This is a good review by Michael Reddell on my co-authored report. As he pointed out, we agree with the Goodhart/Pradhan hypothesis on the demographic implications on the global financial system.

At 11am the New Zealand Initiative released their latest report, by Bryce Wilkinson and Leonard Hong, under the title “Walking the Path to the Next Financial Crisis”. It comes complete with a Foreword from former Reserve Bank chief economist (and former Board chair) Arthur Grimes, under the title “A short walk?”, foretelling doom and repeating his recent attacks on the Reserve Bank’s conduct of monetary policy over the last 20 months, ending with the ominous – and printed in bold – declaration “This time is not different”.

The Initiative was kind enough to send me an embargoed copy yesterday. Perhaps the first thing that rather surprised me – in a document that is really quite critical of both monetary and fiscal policy and aspects of the way the Bank does other things – is that the acknowledgements include thanks to a Reserve Bank MPC member (Bob Buckle) for “valuable feedback…

The world’s major economies are walking into the next global financial crisis. Moreover, their authorities do not seem willing to change direction. They fear that raising interest rates or cutting government budget deficits risks precipitating the collapse they seek to avoid.

Those are the major conclusions of our report we released last Thursday.

In response to the Global Financial Crisis over a decade ago – and then again to Covid-19 – worldwide, major central banks have eased monetary policy settings to an extraordinary and potentially destabilising degree.

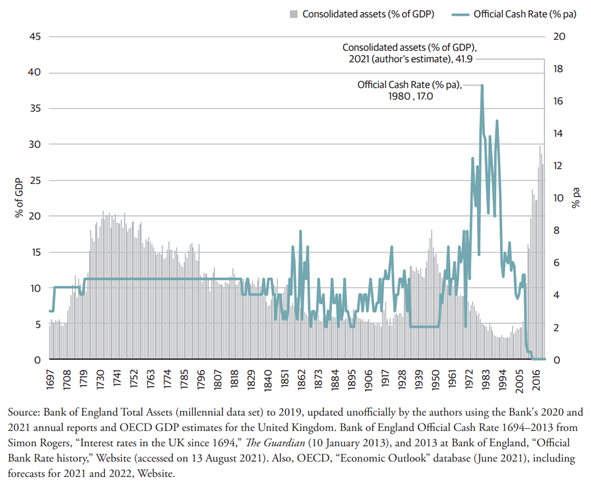

The Bank of England is the world’s oldest central bank. Never since 1697 has its control interest rate been as low as it is today (0.1% pa). Never has its balance sheet relative to gross domestic product (GDP) been as bloated from creating money as it is today. (See the following figure)

The US Federal Reserve, the European Central Bank, and the Bank of Japan have progressively also adopted historically extreme levels for monetary policy settings.

Simultaneously, many governments have pushed their public debt ratios up to an extraordinary degree. Federal public debt held by the public was a historic high relative to GDP at the end of World War II. Congress’s Office of Management and Budget now forecasts that this high will be exceeded in 2024 – a war-time like debt in peace time. This is unprecedented, and it is because of large ongoing budget deficits. The US Federal government’s projected fiscal deficit for 2021 is an astonishing 16.7% of GDP.

In September, US Treasury Secretary Janet Yellen warned the US was heading for sovereign default if the government’s debt ceiling was not lifted. Eventually, Congress agreed to increase the limit, but this merely kicks the debt can down the road – again.

In Europe, a condition set in 1992 for monetary union was that member countries’ gross public debt ratios should not exceed 60% of GDP. According to the latest official forecasts, only 7 of 22 countries will comply in 2021. All the largest economies now exceed 60%. The debt ratios for the seven worst cases exceed 100% – for Italy it is a crippling 166%.

Italy’s high debt ratio is a serious risk to the stability of the Euro currency block. This is because its economy looks to be too large for the rest of Europe to bail out.

Lower interest rates invite governments to borrow more. The utter perversity of the current situation is epitomised by the fact that the Eurozone’s overall government net financial indebtedness has never been higher and the net interest cost lower relative to GDP.

China is also a potential source of instability. Serious debt problems have emerged in its housing market – which accounts for 29% of its economy. This makes it of potential global significance. The debt crisis at Evergrande – the second largest property developer illustrates the concern.

Globally, persistently low interest rates encourage firms and households to borrow excessively to buy assets that would otherwise be over-priced. That contains the seeds for that next crash.

Low interest rates also prolong the existence of “zombie” companies that should be wound up. Healthy companies could use their resources more productively.

High public debt ratios not backed by assets of comparable value give governments a conflict of interest. As economic managers, government should be leaning against excessive borrowing rather than fuelling it by low interest rates and quantitative easing.

Being heavily indebted compromises government’s willingness to act.

This problem of excessive borrowing and over-priced assets has been made worse by the signal the major central banks have been sending to investors – that the authorities will ‘do whatever it takes’to prevent any major collapse.

Professor Arthur Grimes, former chair of the Reserve Bank’s board, wrote the foreword to the report. He succinctly identified that perverse incentive problem:

“Governments, central banks and private sector financial institutions have together created the seeds of the next crisis on the assumption that policy actions will protect borrowers and lenders from downside risks. The result has been a one-way bet for those positioned for asset price rises, while those who have acted prudently have been left behind.”

The perversity of the current situation is further illustrated by the US. In 2020, it recorded the greatest decline in economic activity (real GDP) in at least 60 years. Its unemployment rate more than doubled.

Yet US household wealth rose by a record amount (26%). In dollar terms, it rose by much more than if households had saved 100 percent of national income in 2020.

So, how could US households overall become far more prosperous amidst the biggest downturn in over 60 years? The answer is capital gains and more money in the bank because of the Federal Reserve’s credit creation and low interest rates. US sharemarkets have boomed along with property prices.

The Initiative’s report traces the path to the current government ‘debt trap’ situation, first under the gold standard and subsequently with fiat money.

There is an optimistic scenario. It requires continuing near zero interest rates; low inflation, strong growth that lifts tax revenues; and firm resolve to reduce government budget deficits.

One can hope, but each step in this scenario looks implausible. Consumer price inflation has emerged this year that can only put upwards pressure on interest rates; pressure that central banks have been resisting.

In the past, periods of excessive debt and money creation have tended to end badly. Our report considers two much less rosy, low growth, high unemployment scenarios and one disastrous one of ‘Great Depression’ dimensions.

We leave it for readers to decide what probabilities to put on these and other possible scenarios. Nor does the report speculate about the timing of the next global crisis.

New Zealanders can only take precautionary measures. Being a small and globally integrated economy, New Zealand cannot prevent the next financial crisis.

Reducing debt to prudent levels is important both for governments and households. A fiscal council could help Parliament to hold government to account for the quality of its spending.

Firms and households should avoid borrowing to excess to buy over-priced assets. A narrower and more prudent focus for the Reserve Bank is desirable.

The temptation in the face of such extremes in the major economies is to hope that somehow this global episode will not end in tears – that “this time really is different”. That is mere wishful thinking.

Dr Bryce Wilkinson and Leonard Hong of The New Zealand Initiative co-wrote Walking the Path to the Next Global Financial Crisis.

Both the global financial crisis (GFC) of 2007-2008 and the Covid-19 pandemic caused disruptions to the world economy.

During the GFC, stock markets plummeted, and millions of people became unemployed. Business and bank failures resulted in financial pain.

Covid-19 did not cause as much economic destruction as experts predicted. So far, at least.

During this recession, bankruptcies declined during the pandemic, while prices of assets such as cryptocurrencies, stocks, and houses reached record levels. The net worth of US households increased by USD$26 trillion in 2020.

These developments are extraordinary and unusual. Usually, recessions mean severe losses rather than wealth gains. Are our current financial circumstances sustainable?

Our new report Walking the path to the next global financial crisis explains how skyrocketing public debt and monetary policy easing threaten global financial stability.

In the wake of the GFC, government bailouts of financial institutions ratcheted up public debt ratios dramatically. That was not reversed before Covid struck.

Governments and central banks in developed economies now face tough choices regarding interest rates and debt.

Raising interest rates or ending quantitative easing could destabilise asset markets and the economy. Governments, meanwhile, struggle to wind down stimulus spending and fear higher interest payments on debt.

By printing money and maintaining low-interest rates, it also fuels consumer price inflation. In New Zealand, consumer price inflation hit 4.9% – the highest level in over a decade. Inflation in the US and the EU is also approaching 6%.

The authorities are not showing a determination to return settings to more normal levels before the next economic shock occurs. They have led investors to believe that the government will underwrite high asset prices such as cryptocurrencies, stocks and housing.

It is now common to hear terms like “too big to fail” and “whatever it takes” in financial market jargon. Such beliefs are dangerous for financial stability.

For the government, it is prudent to repair the roof while the sun is still shining. Financial support packages were necessary during Covid-19. But the government should have a credible plan for reducing net debt to more sustainable levels once the pandemic is over.

The financial well-being of citizens is at greater risk when governments are less financially prudent.

As a small, globally integrated economy, New Zealand cannot prevent the next financial crisis.

We do not know when the next financial crisis will hit. But we can prepare for it when it does.

이 보고서의 제목인 “글로벌 금융위기로 가는 길(Walking the Path to the Next Global Financial Crisis)”은 얼마나 가까운 미래에 금융위기가 발생할 것인지에 논란에 대한 질문을 던진다. 그리고 상당히 근미래에 글로벌 금융위기가 발생할 수 있는 이유가 있다고 본다.

지난 25년간 뉴질랜드를 비롯한 많은 국가들은 아시아금융위기와 글로벌금융위기(GFC)라는 두 번의 전세계적인 위기의 영향을 받아 왔다. 이 두번의 금융위기는 부채 문제를 심각하게 받아들이지 않고 지속가능하지 않은 방법으로 무리한 확장을 해왔던 것이 그 원인이라고 할 수 있는데, 정부의 재정적자, 중앙은행의 안일한 통화정책, 그리고 민간금융기관의 무분별한 대출관행이 맞물려 이러한 위기를 초래했다.

코로나19팬데믹으로 인한 위기 상황에 대해 금융기관이 취한 결정들은 앞서 발생한 두 금융위기를 초래한 문제들을 답습하고 있다. 각국 정부는 활발한 경제 활동과 경기부양을 위해 위해 돈 쏟아붓기를 감행하여 부채 후유증 가능성을 높이고 있고, 중앙은행 이러한 적자 보전을 위해 자금을 마련해주었으며, 민간기관은 그로 인한 유동성이 막대한 투기적 자산 구매를 위한 대출로 이어지게 방관하고 있다.

금융시장 버블에 대해 금융정책기관들이 근시안적인 행동을 취하고 있는 것 역시 과거를 답습하고 있다. 예를 들면, 미국연방준비은행(Federal Reserve)은 1998년 장외파생상품(LTCM: Long Term Capital Management) 시장의 붕괴 이후 금융기관을 구제해 주는 결정을 내린 바있다. 그러한 개입직후, 미국회계감사원(GAO)는 그 같은 구제에 대하여 다음과 같이 평가했다.

… 연방준비은행이 대형금융기관을 대신하여 개입 할 것이라는 믿음을 줌으로서, 그 기관들이 더 많은 리스크를 감수하도록 장려한 셈이 되었다 … 연방준비은행의 개입으로 인해 사람들은 “대마불사(too big to fail)”의 신조가 확대 되었다고 우려했다 … 연방정부의 안전망이 확보되었다고 기업들이 믿게 된다면 이들이 더 리스크가 큰 사업을 추구하는 행태를 조장하게 된다.

무분별한 확장에 대한 이러한 예측은 글로벌 금융위기 이전에 이미 쓰여진 것이다. 정부, 중앙은행 및 민간부문 금융기관의 정책 방안은 대출기관과 채무자의 손해 리스크를 줄이도록 개입하는 것에 초점을 맞추어 왔는데, 이것은 자산가격 상승에 올인하는 사람들을 유리한 입장에, 반대로 보다 신중하게 접근하는 사람들은 불리한 입장에 놓이게 하는 것이다.

1984년 경제개혁 이전 뉴질랜드에서도 유사한 방향의 움직임들이 있었다. 그리고 1994년부터 2008년까지 중도좌파와 중도우파 정부들은 후속조치로 15년 연속 재정흑자를 실현한 바 있다. 그리고 뉴질랜드 중앙은행은 물가안정 또는 최소한의 낮은 인플레이션을 목표로 삼았기 때문에 정부가 막대한 재정 적자를 초래한 타국가들과는 다르게 아시아금융위기와 글로벌 금융위기를 상대적으로 잘 해결할 수 있는 위치에 있었다.

뉴질랜드정부는 글로벌 금융 위기와 코로나위기에 대한 대응으로 확장 재정정책을 실행하였고 이러한 조치는 불가피한 측면이 있었다. 글로벌금융위기 이후, 재정정책은 신중한 자세를 견지 하였으며, 또 마땅히 그렇게 했어야 했다. 다만, 앞선 두 위기와 현재의 코로나-19 대응은 중요한 차이점이 있는데, 바로 코로나 대응을 위한 중앙은행의 조치는 유동성 및 자산가격의 큰 상승을 초래했다는 점이다. 이러한 조치는 뉴질랜드를 자산가격의 붕괴 위험에 노출시키는 것이고 이것은 향후 경제적 고통을 야기할 수 있다. 지속이 불가능한 재정정책과 및 통화정책으로 인하여 금융위기 리스크에 적신호가 켜졌다.

지난 40년 동안 공공정책에 대한 경제학자들의 가르침은 “이번에도 다르지 않다(this time is not different)”는 이 보고서의 통찰력있는 메시지와도 일맥상통하다.

보고서요약

이 보고서는 글로벌 금융시스템의 안정성에 대해 경고하고, 이에 대한 근거를 제시한다. 특히 미국, 유럽연합, 영국, 일본 등의 세계 주요국가들의 최근 행보는 또 한번의 글로벌 금융위기를 초래할 수 있다. 중국의 불투명한 부채 문제에 대해서도 우려가 크다.

각 국의 주요 중앙은행들은 전례 없는 수준으로 금리를 인하하고 자산을 매입하는 양적 완화를 단행하고 있다. 1694년 이후 영국중앙은행(Bank of England: BOE)의 재할인금리가 지금처럼 낮았던 적이 없다. GDP대비 자산가치도 전례없이 높다.

대규모 정부재정적자와 극심한 국가부채가 일상화되고 있다. 재정적자와 국가부채 문제는 금리가 예년 수준으로 올라갈 경우에 훨씬 더 심각해질 것이다.

역사적으로 보면 국가부채비율은 전쟁을 치룬다든지 하는 특별한 필요에 의해서 높아졌지만, 평화 시에는 천천히 감소하는 경향을 보여왔다. 그러나 평화 시기라고 할 수 있는 지금 현재, 국가부채비율은 충격적인 수준이다.

주요 선진국에서 국가부채는 공공부문의 자산 가치를 넘어서고 있다. 이들 정부들은 납세자인 국민들의 미래를 저당잡고 있는 것이나 마찬가지이다.

현재 각국의 금융당국의 대응을 보면 2007년 글로벌금융위기(GFC) 당시의 이례적인 수준의 대응보다도 더 극단적이다. 중앙은행은 금리를 대폭 인하하고 아주 이례적인 수준으로 대출을 확대하고 있다. 다시 말해, 정부가 그들의 금융기관들에게 긴급구제금융(bail out)을 제공하고 있는 셈이다.

이러한 조치는 일견 이해가능한 면도 있으나, 미래의 큰 리스크를 야기한다. 정책결정자들은 시장원칙을 무시하고, 여론을 악화시키고, 국가부채비율 증가를 부채질하고 있다. 당국에서 이러한 비용을 고려하지 않은 것은 아니다. 다만, 그들의 절실한 과제는 고용과 경제활동의 유지였다.

Covid-19 팬데믹 이전에도 세계 주요국들은 글로벌금융위기 이전 수준으로 금융정책이 정상화되지 못한 상태였다. (예외적으로 뉴질랜드는 대부분 글로벌금융위기 이전 수준으로 정상화되었다고는 하지만, 뉴질랜드를 세계 주요국이라고 하기 어렵다). 코로나 팬데믹으로 인해 국가부채비율과 순 금융 부채(net financial liabilities)는 전례없는 수준으로 증가하였다. 이것은 톱니바퀴 효과처럼 한쪽 방향으로만 움직이게 되기 때문에 우리를 미래의 글로벌금융위기로 이끌 가능성이 크다.

인위적으로 낮춘 금리는 역효과를 낳게 된다. 인위적으로 낮은 금리는 사람들로 하여금 과대평가되고 리스크가 큰 자산을 매입하기 위해 대출을 받도록 부추긴다. 그러한 결정은 암울한 결말을 맞이하게 될 가능성이 크다. 이러한 조치들은 또한 “좀비 기업(zombie firm)”이라고 불리는 기업들, 즉 미래는 없고 부채만 많은 기업도 근근히 생명을 연장하게 할 것이다. 이 좀비 기업들은 다른 기업들이 더 잘 활용할 수 있는 자원을 점유하고 있다. 그들은 또한 정부로 하여금 더 많이 빌리고, 덜 신중하게 지출하도록 조장한다. 이것은 다 미래에 큰 비용을 치루게 된다.

이러한 최근의 현상들은 다음과 같은 질문을 낳는다. 글로벌 금융시스템이 어떻게 하다가 이 지경까지 오게 되었는가? 앞으로는 어떻게 될 것인가? 뉴질랜드 정부와 국민들은 어떻게 책임 있는 행동을 할 것인가?

첫 번째 질문에 대한 간단명료한 대답은 우리의 시스템이 정부, 금융기관 및 투자자를 금융 리스크로부터 과도하게 보호했기 때문이라는 것이다. 정부를 포함해 모든 이들은, 납세자인 국민들이 리스크에 대해 계약심사(underwriting)를 하고 있다고 여길 때 덜 주의하게 된다. 이러한 행태는 소위 도덕적 해이(moral hazard)라고 불리기도 한다.

이 문제의 원인은 애초에 설계가 잘못되었다기 보다는 상황변화로 인한 것이라고 볼 수 있다. 평화 시기의 인플레이션은 고전적 금본위제를 고수하는 국가들에서는 미미한 수준이었다. 불황 속 물가상승 현상인 스태그플레이션(stagflation)은 1971년 미국이 금본위제를 폐지한 후 발생했다. 그리고 인플레이션을 줄여야 하는 고통스러운 디스인플레이션 과정이 뒤따랐다.

1990년대에 각국정부들은 0-2% 대의 낮은 인플레이션을 목표로 하는 통화정책에 집중했고 이러한 시도들은 꽤 성공적이었다. 이 시기에는 낮은 인플레이션과 함께 완만한 경제성장이 이어졌다.

그러나 1990년대에 글로벌 금융위기의 씨앗이 뿌려지고 있었다. 정부정책은 지나치게 리스크가 큰 부동산담보대출을 조장했다. 투자자들은 자산가격이 폭락할 경우에는 미국연방준비은행이 금융기관을 지원하기 위해 기꺼이 나선다는 것을 목격했다.

‘대마불사(too big to fail)’ 및 ‘그린스펀 풋(Greenspan Put)’과 같은 용어들은 금융업계의 일반적인 문법이 되었다. 거대한 미국정부 후원기관은 모기지 관련 보안위험을 감수했다. 신용평가기관들은 리스크를 제대로 파악하는데 실패했다. 심지어는 유럽중앙은행(European Central Bank)조차도 금융시장의 추락을 피하기 위해 모든 것을 감수하겠다고 약속하였다.

반면, 일본은 다른 경로로 글로벌 금융위기를 겪었다. 일본은 1970년대 스태그플레이션을 경험하지 않은 국가이다. 다만, 일본은 급격한 부동산가격 상승을 1980년대에 겪었으며, 1990초반에는 일본 경제침체와 함께 부동산가격이 폭락하게 되었다.

일본정부는 재정적자를 감수하고서도 경제활동을 활성화하기 위해 금융정책을 폈다. 일본중앙은행(Bank of Japan)은 점점 더 극단적인 통화정책을 실시했다. 경제성장은 여전히 취약했다.

일본은 글로벌금융위기 이후에도 이와 같은 정책경로를 고수해왔으며 다른 많은 선진국들도 동일한 조치를 많이 실시했다. 자산가치가 뒷받침되지 않는 국가부채의 급증은 일상화되었다.

앞서 말한 세가지 질문 중 두 번째 질문과 관련하여서는, 앞으로 자산가격, 인플레이션, 생산량 및 실업과 관련하여 굉장히 안좋은 일들이 펼쳐질 것으로 예상한다.

정부와 중앙은행의 극단적인 조치들을 어떻게 정상화할 수 있을 것인지 대책이 없다. 일본이 먼저 이런 상황에 빠졌고 스스로 빠져나올 수 없음을 보여주었다.

정부는 재정적자를 줄일 경우 실업이 증가할 것을 걱정한다. 중앙은행들도 금리 인상을 할 경우 실업에 미칠 영향을 우려한다. 소위 “좀비 기업” 들은 분명히 도산할 것이다. 금리가 높아지면 재정적자도 증가하는데, 이는 국가부도로 이어질 우려가 있다.

통화정책은 재정정책과 점점 더 밀접하게 연결되고 있다. 이러한 통화정책의 정치화(politicisation)는 금융시장의 안정성을 크게 위협한다. 다급해진 정부는 중앙은행이 낮은 이자율로 그들의 재정적자 문제를 해결하기 원한다. 유럽 중앙은행의 국채매입은 상당한 기간 동안 이탈리아와 일부 다른 국가의 정부재정적자 수준을 초과했다. 이러한 행보는 법적으로, 도덕적으로, 경제적으로 지속 가능하지 않다.

또 한번의 글로벌 금융위기가 시작되면 자산가격이 폭락하고 금융공황상태가 야기될 것이다. 실업과 대규모파산 사태가 이어질 것이다. 극단적인 인플레이션에 이어 디플레이션 상황이 오게되면 은행예금과 현금의 가치가 파괴될 수 있다. 많은 사람들이 부의 상당부분을 잃게 될 것이다.

미래에 글로벌 금융위기가 발생하면 모든 사람들은 정부에게 파산만을 막아주도록 경기부양(keep the economy afloat)을 하도록 기대할 것이다. 정부는 정치적으로 어렵지만 꼭 필요할 결단을 하기 어려워진다. 아쉽게도 정부가 그렇게 할 수 있는 역량도 줄어들고 있다.

그렇게 되면, 유권자들은 불행한 정권을 퇴진시킬 것이다. 유권자들은 포퓰리스트 또는 독재주의 정부로 기존의 정권을 대체할 수도 있다. 실망과 불안이 따를 것이다. 예측불가능한 미래가 펼쳐질 것이다.

이것은 선진국 경제의 최악의 시나리오이다.

이보다 더 낙관적인 시나리오가 있을 수 있다. 이자율과 인플레이션이 낮게 유지되는 동안 강력하고 지속적인 경제성장이 필요하다. 또한 정부는 지출을 늘리기보다는 재정적자를 줄이기 위한 세입 증가노력을 기울여야 한다. 안타깝게도 이 시나리오는 모든 면에서 문제가 있다. 그로 인해 낙관적인 시나리오는 단순히 희망사항(wishful thinking)일 수 있다.

이 보고서는 두 가지 다른 시나리오를 고려하고 있다. 하나는 선진국 경제는 일반적으로 절뚝거리게 될 것이라는 시나리오로, 1990년대 초반 이후 일본과 같은 상황이라고 보면 된다. 경제침체가 계속되고 순공공부채비율은 GDP의 200%를 넘게 된다. 인플레이션은 최소한으로, 이자율도 낮은 수준을 유지한다.

인플레이션이 문제가 된다면 금리를 올려 채무자에게 부담을 줄 수 있다. 글로벌 금융위기를 어떻게든 피하게 되더라도 1970년대의 스태그플레이션 사태와 비슷한 시나리오가 전개될 수 있다.

뉴질랜드가 글로벌 금융폭풍으로부터 스스로를 가장 잘 보호 할 수 있는 방법은 무엇인가? 뉴질랜드 국민들은 이상적인 상황을 원할 수 있겠지만, 그런 낙관론에만 의존해서는 안된다. 앞서 설명한 세계적인 흐름는 전례가 없었다.

소국 경제(small economies)의 경우 신중한 방어조치가 거의 유일한 대안이다. 뉴질랜드정부는 다음 금융위기가 닥치기 전에 국영기관(Crown)의 순자산과 공공 순부채를 합리적인 수준까지 회복시킬 계획을 세워야 한다. 이러한 조지들은 계속적인 지출증가를 억제한다는 것을 의미한다. 독립적으로 운영되는 재정위원회가 의회에 보고하는 것이 도움이 될 수 있다. 뉴질랜드의 외환보유고 상황이 검토될 수 있는데, 특히 금 보유고에 관해 그러한 검토가 필요할 수 있다. 준비은행은 긴급구제금융을 정상화하고 금리를 인상하는 명확한 계획을 가지고 있어야 한다.

뉴질랜드 정부가 덜 신중할수록 개인차원에서 뉴질랜드 국민 개개인은 더 신중해야 한다. 현재의 가격으로 부동산이나 주식을 매수하기 위해 무리하게 대출을 감행하는 것은 개인의 미래를 가지고 러시안룰렛 게임을 하는 것과 마찬가지로 위험하다. 포트폴리오를 분산투자해야 한다. 디플레이션과 인플레이션 문제가 발생할 가능성이 모두 존재한다.

New Zealand must prepare for the next global financial crisis

New Zealand’s economy suffered less damage from the pandemic than analysts expected.

But new research warns, however, that just as we are emerging from the COVID-19, a new crisis is already on the horizon.

Walking the path to the next global financial crisis highlights the danger of an economic crash which could see asset prices collapse, businesses fail, and KiwiSaver funds and investment portfolios destroyed. Recent homebuyers may find themselves owing more on their mortgage than their home is worth.

According to the report, governments’ and central banks’ responses to the Global Financial Crisis of 2008 laid the groundwork for the next financial crisis.

With zero interest rates and money printing, asset prices have soared, consumer prices have risen, and public debt has reached dangerous levels globally.

The world’s politicians and central bank governors are now struggling to return to more normal policies. The result is an economically perilous future.

Former Reserve Bank of New Zealand chair Arthur Grimes warns in the foreword to the report there may be only a short time before the next financial crisis. “Central bank actions through the pandemic … have placed New Zealand at greater risk of an asset price collapse with ensuing economic pain; the risk is heightened by the unsustainable fiscal and monetary policies globally,” Grimes writes.

The Government must prepare for the next global financial crisis, even though New Zealand is too small to prevent it. The prudent course is to reduce debt, both public and private.

The Covid-19 financial support package has kept Kiwis off of the dole queue and saved many businesses from bankruptcy. However, the government should promptly repay those debts in order to be prepared for the next financial shock.

Failing to prepare now for the next financial crisis could destroy New Zealanders’ nest eggs and threaten their livelihoods.

We’re on a slope where monetary policy has become increasingly ineffective in promoting real economic growth. Every crisis was met with monetary easing that caused debt and other imbalances to accumulate over time, and that caused the next crisis to be bigger than the previous one.

William White, Former Chief Economist of The Bank of International Settlements

Cracks on the Wall in 2021

A few weeks ago, US Secretary of Treasury Janet Yellen announced that the US government is heading towards default if Congress does not lift its ‘debt ceiling’. As we all know from economic history, the default of the United States would be a catastrophic ‘financial Armageddon’. With the US being the largest economy in the world, this is alarming news.

On the other side of the world, China’s second largest property company, Evergrande is facing a debt crisis. The default of Evergrande may have potential spillovers with the residential market being worth 29% of China’s GDP (Rogoff and Yang, 2020). Excess leverage of the Chinese corporate sector does not spell financial confidence. Some are claiming that this is potentially a Chinese ‘Lehman Brother’ bubble bound to pop like the 2007-08 global financial crisis (GFC).

In Europe, since the advent of Covid-19, the European Central Bank bought virtually all the government bonds (quantitative easing) of European countries like Italy and kept its interest rates at zero percent. No private investor is willing to buy government bonds at this stage. The only market players in this area are central banks.

Something strange is happening across the world economy. We are witnessing imminent cracks in the global financial system. It’s difficult to predict what may occur in the next few months or years, but one thing is clear – the global economy is extremely fragile. The net worth of many individuals and households are bound to crash sooner or later.

There are strong correlations between populism (both left and right wing) and the 2007-08 global financial crisis. (By Ingram Pinn for The Financial Times).

Introduction

Virtually everyone understands that getting into excess debt leads to trouble. Whenever someone sees a ‘red’ balance in their bank accounts, they panic and try to do everything they can to either lower their deficits or pay back the debt. Financial circumstances matter to people. Saving before spending is the common wisdom. This logic applies to governments too. Except they have the ‘printing press’ with government-controlled (or owned) central banks to fill their coffers (as lender of last resort), on top of tax revenue.

Whilst it may be true to claim that governments are different to individuals and households, its economic decisions have significant consequences on our livelihoods.

It’s been a year since the Covid-19 pandemic began. In contrast to last year’s 3% economic contraction, the International Monetary Fund (IMF) projects that the world will face positive economic growth of 6% for 2021 (IMF, 2021). It seems that high vaccination rates are allowing cities and regions to get out of lockdowns. The United States, the United Kingdom, the European Union and other parts of the world are opening up to the rest of the world. In hindsight, financial circumstances appear better than 2020.

However, there are serious questions as to whether this will be the case in the medium term. In response to the Covid-19 pandemic, many governments across the developed world have accumulated debt levels well-beyond their annual economic output (Gross Domestic Product – the value of every single thing sold on every single shelf around NZ and the value of every single person who worked for a whole year) and the net worth of these governments are heavily in the negative (considering the assets and liabilities of governments).

Table 1: Net Worth of Governments

Country

2016

United Kingdom

-141

Finland

-109

United States

-69

Austria

-41

Canada

-29

Germany

-22

Australia

-21

Switzerland

12

South Korea

41

New Zealand

46

Norway

384

As of 2016, governments were already under in the heavy negatives (IMF, 2018)

This is an unprecedented level of debt during peacetime. Instead of fiscal surpluses, we have so far witnessed the exact opposite from governments. Unfortunately prudence is not a popular term for government officials. Low interest rates from central banks induced more governments to borrow more money. They decided to get the money now instead of the future. Instant gratification took precedent over delayed gratification.

In addition, central banks across developed economies printed trillions of dollars out of nothing to stimulate the world economy away from the recession. They also lowered its interest rates to zero-bound levels. In essence, central banks have made borrowing extremely cheap for everyone, including governments. But the such low interest rate levels are unprecedented.

Spending has become easier. Saving money is not rewarded. Inflation undermines the real value of the dollars in your bank account. This forced individuals to speculate in the stock market or the housing market for a decent return. Unproductive zombie firms have been propped up without falling, forcefully maintaining low unemployment levels without ‘creative destruction’ (Banerjee and Hofmann, 2018, 2020)

But what happens if these markets face downturns again later? Everyone may lose everything. Can they react in a similar manner to the GFC of 2008 or Covid-19? Are bailouts from governments even feasible? I’m not entirely sure.

This is why governments and central bank policies matter to all of us. This essay will explore the few key variables that culminated into the current state of financial affairs. The moral hazard problem; the public debt precedent set by the 2007-08 GFC; the doubling down of debt with the responses to Covid-19 and finally the potential long-term ramifications of these responses.

In times of uncertainty, policymakers pursued these policies for correct short-term reasons, but the decisions have created unintended consequences for the future. Central Banks cannot raise interest rates, nor can they suck the printed money out of the system for fears of creating a worse recession. They are now stuck at a corner by kicking the ‘recession’ can to the future. In the words of former Federal Reserve economist Bill Dudley, central banks are “running out of fire power” (Dudley, 2020).

The decisions in response to the pandemic were understandable. In the face of uncertainty, it is entirely rational to have pumped money into the economy, and to have spent billions on the wage subsidy and other fiscal programmes across the developed world – including New Zealand.

But the net consequences is that the financial system does not look healthy or sustainable. In contrast to optimistic scenarios, the reality is that the world is at a crisis point.

Overall, the decisions by governments and central banks have created a financial system that is chugging along entirely on the “excessive build-up of debt” (White, 2021). This is unsustainable and a form of a financial crisis will loom the world soon. It is uncertain how this next crisis will occur, but economic history tells us that risk is always present (Reinhart and Rogoff, 2009).

We will explore the reasons why that is the case. The origins of the problem started with the end of the stagflation period under Paul Volcker.

The Rise of Moral Hazard

The only way to contain the economic damage of a financial fire is to put it out, even though it’s almost impossible to do that without helping some of the people who caused it.

Ben Bernanke, Henry Paulson and Timothy Geithner, on their policy responses to the GFC

Moral hazard is a common economic term used to define human behaviour when people get incentivised to take more risks for greater profit at the expense of the other party. Another term for this is the ‘principal-agent problem’. For example, if I have health insurance I have the incentives to be more careless with my health, assuming the insurance company will bail me out when I need heart surgery based on my heart attack. It’s the problem of taking more risk when you are not as personably liable.

On similar grounds, beginning with the Federal Reserve Chairman Alan Greenspan, central banks intervened in the economy whenever there was a downturn in the stock market. In contrast to health insurance where there is a risk premium demanded by these companies, what Greenspan did was essentially bail out investors and financiers for free repeatedly. Under Greenspan, the Federal Reserve intervened by lowering the Effective Federal Funds rate during the 1987 stock market crash, the 1994 Mexican peso crisis, the 1997 Asian Financial Crisis, the collapse of Long Term Capital Management and the dotcom bubble in 2000 (Rudd, 2009). By easing monetary conditions whenever there was a downturn, he propped up the stock market and economic activity. Essentially, the Fed was providing free insurance to investors. During his reign between 1987 and 2006, he was world renowned for presiding over the ‘Great Moderation’ period of moderate economic growth, low unemployment, low inflation and ‘managing’ the global economy well.

But if you continue bailing out the people that fail, they are more likely to make riskier decisions, assuming a massive profit by taking that risk. Why wouldn’t they!? The Fed had their backs. The higher the S&P 500 went, the more riskier investments they made. We see this in the growth of new financial products in the likes of subprime mortgages market (Mortgages lent to people that do not have the collateral, capital or employment to buy homes, but loaned out on the basis of higher risk. These were sliced and diced into non-risky assets into the form of Collaterized Debt Obligations) and credit default swaps (financial instruments purchased on the assumption that other parties will fill for bankruptcy, which is essentially a bet) during this era. This was a timebomb in the residential sector that was bound to fall, but for the medium term, as long as house prices continue to go up, things looked rosy. Then the global financial crisis happened beginning in 2007.

The Road to High Government Debt Levels: GFC 2007-08

New Zealanders might recall the tumultuous period during the 2007-08 GFC. The fall of Lehman Brothers and other financial institutions across the stock market left investors in panic mode. The financial ‘cancer’ of subprime mortgages and CDOs spread to the entire global financial system. Banks such as Northern Rock in England faced bailouts from the British government and the Bank of England. With the help of the Federal Reserve, the United States had to spend USD$1.5 trillion in bailouts and tax cuts to stimulate the economy and stir away from the global recession. It was a transfer of a banking crisis into a public debt crisis.

Alongside the Federal Reserve in the United States, other central banks – such as the ECB, the Bank of England and the Bank of Japan – begun the process of what economists call quantitative easing (the printing of money) and reducing their interest rates to low record levels. This was to save the economy from falling into further recession.

Millions of people lost their homes, life savings and their livelihoods. Many people became unemployed and lost jobs – some even permanently became redundant. It was an extremely unpleasant sight at the time. Alan Greenspan’s reputation had tarnished completely.

It affected the New Zealand economy as well. NZ unemployment jumped from 3.6% in 2007 to 6.1% by 2010. As a response, under both the Fifth Labour government and Fifth National government, we pursued fiscal stimulus programmes. Thanks to our prudent fiscal measures beginning in 1994 to 2008, we were able to respond well. Under John Key’s National government, our government debt levels went up from 5.4% debt to GDP in 2008, to 25.4% of GDP by 2014. The Reserve Bank under then- Governor Alan Bollard dropped interest rates by 5.75% to stimulate the New Zealand economy (Bollard and Ng, 2012). New Zealand did not need to pursue quantitative easing.

According to Ben Bernanke (the former Federal Reserve Chairman and successor to Greenspan), it was imperative for policymakers in American ‘to do everything it takes’ to stop the world economy facing a modern ‘Great Depression’. They bailed out financial institutions bound to fail, they provided liquidity to the US Treasury by purchasing government bonds and rapidly expanded their balance sheets. The total assets of the Fed increased from USD$1 trillion to USD$2 trillion by 2009, and the Federal Funds rates at 0.75 as indicated in Figure 1.

Under Obama, the US Federal government pursued fiscal stimulus programmes such as the American Recovery Reinvestment Act of 2009. This programme alone added USD$840 billion to the budget deficit. As indicated Figure 2, the federal debt held by the public ballooned from 35.7% in 2008 to 75.9% of GDP by 2017, which is more than double before the GFC.

Other economies such as The European Union, the United Kingdom, Japan and other developed economies spent their way out of the problem. The banking crisis originating in American transformed into a public debt crisis across the developed world (except for fiscally prudent nations such as Australia and New Zealand), culminating into a sovereign debt crisis in Europe – also known as the 2011 Euro crisis.

The GFC revealed excess public borrowing. Countries in Europe such as Greece, Portugal, Ireland, Spain and Cyprus were unable to repay or refinance their debt obligations to their bond holders. Many looked to other European Union member states for financial assistance or even bail outs. An extreme example is Greece. The small Southern European country received series of 100 billion euro bailouts from the International Monetary Fund and the European Union (Voigt, 2012). Germany was the most generous of lenders. Yet despite this, Greece defaulted in 2015 (and is currently barely staying afloat with Greek government debt levels remaining well above 100% at 210% of GDP as of 2021). Many European economies are also floating along thanks to the financial support from prosperous economies such as France and Germany, and low interest rates from the European Central Bank.

Figure 3 shows that governments have been induced to borrow more as interest payments continue to decline. The European system is not healthy by any means. Debt levels and leverage are far too high, encouraged by central bank intervention and help from other countries.

Figure 3:

Euro zone general government net interest cost and financial liabilities (OECD, 2021).

In conclusion, the responses to the GFC saved the global economy facing an economic depression. However, this came at a cost. The banking crisis turned into an inevitable public debt (or sovereign debt crisis). In the United States, public debt continued to accumulate with little indication of deleveraging or fiscal restructuring. Meanwhile, Greece created political and economic turmoil in Europe, amalgamating into populist sentiment in Europe. With the Brexit vote in 2016, the European Union and the euro currency’s future remains uncertain.

If the Greek default created such geopolitical turmoil, imagine what the circumstances would be if any of the major G20 economies face financial trouble. In addition, the initial quantitative easing from central banks restarted the economy following the GFC, but it incentivised governments, households, companies to all take more debt rather than less. The world essentially buckpassed the financial crisis to the future as a short-term band aid. Then in 2020, Covid-19 hit the world starting in Wuhan, China, forcing governments and central banks to make drastic decisions.

The Fiscal and Monetary Consequence of Covid-19

The supply shock to the global economy came from a pandemic. Governments and central banks again took swift decisions. The fiscal and monetary responses to Covid-19 were very similar to the GFC, except the scale and size of the quantitative easing from central banks and deficit spending of governments were far larger. For the Euro zone the average gross financial liability levels were close to 120% of GDP. The United was 141% and the United States was 146%. Under President Biden, the US Federal government’s fiscal deficit was 15.9% of GDP for 2021. For the Euro zone on average it was 7.2% and New Zealand was 4.2% deficit (OECD, 2021). Before in 2008, the ratio of global household, corporate and government debt to GDP was 280%. As shown in Figure 4, in response to the pandemic, in 2020, this ratio had grown by 75% to355%(IIF, 2021). The world has now mortgaged our future by getting into more debt now.

Figure 4:

Global Debt Monitor: COVID Drives Debt Surge—Stabilization Ahead? (IIF, 2021)

Governments around the world have never spent this much money in response to a pandemic in peacetime. The deficits created during the 2007-08 GFC look miniscule in comparison.

In monetary policy, the central banks have pumped more money and liquidity into the system than ever before, shown in Figure 5. ‘Trillions’ are being swashed around the global financial system (For context, 1 trillion is five and a half times New Zealand’s GDP). Bank rates are now virtually zero around the world – see Figure 6. The banks have little firepower left to tackle another financial crisis later down the track. Monetary policy has become less effective as a result of all of these responses beginning from the GFC.

When the United States and the rest of the developed world entered zero-bound rates during the GFC, former Bank of Japan Governor Masaaki Shirakawa noted that when Japan was adopting zero bound interest rates and quantitative easing policies beginning in the early 1990s, he never expected other countries such as the United States to follow suit (Shirakawa, 2014).Yet, other central banks did, and they all entered a road of no return.

Conclusion

The global economy has entered a cross road, unable to turn back towards a period of relative normalcy. Starting with the fiscal and monetary responses to the GFC, governments have accumulated record debt, and central banks lowered its rates and printed money to stir the economy away from prolonged recessions. We have kicked the can down the road to an even more precarious future.

Both governments and central banks are stuck into a corner. Governments’ cannot stop spending, because otherwise unemployment rates would erupt; central banks cannot lift rates for the fear of sovereign default and collapses of heavily indebted companies. The public cannot stop buying inflated assets with the ‘fear of missing out’. Rising inflation and low interest rates incentivise people to stop saving and risk their future wealth through speculation. All of these government responses create bad incentives across the whole global economy.

On monetary policy, the late macroeconomist John Maynard Keynes wrote in 1936 that “If, however, we are tempted to assert that money is the drink that stimulates the system to activity, we must remind ourselves that there may be several slips between the cup and the lip.”

The effectiveness of monetary policy has now been nullified with rates close to zero percent. What can central banks do to respond to the next crisis? Bailouts? Further quantitative easing? Economists cannot predict the future, but we can anticipate risks from recent trends.

Contemplating that future is bleak. The era of normalcy following the end of the Cold War seems like a distant past. The period of ‘normal’ interest rates and sustainable debt levels seem implausible at this stage. The trends have been towards more debt, lower rates and more money printing. What will governments and central banks around the world do? And more importantly, when will this madness end? We will soon find out in the near future.

References

Alan Bollard and Tim Ng, “Learnings from the global financial crisis,” Sir Leslie Melville Lecture, Australian National University, Canberra (9 August 2012).

Alan Rappeport, “As debt default looms, Yellen faces her biggest test yet,” The New York Times (23 September 2021).

Bill Dudley, “The Fed Is Really Running Out of Firepower”, Bloomberg (28 October 2020).

Emre Tiftik and Khadija Mahmood, “Global Debt Monitor: COVID Drives Debt Surge—Stabilization Ahead?” Institute of International Finance (17 February 2021).

International Monetary Fund. “IMF Public Sector Balance Sheet Statistics: Database.”

Kenneth Rogoff and Carmen Reinhart, This Time is Different (Princeton University, 2009).

Kenneth Rogoff and Yuanchen Yang. “Has China’s Housing Production Peaked?” China & World Economy 29:1 (2021), 1–31.

Kevin Rudd, “The Global Financial Crisis”, The Monthly (February 2009).

Kevin Voigt, “Eurozone approves new $173B bailout for Greece,” CNN (21 February 2012).

Mark Dittli, “Central banks keep shooting themselves in the foot,” Interview with William White, The Market (6 November 2020).

Masaaki Shirakawa, “Is Inflation (Or Deflation) ‘Always and Everywhere’: A Monetary Phenomenon? My Intellectual Journey in Central Banking,” BIS Paper 77e (2014).

Matt Egan, “‘Financial Armageddon’. What’s at stake if the debt limit isn’t raised,” CNN Business (8 September 2021).

OECD.Stat.

Ryan Banerjee and Boris Hofmann, “Corporate Zombies: Anatomy and Life Cycle,” BIS Working Papers No. 882 (2020)

Ryan Banerjee and Boris Hofmann, “The Rise of Zombie Firms: Causes and Consequences,” BIS Quarterly Review (2018)

The Economist: “How should recessions be fought when interest rates are low?” (21 October 2017).

US Federal Reserve, “Federal Debt Held by the Public as Percent of Gross Domestic Product.”

US Federal Reserve, “Credit and liquidity programs and the balance sheet.”

William White, “It’s Worse than ‘Reverse’: The Full Case Against Ultra Low and Negative Interest Rates,” Working Paper No. 151 (New York: Institute for New Economic Thinking, 2021).

Yardeni, and Mali Quintana. “Central Banks: Monthly Balance Sheets” (Yardeni Research, Inc. 2021).

In the past 30 years we’ve witnessed the end of the Soviet Union, the third wave of democratisation and extensive levels of globalisation. Mass flows of capital and mobility have become the norm. Francis Fukuyama predicted the ‘End of History’ with liberal democracies spreading around the planet and market capitalism enriching everyone.

To some extent this became a reality. Steven Pinker’s Enlightenment Now shows empirical studies of great benefits brought to the world by globalisation. We live in a richer, healthier and more peaceful era than ever before.

However, drastic changes to the global economy and mass migration resulted in a backlash against cosmopolitanism. 9/11, the global financial crisis of 2008, the Euro crisis of 2011, the failures of the Iraq War and the refugee crisis of 2015 cumulatively left Western liberal democracies politically precarious. The rise in domestic inequality, offshoring of low skilled work, and declining trust in political and financial institutions led to worsening social cohesion.

These unexpected circumstances of events led us to a world of increasing populist sentiment evidenced by Brexit and President Trump’s election — the revival of nationalism.

John Mearsheimer stated that “nationalism is the most powerful ideology on the planet”. Humans are tribal and we are social animals to the core. This explains the zealous dedication people exert towards national causes which seek to advance identity-based policies.

Contemporary populism is a symptom of the problem and not necessarily the solution. We have to defend the liberal world order, but future policy-makers should consider dealing with the side effects of globalisation.

To sustain an interconnected and a peaceful modern world, we must understand the causes of populism and continue to build towards a society where we embrace liberal democratic principles.