New Zealand’s two major political parties, National and Labour, are losing popular support. The latest 1News Verian poll had a combined total for both parties of only 61 percent, among the lowest since the introduction of our MMP electoral system.

Their polling weakness reflects a deeper failure: neither party has provided compelling economic answers to the country’s long-term challenges.

People are frustrated with NZ’s left for confusing more government spending with the delivery of quality public goods, for pretending that redistribution can provide abundance for all, and for equating centralisation with state capacity.

There is equal frustration with NZ’s right for confusing fiscal austerity with economic growth, deregulation with productivity, and small government with better government.

Neither approach has worked. Successive National and Labour governments have left us with a high cost of living, sluggish economic growth, shallow capital markets, fiscal pressures from population ageing, and low savings.

That is why National’s recent announcement on compulsory KiwiSaver matters. It is a courageous admission, from our largest centre-right party, that market forces and voluntary savings alone cannot solve our problems.

The political revival of our major parties requires them to think beyond their own conventional wisdom. A distinctly new reformist agenda is needed, building on the best of competitive markets and personal responsibility, while using strong institutions to support universal savings, productive investment and broader ownership.

Compulsory KiwiSaver is not merely a retirement policy. It comes with other implications. It points to a more fundamental question that neither party has answered: “what kind of capitalism should NZ build for the next generation?” The answer is influenced by our economic inheritance, which both parties still operate under.

During the eighties and nineties, Finance Ministers Roger Douglas and Ruth Richardson, under Labour and National governments, oversaw the dismantling of an exhausted protected economy. They achieved successes – averting a currency crisis, lowering inflation, restoring fiscal discipline and opening the economy.

But their reform style also caused serious damage. Welfare spending was cut during a recession. State-owned assets were sold, which caused greater market concentration. The cost of living rose. A third of the population with no savings were locked out of high-asset markets and left to their own devices.

The historical mistake was to turn a necessary period of liberalisation, designed for a specific crisis, into a permanent “catch-all” neoliberal prescription for every problem.

Even though our country performed reasonably well in the OECD afterwards, we failed to match Australia’s economic growth – let alone economies like Singapore and South Korea.

Unlike New Zealand, Australia never treated market liberalisation as the whole economic project. Instead, it only marked the start of a broad national development strategy.

By combining gradual market reform with compulsory superannuation in 1992, Australia successfully turned wages into a savings pool for investment. The result is now AU $4.5 trillion under management.

New Zealand liberalised. Australia capitalised.

That is the missing element of our reform story. We never built an equivalent national savings architecture to create a deep pool of domestic capital to support productive investment and broaden wealth to include those left behind. Without deeper domestic capital markets, it is harder for new firms to scale, challenge incumbents, and place pressure on concentrated sectors.

As presciently analysed by former Reserve Bank Governor Graeme Wheeler, New Zealand relied too heavily on housing, foreign capital, immigration, construction, tourism and primary exports as the engines of growth. That model is no longer enough.

Compulsory KiwiSaver will not solve every problem, but it marks a departure from the old economic reflexes that have dominated National and Labour thinking. It is neither old-fashioned socialist nostalgia nor libertarian fantasy, but the beginning of an asset-owning capitalism in which everyone shares.

For younger New Zealanders, this matters enormously. Generation Z and young Millennials are inheriting unaffordable housing and scant savings, whilst being asked to fund an ever-larger number of elderly with higher taxes. They are being asked to pay more of the future bill without being given the tools to own part of that future.

Universal KiwiSaver does not fit neatly under either old-fashioned ideology. It may not be the end of the debate, but it does symbolically mark a new future for Kiwi capitalism.

Leonard Hong is an economist based in Auckland who has a Master’s degree in International Political Economy from the Nanyang Technological University, Singapore (2024). He is a leadership network member of the Asia NZ Foundation, an executive member of the Korea-New Zealand Business Council and a former adviser to former Minister of Commerce Hon. Andrew Bayly

The National Party’s KiwiSaver announcement is one of the most significant shifts in New Zealand politics and economic policy in a generation.

“We are delighted that the Prime Minister has agreed to implement compulsory KiwiSaver if re-elected in this year’s election.”

“For the past few years, we have been advocating for compulsory savings through our opinion pieces, public commentary, and Leonard’s postgraduate research from Singapore. We saw it as one of the most compelling macroeconomic policies that can help New Zealand become a rich, asset-owning country with deeper domestic capital markets and a stronger external position.”

“The lesson from Australia’s compulsory superannuation system and Singapore’s Central Provident Fund is clear: mandatory savings can deepen capital markets, reduce the long-term fiscal burden of public pensions, and create pools of capital that support investment in national development.”

“As presciently analysed by former Reserve Bank Governor Graeme Wheeler, New Zealand has for too long relied on housing wealth, high immigration, international tourism, and primary sector exports as the main engines of growth since the 2008 Global Financial Crisis. That model is no longer enough.”

“In contrast to economic policies advocated by libertarians, New Zealand needs a comprehensive economic strategy to diversify its economy, and one approach is to develop greater domestic capital and expand public assets, including KiwiSaver and the New Zealand Superannuation Fund.”

“The National Party’s commitment to KiwiSaver development signals an important shift in economic thinking. It recognises that New Zealand cannot build long-term prosperity under the status quo of heavy reliance on foreign capital, house price inflation, and chronically low household savings.”

“For a centre-right government to accept compulsory KiwiSaver is a major philosophical shift. It recognises that personal responsibility sometimes requires strong institutions and pragmatic paternalism to incentivise higher capital accumulation.”

“This unorthodox economic approach provides a more seamless pathway out of a fiscal crisis, and in stark contrast to rapid increases in taxation, monetisation of public debt, or harsh fiscal austerity measures.”

“Today’s announcement by the Prime Minister is not the end of that debate, but it may be the start of a new economic consensus.”

Leonard Hong is an Economist at the University of Aucklandwith a Master’s degree in International Political Economy at Nanyang Technological University, Singapore with the support of the Prime Minister’s Scholarship for Asia

Professor Robert MacCulloch is the Matthew S. Abel Chair of Macroeconomics at the University of Auckland.

Former Australian PM Paul Keating, right, pictured here in 2016 with his predecessor Bob Hawke, brought in mandatory retirement saving in Australia.

New Zealand’s rapidly ageing population is putting increasing pressure on the Government’s budget, with threats of large cuts in welfare, or tax hikes, or both.

Mandatory savings, as have been successfully modelled by both Australia and Singapore, could help ease the burden without undermining our state pension, NZ Super.

Australia’s former Labor Prime Minister Paul Keating enacted mandatory savings in 1992, supplementing an existing mean-tested pay-as-you-go public pension. He says its advent slashed reliance on taxpayer-funded pensions.

With a contribution rate of 12 percent, and on the back of compound interest, Australia’s Super wealth is estimated to reach $8 trillion by 2035, becoming the second largest in the world (after the US).

Singapore also has mandatory savings, managed by the Central Provident Fund. The institution is lauded globally with around NZ$876 billion assets under management. Both superannuation and healthcare are provided through mandatory individual accounts.

Meanwhile, 19 years after New Zealand’s voluntary KiwiSaver was set up, a low default rate of employer and employee contributions equal to 3 percent of wages (from 2009 to 2025) has meant average balances nationally now sit at about $41,000.

Mandatory accounts were set up in Chile in 1981, although under dictatorship without democratic mandate. Similar models later spread through Latin America and Eastern Europe, but many countries reversed course after the 2008 global financial crisis, shifting back towards optional state systems or abandoning individual accounts altogether.

Why have so many governments refrained from ensuring individuals build greater savings to fund their own welfare needs? Particularly in retirement, and given that public welfare is in such jeopardy?

In New Zealand, there are three reasons why politicians have been unwilling to implement mandatory savings to bolster the state pension.

First, because many policymakers and thinkers across both left and right political ideology have opposed it. Second, because none of the political parties have produced a well-supported plan for how to make the change in a way that doesn’t hurt average workers financially. Third, because of myopia in political decision-making underestimating compound returns.

Although Prime Minister Helen Clark’s government promoted savings through introducing KiwiSaver in 2007, a mandatory scheme was a step too far for her party. This may be related to suspicions about ‘privatising welfare’.

Many politicians on the left in New Zealand still prefer to prioritise reliance on a public pension.

Some politicians and academics on the left worry that making KiwiSaver compulsory would eventually undermine NZ Super, by prompting governments to introduce means-testing arguing that retirees with significant savings no longer need the full pension.

Mandatory savings have also not sat comfortably with National Party ideology either. When KiwiSaver was first proposed, then-National Opposition leader Sir John Key called it a ‘glorified Christmas club’. His party voted against KiwiSaver.

Although the current coalition Government increased minimum KiwiSaver contributions by employees and employers from 3 percent to 3.5 percent in 2026, it also ended subsidies and amended the KiwiSaver Act to create the new first-home withdrawal option.

Proposals for mandatory savings reform usually require employees, employers or both to contribute more. But those extra payments don’t replace taxes. They sit on top of them. That means people could end up paying both: contributions into KiwiSaver and taxes that fund NZ Super, leaving workers with less.

So how might reform in this area win majority support?

Former Australian PM Keating says the political feasibility of his reform depended on including it in a package of tax and tariff cuts, and a shift to union enterprise bargaining through agreements with the Australian Council of Trade Unions.

In his 1995 Budget, he proposed 3 percent tax cuts would be paid into people’s superannuation accounts to raise contributions by 3 percent. That left government with a revenue shortfall, so to keep fiscal balance it came with cuts in areas receiving government support.

This could be done in New Zealand by targeting high-income groups receiving welfare, such as tertiary students from wealthy families on interest-free loans and fee subsidies, winter energy subsidies to the wealthy, screen production grants for big-budget films, and accelerated depreciation allowances to chosen industries.

This would be met with fierce political resistance. The ending of movie subsidies was met with threats to go elsewhere, even though grants totalling $300 million have already been made for Avatar films and Amazon’s Lord of the Rings franchise.

Whatever one’s views on the best structure for our pension system, relying on each young generation to support the elderly with taxes is, more than ever, threatened by the size of our ageing population. Neither the right nor left in New Zealand have provided an answer.

But mandatory savings have been shown to work in nations like Australia and Singapore. They provide an unorthodox but a more seamless pathway out of fiscal crisis, and in contrast to rapid increases to taxation, monetisation of public debt, or harsh fiscal austerity measures.

Leonard Hong is an Auckland-based economist and a student at the University of Auckland Business School

Professor Robert MacCulloch is the Matthew S Abel Chair in Macroeconomics at The Business School of the University of Auckland

Why are nations failing to resolve the fiscal crisis caused by population ageing? Many economies are struggling with rising costs to the government budget of pension and healthcare due to population ageing. A potential solution is greater emphasis on mandatory private savings so future generations are not so dependent on a dwindling proportion of youth to pay taxes to support their welfare needs. However, few nations have buttressed Pay-As-You-Go (PAYG) public systems the past two decades in this way. We use New Zealand as a case study to highlight three salient political-economy barriers. First, ideology leads many right wingers to oppose mandatory savings due to a desire not to curtail personal economic freedoms, as well as left wingers who prefer reliance on State pensions. Second, politicians have been largely unable to design reforms that minimize loss of current disposable income to the median voter as savings are built for workers, whilst at the same time PAYG pensions are continued for the existing retired paid out of current taxes. Third, the long time period required to deliver significant savings boosted by compound returns deters politicians with short horizons.

For many New Zealanders, Singapore may still feel like a stopover city or a gleaming business hub. But as global tensions expose just how vulnerable small economies can be, the relationship is taking on much greater significance. Drawing on his own experience studying in Singapore, Leonard Hong explores why this city-state has become one of New Zealand’s most important strategic partners, and what Prime Minister Christopher Luxon’s recent visit reveals about trade, trust and resilience in an increasingly uncertain world.

When I was a postgraduate student at Nanyang Technological University in 2023, I had an interesting realisation. My Singaporean friends, when they learned I was a Kiwi, would often recall their time in Matamata visiting Hobbiton or talk about following the All Blacks from Singapore. Some also reminisced about past trips to Queenstown and Milford Sound.

What stuck with me, however, was how many Singaporeans described Kiwis as “very friendly.”

Leonard with his friends in Singapore. Image credits – Leonard Hong/AMC

In a more uncertain world, the relationship between our two countries is becoming increasingly important to our economic security and resilience. Singapore is one of New Zealand’s closest and most trusted partners outside our Trans-Tasman relationship with Australia.

Recent tensions in the Middle East and pressure on global energy routes have reminded New Zealand how exposed we are to disruptions far from our shores. In an increasingly fragile and unstable global economy, New Zealand needs strong international partners that share our values and can support one another in times of crisis. Both countries believe strongly in a credible multilateral system that upholds the rule of international law.

Singapore matters to New Zealand not only because it is wealthy, well governed, and strategically located, but because it is a partner we can rely on in a world where shocks are becoming more frequent. Fuel, food, shipping routes, supply chain resilience, defence cooperation, and diplomatic trust all underpin this bilateral relationship.

What’s Actually at Stake in This Visit

It is a special relationship, not only at the government-to-government level, but also through business, education, tourism, and people-to-people ties. We saw this directly in the warm rapport between Prime Ministers Christopher Luxon and Lawrence Wong at the Singapore-New Zealand Leadership Forum last week.

Closer ties at all levels, including through Track II diplomacy, will only benefit both countries in the years ahead.

In trade, the two countries complement each other well. New Zealand’s abundant natural resources allow us to provide daily essentials, including dairy, meat, and even water. Singapore, by contrast, has developed world-leading industries such as advanced manufacturing, logistics, and petrochemicals, built on human capital and innovation.

Crucially, New Zealand imports 33 per cent of its refined fuel from Singapore, and Singapore is our fourth-largest trading partner. Meanwhile, 28 per cent of Singapore’s dairy imports and 14 per cent of its food imports come from New Zealand.

We are a critical partner for a city-state that relies almost entirely on international trade for its survival. Both countries depend on one another for economic security and essential supplies, as recent concerns over the Strait of Hormuz have demonstrated.

The Agreement on Trade in Essential Supplies (AOTES), announced by the New Zealand and Singapore governments, may seem like a technical arrangement, but it matters. It gives legal weight to a simple idea: in a crisis, trusted partners should keep essential goods moving.

The agreement creates a binding framework to help keep supply chains open between the two countries. More importantly, it builds on the trust we have developed over decades and provides legal assurances that our two small, open economies can continue to thrive in an increasingly uncertain world.

Many New Zealanders admire Singapore’s infrastructure, public administration, savings system, and long-term planning. Image credits – Leonard Hong/AMC

How Singapore Might Be Viewing New Zealand

From my observations, Singaporeans see New Zealand as a close and trusted partner with whom they have maintained diplomatic relations for more than 60 years.

As Singapore’s Prime Minister Lawrence Wong put it: “Singapore and New Zealand share many strategic perspectives. We have long seen the world in similar ways. We believe in openness and cooperation. Over the years, we have built a deep reservoir of trust. And we do not just speak about principles; we act on them.”

Both countries also have qualities from which the other can learn.

Many Singaporeans see New Zealand as a society that places greater emphasis on wellbeing, life satisfaction, and quality of life. Our natural beauty, lakes and mountains, and rich indigenous heritage through Te Ao Māori are often viewed as culturally dynamic and inclusive.

New Zealand’s open spaces, slower pace of life, and strong education system appeal to Singaporean families seeking a different lifestyle balance. Singapore, in turn, offers world-class institutions such as the National University of Singapore, a highly regarded civil service, and leading financial institutions like DBS Bank.

At the same time, many New Zealanders admire Singapore’s infrastructure, public administration, savings system, and long-term planning.

The relationship works partly because each country sees something in the other that it can learn from.

Leonard with Professor Kishore Mahbubani, Distinguished Fellow, Asia Research Institute at National University of Singapore

What This Could Mean for the Relationship Going Forward

In recent years, Singapore’s economy and society have attracted growing attention in New Zealand. I have often advocated for compulsory KiwiSaver by pointing to Singapore’s highly successful Central Provident Fund savings system.

Following his visit, Prime Minister Christopher Luxon noted that New Zealand could learn from the Singapore Story, particularly in areas such as infrastructure and urban development.

Any lessons, of course, would need to be adapted to New Zealand’s own democratic, social, and institutional context.

The relationship between the two countries is likely to evolve on two fronts.

First, governments, both current and future, will continue identifying policy lessons that can help New Zealand remain economically competitive and strengthen ties with one of our most important partners.

Second, the partnership will deepen through trade agreements and closer alignment on foreign policy.

And Importantly, Why People Here Should Care

New Zealanders should care about Singapore because it is one of Asia’s most successful economies and one of our most important strategic partners.

Last year, the two countries celebrated 60 years of diplomatic relations, and the partnership is likely to grow stronger as both small, open economies navigate major geopolitical headwinds.

For many New Zealanders, Singapore may still feel like a stopover, a business hub, or a place admired for its efficiency. But it is much more than that.

It is one of our most important partners in Asia, a country that understands the vulnerabilities of small, open economies and a reminder that prosperity depends not only on markets, but also on trust, preparation, and resilient institutions.

Singapore and New Zealand are not just friendly countries. We are two small, open economies trying to remain secure and prosperous in a more uncertain world.

In an era of greater geopolitical risk and increasingly fragile supply chains, Singapore is no longer just a useful partner for New Zealand. It is a strategic one.

Leonard Hong is an experienced political economist with a focus on macroeconomics, international economics, urban development and public policy. He has a Master’s degree in International Political Economy from Nanyang Technological University in Singapore. He is a Leadership Network Member of the Asia NZ Foundation and NZ Prime Minister’s Scholar for Asia.

Last week, after returning to New Zealand from Singapore, Prime Minister Christopher Luxon strongly argued that “we have serious work to do on our infrastructure” compared to Singapore.

It’s public knowledge that ministers in the coalition Government admire Singapore’s economic policy approach.

The Prime Minister admires its long-term planning for development; Winston Peters wants a national infrastructure fund, emulating Temasek Holdings, and has advocated for compulsory savings, like Singapore’s Central Provident Fund (CPF) system; Deputy Prime Minister David Seymour similarly wants mandatory health accounts inspired by the CPF.

It’s not just the Government.

The Opposition under the Labour Party announced, “The Future Fund”, also partially influenced by Singapore’s sovereign wealth funds (SWFs), to “invest in infrastructure and innovative Kiwi businesses to create good, secure jobs”. The Green Party admires Singapore’s high urban density and world-leading public transport system.

The real issue is not New Zealand politicians’ admiration for Singapore, but that they cite Singapore’s successes without adopting the rigorous policies that led to the “Singapore Story”.

We have not witnessed much progress in most policy areas, and there is little congruence between words and action.

If New Zealand politicians invoke Singapore as a model, they must honestly acknowledge what underpins Singapore’s achievements – high savings, strict fiscal discipline, effective infrastructure execution, talent attraction, meritocracy, and strong state capacity. Unless we commit to these fundamentals, talk of emulating Singapore remains empty.

So, what is the secret behind Singapore’s success, and what policy lessons can it offer to boost New Zealand’s economy?

The first difference is their national savings record and fiscal discipline.

Singapore has built strong financial and fiscal institutions for accumulating national capital through compulsory savings, with its world-leading CPF system and sovereign wealth funds, GIC and Temasek Holdings.

The CPF system requires citizens to save up to 20% of their wages, with another 17% provided by their employers, and the total asset under management is around SG$661 billion ($876b). Both superannuation and healthcare are provided through mandatory individual accounts.

Temasek Holdings manages over SG$434b, while the Government Investment Corporation handles nearly SG$1 trillion. The Net Investment Returns Contribution of SG$20b funds government spending, about what Singapore spends on education annually.

Singapore has maintained an annual average budget surplus of SG$8.4b over the past three years, supported by strong economic growth and windfall tax gains. Singapore is a capital-exporting nation with zero net debt.

Conversely, New Zealand’s KiwiSaver means employees save only 3.5%, with employers contributing a further 3.5%. More than 20% of Kiwis do not have a KiwiSaver account or don’t save. Our total funds under management are only $143b, which is far below both Australia’s compulsory superannuation and Singapore’s CPF funds.

Worse, many Kiwis are withdrawing from KiwiSaver due to financial hardship. Despite the OECD’s advice, we continue to tax savings through the Employer Superannuation Contribution Tax.

Our NZ Super Fund is world-class, but its total size is $86b, which is far smaller than any SWF in Singapore.

Meanwhile, since the Covid-19 pandemic, both sides of politics contributed to the massive increase in public debt, with net core Crown debt rising to 44%.

Interest payments have increased to close to $9b. At the same time, the Government has made costly short-term commitments while borrowing remains elevated and tax revenue weakens.

New Zealand’s debt is expected to blow out to 200% by 2065, driven by population ageing and exponential increases in healthcare and superannuation, which are already crowding out discretionary spending. Even if we achieve a surplus by 2029, the long-term projection shows we are headed for a fiscal crisis.

Singapore funds long-term investment through its accumulated national wealth. In contrast, New Zealand relies heavily on foreign borrowing, has low household savings, and a weak KiwiSaver system. Our national savings rate lags far behind Singapore’s, yet there is no effort to improve domestic capital formation.

The second difference is execution. Singapore’s success is not just about prudent public finance. It is about state capacity in turning public policy into project development.

Singapore’s success is rooted in the Urban Redevelopment Authority’s centralised planning model. Its “whole-of-government” co-ordination ensures technical requirements are clear, approvals are rapid, and land-use decisions are treated as essential infrastructure. The results are Changi Airport, Marina Bay Sands and Jurong Industrial Estate.

Since the establishment of the Ministry of Regulation, few regulatory changes have meaningfully reduced compliance costs. The new Planning Act and Natural Environment Act aim to enable more development, yet do not improve the government’s regulatory execution. New Zealand’s development remains hampered by complex consenting requirements, inconsistent political decisions, and an over-reliance on public relations and consultants rather than on technical expertise.

New Zealand’s main challenge is not a lack of goals but weak implementation. Our failure to execute, in contrast to Singapore’s disciplined execution, is the real obstacle to progress.

The third difference is talent acquisition and meritocracy.

The city-state treats talent as a crucial national asset. Singapore aggressively recruits “top-tier” global talent to build new industries and companies, thanks to its low corporate tax rates and a pro-business regulatory environment.

The Government invests heavily in elite institutions, hires foreigners deemed “the best and the brightest”, and places a high value on technical excellence in government and the corporate sector. Both the National University of Singapore and Nanyang Technological University rank in the top 12 in the QS rankings supplemented by major government investments, while competing with Ivy League institutions.

Singaporean academic Kishore Mahbubani credits meritocracy for Singapore’s success. “Meritocracy is the first reason for Singapore’s success.” At its best, meritocracy means selecting people based on abilities rather than nepotism, patronage, family ties or political convenience. We see this with the credentials of various Singaporean politicians and corporate leaders who hold degrees from Ivy League institutions and Oxbridge colleges.

In contrast, New Zealand’s migration settings do not attract the best and the brightest.

Around 180 young Kiwis around my age are leaving for overseas each day. Some argue that this is identical to the past, but this time is different. Faith and trust in our country are fading fast.

Our universities lack support, and none compete globally. The Government ignored the University Advisory Group’s recommendations – led by Sir Peter Gluckman – for advancing our universities.

Furthermore, New Zealand is moving towards a culture that under-rewards excellence. Our public service and corporate boards are now frequently populated by generalist managers and consultants rather than subject-matter experts. By devaluing the “best and brightest” in favour of soft skills, we risk losing the rigorous execution capacity we had in the late nineties.

The Government has indicated and signalled its intention for an ambitious future for New Zealand. However, actions speak louder than words.

The policies under the current coalition Government have not reflected its intention to emulate Singapore’s best practices nor “fix the basics”. Neither has the Opposition presented its proper costings, economic analysis, or alternative solutions to these long-term structural challenges.

Consequently, our economic trajectory is diverging further from Singapore. Singapore’s real GDP grew at an average 3.5% per year from 2023. Meanwhile, New Zealand’s real GDP grew at a meagre 0.6% during the same period. We are experiencing one of the lowest growth rates among OECD countries.

I accept that Singapore is not a model to be copied, but it offers public policy lessons that can help us fix our productivity woes and relative economic stagnation.

Singapore’s success isn’t just a vision; it’s the result of relentless fiscal discipline and state capacity. If our political leaders want to follow their lead, they need to stop talking about the destination and start prioritising transparent budgeting, strict expenditure controls, and building effective public institutions.

Singapore envy is not an economic strategy.

Leonard Hong is an economist based in Auckland who has a Master’s degree in International Political Economy from the Nanyang Technological University, Singapore (2024) with the support of the Prime Minister’s Scholarship for Asia. He is a leadership network member of the Asia NZ Foundation and a former adviser to former Minister of Commerce and Consumer Affairs Hon. Andrew Bayly

Last week, NZ First leader Winston Peters announced his party’s bold proposal to make KiwiSaver compulsory by supporting employers through tax cuts and raising the contribution rates to 10% of wages.

This was politically significant as it puts savings reform at the centre of our economic policy debate. Peters is correct in stating that New Zealand should become a rich asset-owning country through high domestic savings rather than desperately try to rely on foreign direct investment for growth.

Deeper and more broad-based domestic capital markets provide stability and reduce vulnerability to external shocks.

Unfortunately, compared to other advanced economies, New Zealand is woefully behind in the area of retirement income, domestic savings and use of private funds to increase our investment in assets such as hospitals and infrastructure.

As one of the many young Kiwis who left to go to Australia, I am stunned by our Trans-Tasman neighbour’s financial wealth. It greatly exceeds NZ, even after adjusting for their larger population size.

Australia’s Sovereign Wealth Fund, called The Future Fund, has NZ$350 billion in assets under management.

Meanwhile, their compulsory superannuation system is world-leading. Total accumulated funds are currently NZ$4.6 trillion. It is expected to become the second-largest savings pool in the world by 2050 and is 35 times larger than total KiwiSaver balances. Every Australian has an account. Individually their balance averages 10 times the balance in one of ours.

Astonishingly, around 20% of Kiwis don’t have a KiwiSaver account, and no savings at all.

The Australian scenario would not have been possible without solid and competent political leadership. Former Australian Prime Minister Paul Keating introduced Compulsory Superannuation in 1991 to “reduce the future reliance on the age pension, and over time, give ordinary people a better retirement”. Employer contributions started at a compulsory 3% of wages per year and gradually increased to the 12% where they sit today.

Thanks to compulsory superannuation, Australia is the only country across the OECD expected to have its government old age pension spending decrease from 2.3% of GDP today to 2% of GDP by 2060. By contrast, New Zealanders’ demand on the public purse to fund our pay-as-you-go pension system is projected to rise from 4.9% to 7.7% of GDP by 2060.

There is a common theme that emerges from such comparisons. Countries that create strong compulsory savings systems can reduce the fiscal burden of public pensions and also create pools of capital which they then have available to invest in the country’s national development.

After leaving NZ to study for a master’s degree in Singapore, I was amazed to learn about the city-state’s unorthodox social security and public asset system. Its development is deeply rooted in Singapore’s national savings schemes. The country’s Central Provident Fund requires citizens to save up to 20% of their wages – with another 17% provided by their employers. It currently has NZ$834 billion under management.

Singapore’s Sovereign Wealth Funds manage more than NZ$570 billion through Temasek Holdings and NZ$1.3 trillion through the Government Investment Corporation.

Singapore’s economy is expected to continue remaining the crown jewel of Southeast Asia. It is a capital exporting nation with a current account surplus and net zero debt.

Australia and Singapore have both taken the path of focusing on long-term capital accumulation through use of sovereign wealth funds and compulsory saving schemes. It is time New Zealand follows suit.

Many older Kiwis know about how former Prime Minister Sir Robert Muldoon made an awful mistake by abolishing the compulsory superannuation scheme set up under Norman Kirk in 1974.

Peter’s new savings proposals may mark the new beginning of a bipartisan agenda for NZ’s future public asset development.

Politicians across the spectrum support this transition. Labour’s David Parker said in his valedictorian speech, “[Australia’s] universal work-based savings [is] why those clever Aussies own their banks plus ours, our insurance companies, and much more. It’s why their infrastructure is better, their current account deficit lower, their net international liabilities lower, and their growth rate higher.”

Former National Party Commerce Minister Andrew Bayly also understood the vitality of higher domestic savings. He said, “One largely untapped source is the $109 billion of capital held by KiwiSaver providers… By comparison in Australia, I understand roughly 15% of its $3.8 trillion pension fund industry is invested in alternative assets, such as private equity and infrastructure.”

Now, NZ First has proposed a policy to ensure KiwiSaver becomes a major economic vehicle for our future economy. There are gripes about the fiscal costs of the tax cuts needed to buttress compulsion – including me – but the idea behind the policy is sound.

New Zealand stands at a crossroads. Our low domestic savings rate, combined with our ageing population, poses a long-term fiscal challenge that cannot be ignored.

The late Harvard economist Martin Feldstein’s words still ring true, “The problem with the current system is that retirees’ benefits are financed on a ‘pay-as-you-go’ basis, by taxing concurrent employees. The obvious solution is to shift to a privatised system of pre-funding those benefits through mandatory contributions to individual accounts.”

Many analysts argue that foreign capital can drive investment, but as other nations have now successfully demonstrated, mandatory savings systems supplemented by Sovereign Wealth Funds strengthen not only financial stability but also productivity and national independence.

As far as I know, there are no options to addressing long-term fiscal debt problems for a country like NZ other than by hiking taxes, printing money, defaulting, or cutting public services, or by promoting domestic savings through policies that support schemes like KiwiSaver and our Super Fund.

Which one do you prefer?

Leonard Hong is an economist based in Perth, Australia who has a Master’s degree in International Political Economy from the Nanyang Technological University, Singapore (2024) with the support of the Prime Minister’s Scholarship for Asia. He is a Leadership Network Member of the Asia NZ Foundation.

The assessment of the long-term fiscal position of the United States by Harvard’s Martin Feldstein in 1997 can be applied to most of the developed world today. The ‘pay-as-you-go’ comprehensive social security system that became popular during the early period of the Keynesian Consensus supporting retirement income and healthcare is already unsustainable. Unfortunately, because of the inevitable trend of population ageing, long-term unfunded liabilities – financial obligations from governments to citizens with insufficient funds to cover future projected costs – states will be required to spend far more on healthcare and pension (Goodhart and Pradhan, 2020). In response, various governments pursued a myriad of policy options – and failed so far – to tackle this inevitable trend, including tweaks in the system including increasing the retirement age, indexation of pension and in some cases compulsory private savings towards self-provision.

The crucial question is how to accomplish and resolve this looming problem. Some suggest imposing significant tax increases – such as capital and wealth taxes favoured by the left – or cutting expenditures to an extent that undermines the poorest members of our society without an alternative safety net – which is the libertarian argument. The former option supported by the Green Party will push capital out of the nation, undermine our economy, and at best raise barely any revenue. The latter commonly from the ACT Party does not provide any alternative solutions beyond the status quo. Sentimental push from economists towards “faster productivity growth” is not a solution either (Wilkinson, 2024). In my view, there is no alternative but to prioritise raising domestic savings in New Zealand (NZ) towards supporting economic development. New unorthodox thinking and economic approach is required to resolve the challenges facing New Zealand, beyond the left-right political divide.

In response to the relatively interesting – but flawed – analysis by economist Michael Reddell (2025), this essay seeks to counter the arguments provided on the topic of savings. These were the following main arguments and points from Reddell’s article:

Economic growth has been stagnant and some analysts – including Leonard Hong – have argued for higher domestic savings and Reddell questions their conclusions.

Compulsory savings have not led to significant productivity gains and believes other variables are more important to economic success.

Reddell argues that Australia’s spending on retirement income is still relatively high for the old age pension – which is means-tested – and national savings has not risen to the extent he anticipated and productivity is nowhere near the level of the United States.

Singapore’s national savings did not play as much of a major role in the city-states’ substantial part in their economic success, but rather more from its global competitiveness and low tax settings.

The role of foreign capital and domestic capital on economic growth is still under debate, and Professor Robert MacCulloch’s argument on the “Feldstein-Horioka puzzle” is interesting, but not entirely convincing.

Savings rates are often a response to investment opportunities rather than a cause; therefore, Reddell questions the notion that low domestic savings constrain investment in countries like New Zealand.

I broadly support the idea of mandatory savings – mainly because of its pragmatism and simplicity but also the positive spillover effects as outlined from my previous academic work examining Singapore’s economic model centred around the development of public assets (Hong, 2024). Furthermore, numerically higher domestic savings increase the capital available for investment, which translates to investment in infrastructure, businesses, and innovation, and therefore higher productivity. Other scholars provided potential and feasible alternatives based on mandatory savings across various nations such as Singapore, Chile, Sweden, and Australia (Feldstein, 1998; Kotlikoff and Burns, 2004; Ferguson, 2008; Micklethwait and Wooldridge, 2014; Chia, 2016; Douglas and MacCulloch, 2018).

These are the main reasons why I have repeatedly called for a bipartisan political approach to public asset development, in the form of both supporting our KiwiSaver and our sovereign wealth fund, the NZ Superannuation Fund (NZ SuperFund). New alternative state investment vehicles in the form of institutions such as the Accident Compensation Corporation have also provided social and economic benefit to the NZ public. In contrary to Reddell – and others – I will argue that higher domestic savings, supported by a structured compulsory savings system, is essential for New Zealand’s long-term economic prosperity.

Productivity and the Role of Domestic Savings?

The productivity puzzle in NZ has been widely examined across society. Former NZ Prime Minister John Key suggested the cause of our productivity woes was our “geography” – which is in line with Jared Diamond’s (1997) argument on what mainly distinguishes rich and poor countries. Other scholars including Nobel laureates Acemoglu and Robinson (2012) highlighted the quality of political and economic “institutions”. Huntington and Harrison (2000) provided a cultural perspective on economic development and productivity, especially on aspects of work ethic, meritocracy and openness to innovation. I broadly agree with all these theories – especially the institutional argument – but the point is that the debate on what improves productivity has always a puzzle for scholars and policymakers. I am strongly convinced that higher domestic savings – complemented by overseas investment – boosts economic growth and productivity.

Australia’s Productivity

Reddell mentions that Australia’s compulsory superannuation systems set up by Paul Keating has not led to higher net national savings as anticipated despite the policy mandating private savings for retirement on the public. To his credit, it is true that savings have not been as high, but this is attributed to the ‘substitution’ incentive for Australians to borrow more money under the assumption their wealth will accumulate through their superannuation (Connolly and Kohler, 2004). This was previously examined by many behavioural economists such as Daniel Kahneman (2011) on the ‘present and status quo biases.’ However, by in large, academic studies in Australia show that compulsory superannuation still led to increases in net savings broadly (Ruthbah and Pham, 2020).

Despite the relatively mediocre net savings, Reddell points out that Australia is much wealthier than NZ with a much higher GDP per capita of around USD$20,000 stating, “Australia is, by the way, the most culturally and behaviourally similar country to New Zealand in the world.” (Isn’t the fact that the author of this essay is working in Australia somewhat ironic?). His comparison between Australia and the United States may not fully account for the unique factors that influence their economies, such as the role of the US dollar as the world’s reserve currency. Furthermore, if the United States government followed Martin Feldstein’s advice of “large-scale compulsory saving”, perhaps they would not be in such a dire fiscal situation of US$37 trillion of net government debt – culminated from the unnecessary and costly wars in the Middle East.

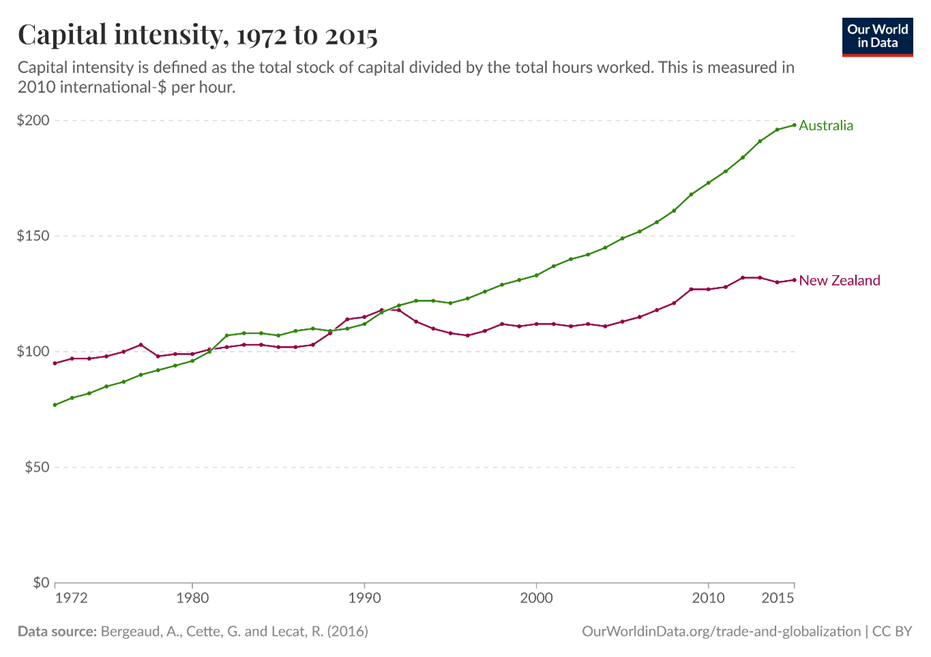

In relation to the comparisons with NZ, there are two major variables in my view that distinguish the two countries – iron ore and the superannuation funds sector. The former, we have limited control over – although depending on the agenda of NZ Resources Minister Shane Jones – but the latter, there is greater potential for reform.

Figure 1: Capital Intensity, 1972 to 2015

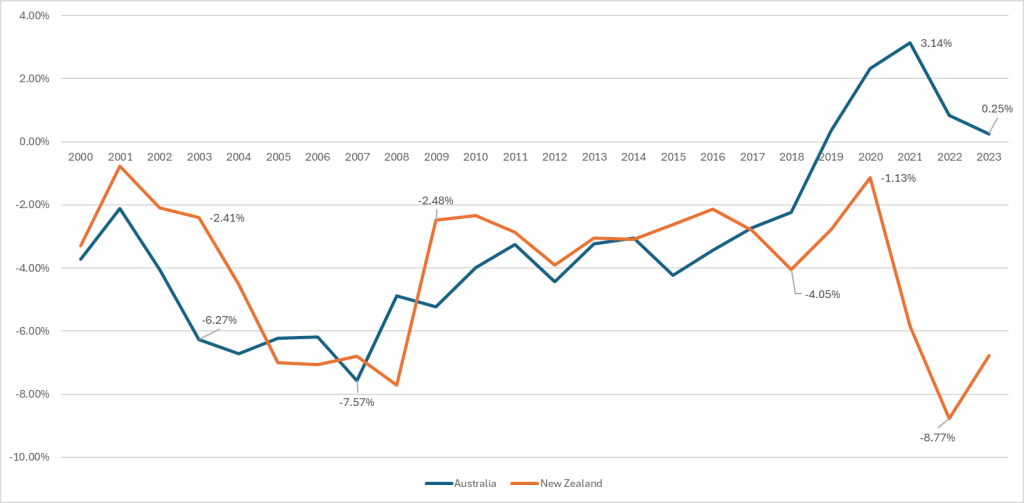

The superannuation system now manages more than AUD$4.1 trillion under management which is the fourth largest savings pool in the world which comprises of 150% of Australia’s GDP – which is expected to become the second largest savings pool by 2050. This is remarkable for the 55th largest nation in the world. This pool of capital translated to rapid increases in capital intensity for the Australian economy. As shown in Figure 1, from World in Data, the specific critical juncture was from 1991, which was when Australian Prime Minister Paul Keating decided to introduce Compulsory Superannuation to “to reduce the future reliance on the age pension, and over time, give ordinary people a better retirement.” (Keating, 2013). He had the foresight and prescience to understand that demographic pressure was inevitable. Therefore, setting up a mandatory savings scheme would allow the system to transfer more from a ‘pay-as-you-go’ system towards a ‘self-provision’ based system. To Keating’s credit, the call on the budget from the old age pension dropped from 5% of GDP in 1991 down to around 1% in 2023. Secondly, in stark contrast to NZ, Australia recently had some periods of current account surpluses starting in 2019 without needing the begging bowl to foreign investors being capital poor. However, as shown by Figure 2, there is not much difference between Australia and NZ with both countries, and I concede that this is probably the weakest point of comparison in my analysis. The differences in economic scale, trade composition, and external sector dynamics significantly influence their respective balance of payments. Although I do consider the historical hypotheticals if Keating’s original plan of raising the compulsory savings rate beyond the 9.5% to 15% was actualised, especially given that Coalition governments have frequently prioritised tax cuts over further superannuation expansion (the Morrison government did eventually raise it to 12%).

Figure 2: Australia vs NZ – Balance of Payments in Proportion to GDP, 1989 to 2023 (World Bank Data)

I am not arguing that in the short-run a current account surplus or deficit is inherently good or bad – in the long run possibly – but it is clear that Keating’s policies led to the structural transformation of Australia’s economy. Despite later Coalition governments pursuing tax cuts over further superannuation expansion, much of the accumulated savings under Keating’s framework were directed toward domestic investment, funding major infrastructure projects such as the Port of Melbourne and Transurban Toll Roads. For higher productivity focusing on capital markets, NZ can only grow by boosting both domestic savings and allowing more foreign capital into the country which will consist of cutting actual red-tape to FDI through supply-side reforms – which Reddell strongly agrees with me – and ramping up domestic savings through KiwiSaver – or other private saving investment vehicles (MacCulloch, 2024). The current National Coalition government’s emphasis has been on attracting overseas investment whilst broadly ignoring the problem of domestic savings so far.

Singapore’s Productivity

Reddell rightly praises Singapore’s economic miracle with the city-state having one of the highest per capita GDP in the world. However, he claimed that “it would be very hard indeed to argue that national savings played any very substantial part in Singapore’s economic emergence.” I believe this perspective overlooks a critical component of Singapore’s economic strategy, which was deeply rooted in their national savings system as a fundamental part of economic policy for current Singaporean politicians (Lee, 2024). Whilst the Central Provident Fund (CPF) was set up in the 1950s, it was an inherent part of the Singapore government’s fiscal strategy. Lee Kuan Yew (2000, p.97) stated he not only maintained the compulsory nature of the system but regularly raised the contribution rates to “avoid placing the burden of the present generation’s welfare costs onto the next generation.” Furthermore, according to Lee (2000, p.102-103), the critical aspect is to ensure bare minimum fiscal pressure on the state to avoid the ‘buffet syndrome’, a fact which Reddell omitted when publishing his article:

Through the CPF system, Singaporeans have access to a comprehensive self-financing social security fund comparable to any old-age pension system or entitlement system in the Western world without transferring the burden to the next generation of workers (Micklethwait and Wooldridge, 2014; Chia, 2016; Douglas and MacCulloch, 2018). The Singaporean government understood the importance that every generation should contribute to their own pension and every individual should save for their own without burdening the state. CPF has a major role on Singapore’s economy – Reddell is incorrect. The whole entire purpose was fiscal discipline which is important for long-term economic growth and macroeconomic stability (Reinhart and Rogoff, 2009).

Secondly, Reddell cites comprehensive data concerning Singapore’s current account position and national savings record in proportion of GDP from the International Monetary Fund. The question from him was the notion that the Singapore government relied on current account deficits in the early period of the 1970s and 1980s for its growth. Indeed, it is true and there is a specific reason. The East Asian Miracle – particularly in Singapore – shows that savings and investment are not separate, but interconnected variables in driving economic development.

Reddell should have considered the extensive work by development economists on the East Asian Miracle, where the initial phase of development focused on attracting foreign capital to acquire the necessary talent, business expertise, and technological spillovers that enabled these countries to build their own capabilities in the long run. This approach, championed by various economists that studied the East Asian developmental state model (Stiglitz, 1996; Chang, 2003; Rodrik, 2015; Haggard, 2018). While these nations initially relied on foreign investment, they eventually became capital-exporting economies after reaching a certain level of development and establishing competitive domestic companies and ‘national champions’. High domestic savings were critical in fostering capital formation for the Four Asian Tigers, which, in turn, led to productive investment and long-term growth.

Figure 3: Singapore Government’s NIRC and Budget Deficits/Surpluses (S$ Millions)

Furthermore, Reddell didn’t mention the importance of sovereign wealth funds for Singapore, but it is relevant to the argument in this essay – it was covered extensively across my postgraduate dissertation. Singapore relies heavily on endowment funds provided by the Government Investment Corporation (GIC) and Temasek Holdings, called Net Investment Returns Contribution (NIRC). For example, in the 2024 Budget, the Singapore government received S$23 billion through the NIRC, comprising 18% of the revenue – 3.4% of GDP. This fiscal mechanism has many benefits since it allows the state to be ‘developmental’ such as public investments in infrastructure, housing, and education, but also tax breaks for new start-ups, capital allowance on depreciable assets, 250% tax deduction on R&D expenses, low corporate tax rate of 17%. The pro-business settings – including tax breaks that Reddell gives a fair bit of credit to Singapore – was possible because of their net zero debt position with massive amount of financial assets – worth US$1.9 trillion owned by the public. As shown in Figure 3 – which is from my dissertation – seven of the ten last government budgets saw the NIRC contribute an overall surplus, despite eight budgets having a primary structural deficit.

Conclusion

In conclusion, I disagree with the premise of the article that was published by Michael Reddell. I fully support Martin Feldstein’s remarks from 1997 that the “obvious solution is to shift to a privatised system of pre-funding those benefits through mandatory contributions to individual accounts.” I do not see another alternative policy approach to tackle this looming macroeconomic problem. The mainstream economic approach currently tinkers around the edges. The status quo – even with the NZ SuperFund – will be fiscally inadequate as highlighted by the NZ Treasury’s Long Term Fiscal Position forecasts. I suggest that moving to a hybrid system like Australia with a means-tested old-age pension would be the next step by incrementally raising the minimum contribution rates to KiwiSaver – either employee or employer – as highlighted by the Retirement Commission (Katz, 2024). Andrew Coleman (2024) recently highlighted the major issue of designing the new system towards “intergenerational neutrality” without harming the younger generation to continue to pay for retirees and at the same time build a nest-egg for their future. This major issue of intergenerational fairness is a very tricky and puzzling problem for transitioning from our current ‘pay-as-you-go’ system towards a social security system based on ‘self-provision.’

Both examples of Australia and Singapore show that high domestic savings matter to a large extent on both macroeconomic stability and economic performance. I also do not see ‘domestic savings’ in a similar way to Reddell that “savings themselves are endogenous.” Savings are not entirely endogenous but can be nudged and supported through policies that incentivise individuals and households towards more private savings and investment. The fact is that NZ has one of the lowest domestic household savings across the developed world is worrisome. Therefore, reversing the trend is critical, not only for our long-term fiscal position but also our economic prospects in the future. We should be attempting to emulate parts of what Australia and Singapore have done, instead of labelling such policy proposals as ‘paternalistic’ or ‘authoritarian’.

Reddell’s statement that “retirement income policy should be approached on its own terms, with a focus on individuals and their own ability to manage retirement,” is a simple classically liberal philosophical position. The only difference from my end is suggesting that people mandatorily save rather than forcefully pay high tax rates! The state already compels the public to pay income tax, and GST, so what is the difference between taxes and being compelled to save money? A high return on private savings is achieved by investing in high-performing investments with compound interest, whereas taxes are simply a means of generating revenue for the state.

NZ is currently discussing the importance of attracting more foreign direct investment. I broadly agree that we need to make it easier for capital from overseas to invest into NZ equities, companies, land, industrial development, housing supply and our chronic infrastructure deficits highlighted by the Infrastructure Commission. However, there is a limit to this strategy as higher concentration of foreign capital also risks financial instability and tends to lead to slower growth than countries that have higher proportion of domestic savings (Prasad et al, 2007; Cavallo et al, 2016). And this idea was partially supported by Reddell who concluded in the latter part of his article stating:

Indeed, higher domestic savings by-in-large would have a positive effect on the current account, put less demand on the NZ dollar, support more exports and allow more Kiwis to accumulate foreign reserves and become a capital exporting nation.

The notion of having more savings on an individual and household level makes sense as a financial buffer and social insurance during times of personal difficulty. The prudent decision is to limit credit card debt and refrain from buying unnecessary items or making “vanity” purchases of luxury goods with credit cards. If every Kiwi behaved and understood finance like Warren Buffett and Charlie Munger, then we would not be having these policy discussions. Unfortunately, most of the NZ public do not have the appetite let alone the long term orientation or foresight to consider making sound financial decisions. If we apply this logic on a macroeconomic level, most of the readers will be able to comprehend as to why a lot of people – including myself – are advocating for mandatory savings. Former NZ Commerce Minister Andrew Bayly was pursuing important policies to kickstart financial education across our school system and I hope new Minister Scott Simpson completes the job. The average balance of NZ$38,000 for KiwiSaver is utterly woeful and nowhere enough to save for retirement – let alone purchasing a house.

I decided to respond in a comprehensive manner with this essay because Reddell is one of the most well-known economic commentators and analysts in NZ, and I have tremendous respect for his work. His compelling research with Dr Don Brash and Dr Bryce Wilkinson for the 2025 Taskforce was very useful with insightful economic suggestions. Anyone interested in economic policy should have a read – as well as his excellent blog. The debate regarding domestic savings is a necessary one, but I am confident that history will prove people such as myself to be correct in the long run.

NZ stands at a crossroads. Our low domestic savings rate, combined with an ageing population, poses a long-term fiscal challenge that cannot be ignored. Some may argue that foreign capital broadly can drive investment, but the examples of Australia and Singapore demonstrate that a comprehensive mandatory savings system not only strengthens financial stability but also boosts productivity and national resilience. In my humble opinion, there is no economic policy alternative to addressing the long-term fiscal debt problem, economic growth and productivity problems besides developing more public assets and boosting domestic savings through policies that support schemes such as KiwiSaver and the NZ SuperFund.

References

Acemoglu, Daron., & Robinson, James. (2012). Why Nations Fail: The Origins of Power, Prosperity, and Poverty. New York: Crown Publishing Group.

Cavallo, Eduardo., Eichengreen, Barry., & Panizza, Ugo. (2016). “Can Countries Rely on Foreign Saving for Investment and Economic Development?” IDB Working Paper No. IDB-WP-718. Retrieved from https://ssrn.com/abstract=2956698

Chang, Ha-Joon. (2003) Kicking Away the Ladder: Development Strategy in Historical Perspective. London: Anthem Press.

Chia, Ngee-Choon. (2016). Singapore Chronicles – Central Provident Fund. Singapore. Straits Time Press.

Feldstein, Martin. (Ed.). (1998). Privatizing Social Security. Chicago: The University of Chicago Press.

Ferguson, Niall. (2008). The Ascent of Money: A Financial History of the World. London: The Penguin Press.

Goodhart, Charles., & Pradhan, Manoj. (2020). The Great Demographic Reversal: Ageing Societies, Waning Inequality and an Inflation Revival. London: Palgrave Macmillan.

Haggard, Stephen. (2018). Developmental States: Elements in the Politics of Development. New York: Cambridge University Press.

Harrison, Lawrence., & Huntington, Samuel. (Ed.). (2000). Culture Matters: How Values Shape Human Societies. New York: Basic Books.

Hong, Leonard. (2024). “Lessons from Singapore on getting the Government’s books in shape without paying more tax.” The New Zealand Herald.

Hong, Leonard. (2024). “Savings and Sovereignty: Comparative Political Economy on Fiscal Discipline and Public Asset Management between Singapore and New Zealand.” Postgraduate Dissertation for NTU.

Kahneman, Daniel. (2011). Thinking, Fast and Slow. New York: Farrar, Straus and Giroux.

Kotlikoff, Laurence., & Burns, Scott. (2004). The Coming Generational Storm: What You Need to Know about America’s Economic Future. Cambridge: MIT Press.

Leonard Hong shares his experience of studying in Singapore on a Prime Minister’s Scholarship for Asia.

I strongly urge students to apply for the Prime Minister’s Scholarship for Asia, it was one of the best decisions of my life.

As an undergraduate student at the University of Auckland in 2019, I finished the autobiography by former Singaporean Prime Minister Lee Kuan Yew, From Third World to First: The Singapore Story: 1965-2000. This book ignited my fascination with Singapore. From that point, I had in my mind that one day I could study or live in Singapore in order to gain a deeper understanding of the economic miracle it has achieved.

Fast forward five years later, I was able to realise both objectives. I just completed my postgraduate degree at the S. Rajaratnam School of International Studies (RSIS) in Nanyang Technological University, Singapore. With its entrepreneurial dynamism and open international economy, I was lucky to have lived in this remarkable nation. I am grateful for the opportunity as it provided me with a world-class education with a much better understanding of Singapore’s political economy as well as other Southeast Asian countries.

Some friends asked me before, “Why International Political Economy, Leonard?” I have always responded that solving complex global and domestic challenges requires an interdisciplinary understanding of political science and economics. I thought the Master of Science degree offered by RSIS would allow me to build a more comprehensive analytical framework with better technical skills.

Gardens by the Bay.

Furthermore, Singapore was a perfect place to study for me as a global financial hub of Southeast Asia reliant on international trade and investment. New Zealand has a similar demography with low corruption and pro-business practices. Singapore’s approach to governance and public policy offers valuable lessons, adaptable to our unique local context.

My dissertation topic considered the fiscal implications of its domestic savings scheme and how that translated to its accumulation of public assets – sovereign wealth funds – and its private pension schemes. I compared and contrasted Singapore with New Zealand and uncovered certain setbacks within our approach. I was able to get coverage from the New Zealand Herald’s Liam Dann’s business column on my comparative political economy analysis as well as publishing a column myself on the New Zealand Herald arguing against a capital gains tax. It was gratifying to contribute to policy debates back home, even from abroad.

The timing of my programme was also impeccable. I was fortunate to meet New Zealand Prime Minister Rt Hon. Christopher Luxon and Minister of Climate Change Hon. Simon Watts in Singapore as part of their Southeast Asia trip in April fostering greater trade and investment across the Indo-Pacific region. Their choice of Singapore as the first destination outside Australia was significant to me.

With Professor Tommy Koh.

I also had the opportunity to meet various policymakers and public intellectuals from Singapore. I had a quick meeting with Minister of State Alvin Tan about his portfolios and responsibilities. Conversations with Professor Kishore Mahbubani on US-China relations and the future of ASEAN were enlightening. I also was very honoured to meet Professor Tommy Koh who graciously signed his book for me during our conversation.

With Dr Anne-Marie Schleich for book launch.

Moreover, I served as the master of ceremonies for the launch of a new book edited by Dr. Anne-Marie Schleich—Senior Adjunct Fellow at RSIS and former German Ambassador to New Zealand—titled Perspectives of Two Island Nations: Singapore-New Zealand. This event, co-hosted by the New Zealand High Commission in Singapore, RSIS, and World Scientific Publishing, was one of the first books directly comparing and contrasting public policy in New Zealand and Singapore.

My time abroad in Singapore well-exceeded my expectations. I met various famous Singaporeans in my field of interest, networked and built a new cohort of friends for life and my understanding about Southeast Asia expanded significantly. This experience made me more resilient, adventurous, and globally minded. It taught me the importance of cultural understanding and empathy in solving global problems.

With Singaporean Prime Minister Lawrence Wong.

I encourage more students and professionals to consider studying in Singapore and building connections to contribute back to New Zealand. I share my story not for its own sake but to motivate others to pursue similar opportunities, learn, grow, and explore Singapore’s unique and unorthodox policy approaches.

The Treasury, in its briefing to incoming finance minister Nicola Willis, said a comprehensive capital gains tax would generate more tax revenue to help balance the Government’s books.

But can’t prudent fiscal policy be achieved in other ways?

Singapore provides some answers.

A couple of weeks ago, the city-state’s finance minister Lawrence Wong released the 2024 Budget.

As with other countries, immediate social spending and investment were prioritised in response to the ongoing cost-of-living crisis and challenges relevant to long-term productivity and population ageing.

However, there is a stark contrast between the city-state and other major developed economies. Singapore has net zero debt, and, in some ways, has already solved the long-term fiscal issues facing other countries.

Singapore’s government gross debt level is worth 170 per cent of gross domestic product (GDP). But this is offset by high levels of domestic savings in both the public and private sectors. The city-state is a capital exporting country that generates reserves from its large financial assets and public investments.

A large portion of the public sector comprises large government-linked companies – such as SMRT Corporation and Singapore Airlines – and its sovereign wealth funds – including the Government Investment Corporation and Temasek Holdings.

GIC has around US$770 billion ($NZ1.2 trillion) in assets under management and Temasek has US$290b ($NZ470b). In combination this is around 227 per cent of Singapore’s GDP.

In contrast to libertarian claims that governments should simply reduce wasteful spending, Singapore’s approach to fiscal policy involves an effective and strategic government that leverages the state as an investment vehicle.

Former Singaporean finance minister Goh Keng Swee said it best: “Our experience confirms some of the conventional wisdom of growth theory, but refuses much of the rest. The role of government is pivotal.”

Simultaneously, in the private sector, the Central Provident Fund (CPF) plays a fundamental role providing social insurance to citizens, but in the form of self-provision rather than a ‘pay-as-you-go’ social security system, such as in the West.

Singaporeans are required to save up to 20 per cent of their wages, and an additional 17 per cent is provided by their employers, which is invested by the CPF Board. As of 2023, CPF managed around S$571b (NZ$707b) – equivalent to 92 per cent of Singapore’s GDP.

Overall, Singapore’s fiscal management has been outstanding, and its prudent fiscal management has allowed the country to thrive as the diamond of Southeast Asia. The city-state currently has a very high net worth position.

I came to study in Singapore to understand precisely why this was possible and what policy lessons the city-state could provide for New Zealand.

I was inspired by Lee Kuan Yew’s story. It was in 2019 when I first read his autobiography, ‘From Third World to First: The Singapore Story, 1965-2000′. It sparked my desire to study in Singapore and learn about its unique and unorthodox economic model and policies.

My time in the city-state has made me realise that we have much to learn from its fiscal policies – particularly around public asset management. In contrast, our economic history has a mixed record.

For NZ, we missed the golden economic opportunity when then-prime minister Sir Robert Muldoon cancelled our superannuation scheme in 1975. It was one of the worst economic decisions made by a government. If we didn’t, NZ would have much higher domestic savings potentially as high as NZ$500b.

Sir Michael Cullen’s decision to revive a private saving scheme under KiwiSaver in 2005 was a sensible decision, but it was insufficient. The total KiwiSaver funds currently under management is NZ$105b – equivalent to 25 per cent of NZ’s GDP. It is an automatic enrolment scheme with minimum and maximum contribution rates of 3 per cent and 10 per cent. This is much lower than Singapore’s compulsory rates for both employers and employees.

Cullen also introduced our sovereign wealth fund – the NZ Super Fund. It was an innovative policy developed in 2001 based on his long-term foresight and prescience that demographic ageing would result in a significant increase in pension demands. Our sovereign wealth fund currently has a balance of NZ$70b – 18 per cent of GDP. Draw downs will start soon in 2033.

Since the passing of the 1994 Fiscal Responsibility Act, there was strong bipartisan consensus of ensuring persistent budget surpluses. This institutional framework helped our nation to weather the storm of the 2007-08 Global Financial Crisis and the Covid-19 pandemic because of our low debt position of 19 per cent of GDP in 2019.

Yet, in stark contrast to Singapore, NZ has not been able to build greater public assets that could be utilised in favour of the long term. There is no doubt that our KiwiSaver plans are competent, but their investments have not been diversified, with a significant portion of funds being invested passively abroad. Regulatory hurdles have hindered the growth of the sector and greater competition.

Although the NZ Super Fund is highly regarded internationally, with annualised investment returns of around 10 per cent over the past 20 years, the fund’s size could have been larger if the previous National-led government had not stopped contributing to the fund to reduce budget deficits.

It is clear that based on the projections from the NZ Treasury, demographic change and population ageing will have substantial fiscal implications with net debt expected to reach above 160 per cent of GDP by 2060. In the words of late Harvard economist Martin Feldstein: “The current structure of pension systems in most developed countries cannot be sustained without cutting benefit levels substantially or introducing much higher taxes”.

Therefore, whilst maintaining fiscal discipline, pursuing the development of much greater public assets and ‘nudging’ individuals and households towards greater domestic savings is fundamental to NZ’s long term fiscal position.

Singapore’s unorthodox but pragmatic economic model provides some answers to our future challenges.

Nicola Willis should consider examining parts of Singapore’s macroeconomic strategy – it’s not just about balancing the books but identifying methods in building significant domestic capital savings and developing strategic government assets in the interests of the public.

Leonard Hong is a NZ Prime Minister’s Scholar for Asia, studying for a Master’s degree in International Political Economy at Nanyang Technological University, Singapore. He is also an Asia New Zealand Foundation Leadership Network member.