher system, those wishing to come to New Zealand – citizens or not – would be required to present before boarding proof of a booking in one of the approved managed isolation facilities. Eligible returning Kiwis could apply their vouchers toward the full or partial cost of their stay in managed isolation. Vouchers could be set at a level consistent with the cost of a stay at a basic facility. Other returnees would need to bear the full cost of their stay. Facilities would be free to set their own room fees, but the Government would charge each facility for the full cost of police, military and other staff involved with managing isolation.

The Government would continue to oversee safety in managed isolation and private accommodation facilities would continue to provide the rooms. But this shift would make it far easier for returning Kiwis, and others, to manage their own arrivals while freeing the Government of the burden of scrambling to place arriving visitors into scarce spaces in managed isolation. It would also encourage other facilities to shift into providing managed isolation services (under Government oversight and supervision).

The present system is strained. It struggles to accommodate need, but must scale up substantially if Kiwis abroad choose to exercise their right to return home. Allocating scarce positions in managed isolation by Ministerial discretion forces Ministers into impossible positions in deciding whose need is greatest.

Being able to scale up safely is critically important. The entire country made incredibly costly efforts to make New Zealand effectively Covid-free. Some Kiwis continue to bear those costs through family separation, unemployment or failing businesses. And for a long time yet, the country will be paying off the new government debt accrued to help the economy survive lockdown.

Improving border protocols to allow for safe entry at scale would not only help those worst affected by the collective elimination efforts, it would open up opportunities that simply were not available in the pre-pandemic world. Rather than trying to estimate the extent of New Zealand’s likely economic losses, the country could be looking at stronger economic opportunities.

Recommendations The New Zealand Government should:

Set a principle to allow safe entry into New Zealand;

Recognise that entry from safe places by people who have not recently been to risky places is safe. Re-open the border to entry from Taiwan and the Covid-free Pacific Islands and assess whether individual Australian states could be considered safe;

Support the Pacific Island neighbours in ensuring safe external borders;

Continue to assess the adequacy of safety protocols on flights to risky places and at airports handling passengers from risky places;

Allow greater scaling-up of managed isolation by: o Allowing those arriving to take up a greater portion of the cost: full user-pays for non-citizens and a voucher-based co-payment scheme for returning residents and citizens; o Certifying facilities as authorised providers of managed isolation or quarantine services; o Charging isolation facilities for the isolation management services provided by the government; o Allowing facilities to provide their own management services if they are able to credibly demonstrate capability of doing so safely, but only under strict supervision and process auditing; o Requiring all arrivals book their own accommodation in authorised isolation facilities and provide proof of booking before boarding flights to New Zealand; o Training potential isolation management staff; o Charging isolation facilities for the isolation services provided by the government on a full cost-recovery basis;

Layering additional safety protocols for non-citizens arriving from risky places to further reduce risk as numbers increase, such as post-isolation testing and daily health check-ins;

Consult with New Zealand’s epidemiologist community over the medium term as both testing and app-based technologies develop to assess whether alternative sets of restrictions could reduce risk at lower cost for travellers from less risky but not risk-free places.

New Zealanders have witnessed partisan nonsense from both sides of the House of Representatives during the Covid-19 pandemic. Ranging from Hamish Walker’s disgraceful letter about quarantine arrivals, Michelle Boag’s woeful decisions, David Clark’s resignation as Health Minister, and in addition blunderous border management by few incompetent Cabinet Ministers. Whilst such partisanship is not surprising to me in politics, the severity of some of these scandals leaves a nasty taste in my mouth. Instead of focusing on the main task of keeping our team of 5 million safe from Covid-19, many politicians in Parliament would rather shoot cheap shots at one another. During the midst of all of this, the centre-left Labour Party will almost certainly win the election and the main key asset for this instrumental task is the Prime Minister herself.

Why do I think the Prime Minister will win? Multifaceted reasons. I’ve known the Prime Minister for a few years beginning in 2016 when I volunteered for the NZ Labour Party initially as a young undergraduate at The University of Auckland. She has always had the personal charm and likability to woo, charm, and make people feel important. I am sure the late Dale Carnegie would approve of her social competence. Without her, the Labour Party would still be in opposition under Andrew Little or some other Labour leader in another universe. Jacinda was the only person that would have had the abilities and leadership qualities to lead Labour to victory, which she did in the 2017 General Election. It was no wonder that for years people touted her as the next leader of New Zealand before. Now as the incumbent, I expect her to win.

Why do I think the Prime Minister will win? Multifaceted reasons. I’ve known the Prime Minister for a few years beginning in 2016 when I volunteered for the NZ Labour Party initially as a young undergraduate at The University of Auckland. She has always had the personal charm and likability to woo, charm, and make people feel important. I am sure the late Dale Carnegie would approve of her social competence. Without her, the Labour Party would still be in opposition under Andrew Little or some other Labour leader in another universe. Jacinda was the only person that would have had the abilities and leadership qualities to lead Labour to victory, which she did in the 2017 General Election. It was no wonder that for years people touted her as the next leader of New Zealand before. Now as the incumbent, I expect her to win.

Jacinda is the most charismatic, likeable, and respectable politician that I have personally witnessed. The masterful political marketing on social media, her genuine smile and exceptional communication skills are nothing short of remarkable. If there was a textbook that I would use for my hypothetical communication class, I would use her as the main role model. I know rarely anyone besides her in the Labour Party with this kind of talent. Some may even claim that she was born for the role…perhaps. This is the key factor that will win her the election. Simply put, the New Zealand public really likes her. The Covid-19 pandemic also may have helped her in the polls, as incumbents tend to do better during crises. Evidenced by President George W. Bush’s approval rating skyrocketing to above 88% during 9/11. But the personable qualities of the Prime Minister helped the Labour Party to climb well above National today. Her identity also shaped her likeability, especially for a small, young and progressive country like Aotearoa. As a female who is young, attractive, relatable, and extremely charismatic, she had all the cards that helped her seem relatable.

In contrast, National has not had anyone on a similar level as Ardern since Sir John Key. Although Simon Bridges is very good when you meet him privately, however, on television and social media, he didn’t have that key spark required to get people on your side. His negative approval rating and his image as a bitter, resentful person hasn’t helped. Although his successor Todd Muller has a positive net approval rating but is someone known as a simple ‘boring old white guy’. Neither does he have personal social competence equal to the Prime Minister and I expect him to be out once the election is over. Until National find a person as equally sociable as Jacinda, they will struggle for years to come. The Key/English years are over, and they must find a long term solution to this missing gap in National’s leadership. The other alternative is for the current leadership self-improve themselves on the basis of mimicking Jacinda’s abilities. The rebuilding stage needs to happen now. For now, they can hope for at least 35% to save most of the caucus, but the pinnacle difference between the two major parties is charisma and charm of the leadership.

Why do I think the Prime Minister will win? Multifaceted reasons. I’ve known the Prime Minister for a few years beginning in 2016 when I volunteered for the NZ Labour Party initially as a young undergraduate at The University of Auckland. She has always had the personal charm and likability to woo, charm, and make people feel important. I am sure the late Dale Carnegie would approve of her social competence. Without her, the Labour Party would still be in opposition under Andrew Little or some other Labour leader in another universe. Jacinda was the only person that would have had the abilities and leadership qualities to lead Labour to victory, which she did in the 2017 General Election. It was no wonder that for years people touted her as the next leader of New Zealand before. Now as the incumbent, I expect her to win.

However, the Labour Party have a clear competence problem within its hierarchy. The Prime Minister has been exceptional as a communicator throughout the pandemic, illustrated in her excellent press conferences with Dr. Ashley Bloomfield. But you cannot run a country well without a great team. There is a reason people like Clare Curran and David Clark were targeted by the opposition – they were incompetent. Period.

Although there are a few very competent Ministers such as Grant Robertson, David Parker, Kris Faafoi, and the new Health Minister Chris Hipkins — on top of his three additional portfolios. After the election, they need to build a broadly new cabinet with the competence, skillsets and abilities to keep New Zealand safe, not just from Covid-19, but also from our precarious economic position. The Prime Minister may be able to rely on her sociability for now, but she must be far more decisive in either sacking or removing incompetent people in Cabinet. As Machiavelli once said, “He who wishes to be obeyed must know how to command.” I’m glad to see the addition of Epidemiologist Dr. Ayesha Verrell in Parliament soon and I know she will make a good contribution for New Zealanders. Hopefully, Ardern realises soon that incompetence will get punished in the next poll in 2023.

The Prime Minister has this in the bag, for now. But until the actual election results, we won’t find out until October.