On November 23, 2023, Dr. Henry Kissinger passed away at his home in Connecticut peacefully at the age of 100 years. Being a curious student of international affairs, I’ve always found him an unusual character – someone who perhaps has a terrible reputation and yet simultaneously admired by elites and academics for decades. When I heard the news pop up on Bloomberg, I felt sad in contrast to other peers around me. Many called him a “war criminal” for his actions as Secretary of State and National Security Advisor under President Nixon. But paraphrasing from his biographer Niall Ferguson, I think that claim may be quite harsh because various American policymakers have made either worse or equally destructive decisions such as President Truman’s nuclear bombing of Hiroshima and Nagasaki. Yet, I do think he deserves scrutiny and history needs to be objective.

Personally, despite what others might say, I put myself relatively more in the “admirers” camp. It is not because I agreed with everything he did – I have strong disagreements with some of his foreign policy approaches and found his brash arrogance across his books occasionally annoying – but rather to do with his academic contributions. Yes, his unilateral involvement in Chile created prolonged issues with the installment of Dictator Augusto Pinochet. His actions in Vietnam prolonged the war which perhaps caused more American deaths and unnecessary suffering of the Vietnamese people. Kissinger and Nixon’s call to carpet bombing Cambodia likely contributed to the rise of the genocidal Khmer Rouge. His decision to support the Bush Administration’s 2003 War in Iraq alongside the neoconservatives was also indefensible. However, he also made a lot of world-leading decisions. Following the initial engagements he had with Mao Zedong in the 1970s, his realist approach to international relations changed the world, paving the way for Deng Xiaoping’s pragmatic leadership. Without Kissinger’s foreign policies, the world would not have witnessed the rapid rise of globalization and exponential improvements in the world economy.

He is also someone who never stopped learning and provided important scholarship in his subsequent years even before his passing. I was fortunate enough to read two of his books, “World Order” and “On China“. I’ve also read his authorized biography, “Kissinger: 1923-1968: The Idealist” by Niall Ferguson as well, which taught me a lot about what it takes to become a master in the field of international relations and how he leveraged his networks with elites. A very charming and charismatic diplomat who be-friended Nelson Rockefeller as a Harvard Professor. I did buy a copy of his last work published in 2022, “Leadership: Six Studies in World Strategy” which I hope to read sometime after I finish my postgraduate programme in Singapore. Nevertheless, throughout his overall scholarship, he always emphasized the importance of pragmatism and effectiveness, rather than ideological crusades in the image of “liberalism”. The notion of the balance of power, the 1648 Treaty of Westphalia, and the crucial importance of “legitimacy” were all common themes throughout his books. He has historically toyed with Immanuel Kant’s “Perpetual Peace” hypothesis and was in many ways a person with strong convictions on a morally just society based on his previous experience as a German Jewish refugee to the United States. His decision-making was made broadly on the strong sentiment that there is no such thing as solutions, but only trade-offs – the worst of two evils. Whilst this might sound cruel, he always kept this sense of tragedy in his mind and viewed human nature broadly in a negative light. Machiavellianism was one of the key ideas that I think he utilised to maximize his own position. A complex ideological thinker who was a true Realist, but context-driven with strong moral convictions about what he truly believed

Lee Kuan Yew and Dr Kissinger

His friendship with Lee Kuan Yew also shaped my view of Kissinger. He was a great friend of Singapore and someone who engaged regularly with Lee Kuan Yew throughout the 60s until his passing in 2015. Kissinger also wrote forewords for both Minister Mentor Lee’s autobiographies and Graham Allison’s interview series written based on his interviews with Minister Mentor Lee. They both share a common agenda – pragmaticism and obsession with excellence. This ideal is something that I share equally. Policy of course always has trade-offs but what matters is whether the better trade-off and decision were made. Lee Kuan Yew was also criticised heavily by many across the Western media for his crackdown on opposition in Singapore’s domestic politics. Coincidently, Kissinger himself faced stringent criticism against him as he finished his tenure in the White House. Both share this unique combination of being renowned for their contributions but also heavily criticized, but they are both remarkable and outstanding individuals. That’s why I respect them in many ways– but more importantly Dr Kissinger for his immense contributions to the world.

In conclusion, I think he is a complex character that he needs to be studied more extensively, rather than simply criticized for the sake of being criticized. Of course, his decisions need to be analyzed carefully but without the personal ad hominem attacks which I have found increasingly common in today’s period of growing political polarization. I think this statement from his son, David Kissinger, provides some insights into what we can learn. David said on his father’s 100th birthday:

How then to account for his enduring mental and physical vitality? He has an unquenchable curiosity that keeps him dynamically engaged with the world. His mind is a heat-seeking weapon that identifies and grapples with the existential challenges of the day. In the 1950s, the issue was the rise of nuclear weapons and their threat to humanity. About five years ago, as a promising young man of 95, my father became obsessed with the philosophical and practical implications of artificial intelligence.

David Kissinger

Something that we should live by as we also get older. Continue to remain curious about the world, improve our decision-making, minimise our mistakes and learn from the best, like Dr. Henry Kissinger. He is perhaps the most formidable policymaker of the 20th century.

I have an announcement to make in regards to my new adventure. I received the Prime Minister’s Scholarship for Asia to study a Master’s degree in International Political Economy at Nanyang Technological University Singapore at the RSIS | S. Rajaratnam School of International Studies starting in August this year. This is an exciting opportunity for me to pursue my passion in political science and economics at a world-leading institution ranked alongside John Hopkins and Columbia University.

I decided to study in Singapore because I was intrigued by Lee Kuan Yew’s leadership and the city-state’s economic miracle. As a result of its world-leading meritocratic approach to governance and Singapore’s emphasis on excellence within its society, the nation is now one of the most developed economies in South East Asia. In particular, I am eager to learn about Singapore’s sovereign wealth funds, its interconnections with state-entities like the Monetary Authority of Singapore, Temasek, GIC and the Central Provident Fund.

I would like to thank my academic and professional mentors, notably Professor Natasha Hamilton-Hart and Andrew Bayly MP; and also colleagues and friends who have contributed to my personal and professional development. Special thanks to Education New Zealand | Manapou ki te Ao for the financial support. I’m looking forward to this new adventure abroad that takes place soon.

A famous national populist, former US President Donald Trump

The economy is not an understandable and controllable machine as assumed by conventional macroeconomic theory. Rather, the economy is a complex, adaptive system, like many others in nature and society, in which policies can have significant, unintended consequences.

Former BIS Chief Economist William R. White

We are dealing with an intellectual problem—a profession that has been absorbed by theoretical constructs abstracting from human behaviour. We are dealing with ingrained ways of thinking. The challenge is to raise questions about accepted approaches, in drawing lessons from recent experience. We need to pull economics back into the real world of political economy.

Former Federal Reserve Chairman Paul Volcker

We also have to recognize that good economics cannot be divorced from good politics: this is perhaps a reason why the field of economics was known as political economy. The mistake economists made was to believe that once countries had developed a steel frame of institutions, political influences would be tempered.

Former IMF Chief Economist and University of Chicago Professor Raghuram Rajan

Leonard’s Curiosity in Economics

My interest in the political dimensions of economic policy began while I was still an undergraduate student at the University of Auckland. I was intrigued by the rise of Bernie Sanders in the United States and Donald Trump in 2015. They both represented movements against the status quo of government. Meanwhile, in my Economics courses, I was learning about macroeconomic models of endogenous growth, the Solow-Swan theory of technological progress, Paul Krugman’s liquidity trap theory, Milton Friedman’s monetarist theory, among other frameworks. An intense interest in both Political Science and Economics led me to major in both disciplines (History and International Business were later added in 2018).

Theoretical economic models were fascinating. Yet, in my mind economists have been missing the mark.

I was particularly intrigued by the global financial crisis (GFC) of 2007-2008. What caused it? The greed of Wall Street, easy monetary policy, or institutional corruption? Globalisation? Are there political influences at play? Exactly how can geniuses from Ivy League universities make such an error? I was perplexed by the global financial crisis and remained keenly interested in it (so much so that I even co-authored a report on the potentials for the next financial crisis in 2021).

The failure of world-renowned economists – in the likes of Larry Summers – to identify the fundamental causes of the GFC (and the aggregated political effects of that crisis) convinced me that the discipline required fundamental reform.

My education at the University of Auckland contributed to my intellectual framework. However, the models and theories that I learned in my economics classes were insufficient to prepare me to be an excellent economist. I believe that the study of Political Science, Psychology and Economic History should become complementary areas for students studying Economics.

As someone who also holds a degree in History, the economic topics within all of the courses I took always intrigued me. Among these themes are, for example, the role of hyperinflation in the fall of the Weimar Republic and the rise of Hitler; the rise of Keynesian economics and the New Deal; the rise of the Bretton Woods system and its effects on international affairs; the revival of Communist China under Deng Xiaoping; and the experience of New Zealand under Rogernomics and Ruthanasia. In contrast to my colleagues who were studying other topics, I was fascinated by economic problems and how they affected the political system in general. As I see it, Economics is a hybrid of the humanities and the sciences – a social science. I was told by my history lecturer, Dr Paul Taillon, that I had more of a ‘political economy’ bent. I fully concurred with his assessment.

My involvement in Economics as a discipline was motivated by this experience. An overview of my obsession with the subject is presented in this section. It is fascinating to me and I intend to continue my studies in the future. In the next section, I will explain the fundamental causes of the GFC and why many economists got their predictions completely wrong.

The Failures of Economists: Predicting GFC

Many economists, including Nobel laureate Paul Krugman, admitted they were wrong in the wake of the first major economic catastrophe since the Great Depression. Most mainstream economists failed to predict the onset of the financial crisis in 2007-2008 (with notable exceptions such as William R. White, Niall Ferguson, Raghuram Rajan and Kenneth Rogoff). There was a great deal of hubris and arrogance in the profession.

By the beginning of the 1960s, mathematicians and engineers were becoming increasingly involved in the economics discipline, leading to the development of econometric models as a dominant source of policy analysis. One of the main reasons this occurred is the rise of mathematical economics. Paul Samuelson and other ‘technical’ economists popularised this sub-discipline. Prior to this disciplinary revolution, the subject was called ‘political economy’, not economics as we all understand it today. Through mathematic economic modelling, increasingly more experts have become almost certain that modelling meant that it will be reflected in the real world. In many ways because of what the numbers told them, many determined that the risk of financial collapse has been eliminated. Financial markets are supposedly safer as a result of the ‘Great Moderation’ and technocratic management of the economy. Francis Fukuyama’s End of History did not help. It created further arrogance and complacency among western elites, believing that they were destined to spread free markets and liberal democracy globally. However, with the bursting of the housing bubble in 2007, the Great Moderation of 1987-2006 proved to be a myth as it led to the collapse of the global economy.

The GFC taught me that economics was not an entirely objective or empirical discipline in the same vein as mathematics, chemistry, and physics. In the words of former Bank of England Governor Mervyn King, “Economists have brought the problem upon themselves by pretending they can forecast. No one can predict the unknowable future and economists are now exception”. Economists forgot a very important concept called ‘radical uncertainty’.

In terms of quantitative predictions, in many ways they are correct in the modelling. But it is correct in real life? No. The models are not perfect. Individuals are not fully rational. Statistical formulas and mathematical equations can get manipulated to provide the authors of a particular research paper with data that supports their hypothesis.

I do not claim, however, that empiricism does not matter – it does matter to a considerable degree. Using models, we can obtain an understanding of what is happening throughout our economic system. We would struggle to solve problems without the aid of hypotheses testing and quantitative methods. But it does become problematic when economists strictly rely on models, as fundamentalist beliefs, akin to the scientific fact of gravity.

Pricing for options is an example of this. The Nobel Prize in economics was awarded to Robert Merton of Harvard University and Myron Scholes of Stanford University for their contribution to calculating stock options (a form of derivatives). In the financial world, it was believed that ‘rational’ calculations of these risky investments were feasible. But this was utter nonsense. It is nearly impossible to determine the value of these complex financial instruments. Analysts have devised numbers to create an impression of credibility. It was just a bogus form of quantification. There was a quasi-religious belief among people in the financial sector that risk had virtually disappeared following the introduction of these objective models. This legitimized financial gambling. This intellectual debacle was caused by the dogmatism of belief in ‘market perfection’ and ’empiricism’. Economist Raghuram Rajan questioned this dogma of the financialisation of the world economy in his 2005 research paper. He showed that actually banks and financial institutions were making more money via more risk, not less risk as shown by these models for derivatives. As shown in the documentary ‘Inside Job’ by Charles Ferguson, to some degree it was a form of intellectual and moral corruption where economists across elite institutions brought the idea that risk was eliminated.

The failure of economists told me a few things. There needs to be a fundamental restructure in the education of future economists. Economics as a discipline needs to combine both the ‘economic history’ and empirical methods to explain and understand complex systems like the global economy. More emphasis needs to be placed on the ‘humanity’ aspect of economics. The classical scholars in the likes of Adam Smith, David Ricardo, David Hume, John Maynard Keynes and even Hayek were not entirely mathematically driven economists. All of them were experts in the political economy. Excess objectivity within the field of economics led to financial disasters and hubris.

The GFC should have been a wake up call, but have there been some changes? Not necessarily. Economists still buy into their DSGE models and macroeconomic equilibrium hypotheses. Although some economists in the likes of Dani Rodrik, Raghuram Rajan and Joseph Stiglitz have been warning others for some time about the continued failure of their fellow colleagues to diagnose the problem. What we witnessed instead were significantly political consequences in the form of both left wing and right wing populism.

Backlash against the Technocrats – Western Populists

While the mainstream neoclassical economists continued to repeat their talking points to the world, the world was shifting to a more polarised society. The GFC did not help the cause. With millions of ordinary people losing their life savings and wealth. Simultaneously, big banks and financial institutions were bailed out without any jail time for many of the financial executives that created the problem. Injustice and economic corruption led to a growing mistrust towards public institutions.

Politically, people became very angry across the world and manifested to resentment.

As shown by Charles Murray’s ‘Coming Apart‘, much of the political discontent had to do with offshoring of manufacturing and the decline of communities in former manufacturing hubs such as Detroit. These states and regions are nicknamed Rustbelt states for a reason. These same white-working class folks lost their jobs and their livelihoods through free trade agreements and offshoring of their jobs into developing countries. The rise of opioid addiction, rising divorce rates, crime, social disintegration, declining social mobility, and educational regression led to an intergenerational downward cycle. J.D. Vance’s ‘Hillbilly Elegy’ does a wonderful job illustrating the extent of the social decay. The richer urban class in states such as California and New York saw their wages increase exponentially with more households and families in these areas getting more educated, while those in the former stronghold manufacturing states such as Michigan, Wisconsin and Pennsylvania failed to see rising incomes. As mentioned by Raghuram Rajan, the premium on College education and demand for skilled work led to growing economic inequality. Social decay and free market prescriptions were a recipe for social disintegration and political discontent.

Globalisation and international economic integration was the correct policy subscription, but the short turn effects were devastating. Although globalisation and free flow of capital and labour led to overall net-positives for the world economy (3.8 billion people in the middle class as of 2018). Economists and policymakers failed to consider these people’s livelihoods. Trade adjustment subsidies and social insurance were insufficient.

Consequently, across the western world, we saw more politicians going against these mainstream orthodoxies. Anti-European Union politicians in the likes of Nigel Farage and Boris Johnson became increasingly popular, meanwhile the US saw the rise of an anti-liberal demagogue in the form of Donald Trump. Simultaneously, left-wing populists such as Bernie Sanders and Jeremy Corbyn shocked the world with their relatively successful campaigns for President and Prime Minister (and UK Labour’s leadership).

In my eyes, a healthy dose of populism is important for liberal democracies. It provides people with the sense that something is fundamentally wrong in society and that policy adjustments were warranted. But, extreme and excess populism can lead to bad consequences as we’ve seen with the rise of Hitler and Soviet Communism post-Great Depression. Economic stability and growth is significant for a stable liberal democratic system. Systems can break down and cause revolutions if it gets out of hand. This is why understanding the root causes of contemporary populism and dealing with the problems raised is crucial. However, I’m yet to see any western politician hoping to resolve the anti-establishment populist sentiment. Nor are economists willing to provide a new approach to this ongoing political economy problem.

Conclusion

“Almost every political question has an economic aspect and almost every economic question has a political aspect”.

Charles P. Kindleberger

As the prominent international political economy scholar Charles Kindleberger states in this quote, economics cannot be separated from politics and vice versa. The rise of mathematical economics and econometrics are crucial to policy evaluation and analyses, but by ignoring economic and political history, we fail to learn our lessons from what really happened. Economics is not just about models – it’s about people’s livelihoods. Humans are not just rational utility maximising robots. We are complex and we cannot rely simply on microeconomic theory, presumptions and calculations as a basis for effective economic policy making.

This opinion piece was to inform readers about understanding and staying skeptical about the economics profession. I have been heavily involved in this field and public policy in the early stages of my career and even though I don’t know much in comparison to many professionals globally, I hope this piece was relatively informative. As Kenneth Rogoff mentioned before, economics should still stay relatively objective and mathematical, but we must not ignore economic history and incorporate other aspects of social science into the equation.

I am a political economy person, and I think more economists should move in this direction.

US President Herbert Hoover once stated, “Blessed are the young, for they shall inherit the national debt.”

Right now, young people have a reason to be concerned. Since Covid-19 arrived 18 months ago, New Zealand’s net public debt has nearly doubled. Government net debt rose from 19% of GDP – Gross Domestic Product – in 2019 to 34% this year.

This is the highest ratio since 1996.

The bulk of debt increase was from the wage subsidies – around $18 billion. Other business support programmes were supplementary. These fiscal responses were intended to enable faster economic recovery.

New Zealanders were seared by the 1984 debt crisis. That experience produced a broad bipartisan consensus in favour of fiscal responsibility rules. Budget surpluses were achieved by the mid-1990s and sustained, albeit with reducing spending discipline, to 2008.

Those surpluses helped New Zealand weather the storms of the 2007-08 GFC and the Christchurch earthquake. But it took seven years of fiscal slog and expenditure restraint to restore fiscal surpluses after the GFC.

Big spending increases from 2017 preceded Covid-19 and now the challenge of turning ongoing fiscal deficits into surpluses has arisen anew.

Are current arrangements up to the task? Not in our opinion. In 2014, the New Zealand Initiative proposed a Parliamentary fiscal council to help Parliament better scrutinise government spending and fiscal prudence.

This was not out of the blue. In 2011, the OECD found that “independent fiscal institutions can buttress a government’s capacity to comply with a numerical rule.” These institutions exist in 28 of the 38 countries in the OECD.

In 2017, the-then opposition parties – Labour and the Greens – endorsed a Fiscal Council of an unclear design. The advent of Covid has stilled work on this, and there are no indications that fiscal discipline and constraint will be the heart of the Government’s priorities.

A global pandemic understandably opens the fiscal taps, but that only heightens the need for a subsequent return to fiscal discipline and accountability. That determination is not yet evident.

To fail to restore discipline in spending quality and current financing is to do future generations a disservice. It is fine for the young to inherit debt backed by assets of equivalent value, but not otherwise. Herbert Hoover’s remark is best seen as a humorous aside that would be irresponsible if put into practice.

This is a good review by Michael Reddell on my co-authored report. As he pointed out, we agree with the Goodhart/Pradhan hypothesis on the demographic implications on the global financial system.

At 11am the New Zealand Initiative released their latest report, by Bryce Wilkinson and Leonard Hong, under the title “Walking the Path to the Next Financial Crisis”. It comes complete with a Foreword from former Reserve Bank chief economist (and former Board chair) Arthur Grimes, under the title “A short walk?”, foretelling doom and repeating his recent attacks on the Reserve Bank’s conduct of monetary policy over the last 20 months, ending with the ominous – and printed in bold – declaration “This time is not different”.

The Initiative was kind enough to send me an embargoed copy yesterday. Perhaps the first thing that rather surprised me – in a document that is really quite critical of both monetary and fiscal policy and aspects of the way the Bank does other things – is that the acknowledgements include thanks to a Reserve Bank MPC member (Bob Buckle) for “valuable feedback…

Content creators are the fastest growing type of small business worldwide. Today, over 50 million people consider themselves ‘influencers’ on social media.

According to YPulse – a youth research organisation in the United States – over 72% of Generation Z wants to become online celebrities.

Nowadays, getting famous on Instagram or TikTok is the ticket to wealth and fame. According to a Harris poll, more kids dream of becoming a YouTuber than an astronaut.

Generation Z kids do not want traditional careers in engineering, medicine, consulting, and teaching. Becoming viral on TikTok through outrageous flamboyance can make you a millionaire. “Don’t need no education, don’t need no thought control”.

Intellectuals, social conservatives and cultural pessimists commonly decry this trend of ‘superficial consumerism’. “Yet another dissolute younger generation in the making”, they sniff.

Yet, pop culture meets a need. No one is forcing the youthful masses to follow ‘influencers’. Following them takes time, and buying the products they endorse swallows money.

This is not new. Teenagers have been buying ‘brands’ for decades. They having been indulging and experimenting in all sorts of things that affront their elders, probably from time immemorial.

So the followers of the influencers must be getting a benefit. In part, it will be a social group thing. I get that.

Moreover, ‘influencing’ must be a competitive and risky business. Entry is free. Anyone can be outrageous and flambuoyant – until the euphoria fades. One tweak that misses its mark could destroy months or years of assiduous cultivating of one’s followers.

Take Daniel LaBelle for example. He started a physical comedy channel on TikTok last year, and now has over 23 million followers. Podcaster Joe Rogan has to entertain 200 million people monthly on Spotify.

Imagine waking up every morning wondering what you can do next to titivate such followers, without blowing everything. Who wants that pressure?

Many influencers will crash and burn, just as pop musicians have for decades.

But pop music endures because it entertains. So far influencers are passing that test.

The world’s major economies are walking into the next global financial crisis. Moreover, their authorities do not seem willing to change direction. They fear that raising interest rates or cutting government budget deficits risks precipitating the collapse they seek to avoid.

Those are the major conclusions of our report we released last Thursday.

In response to the Global Financial Crisis over a decade ago – and then again to Covid-19 – worldwide, major central banks have eased monetary policy settings to an extraordinary and potentially destabilising degree.

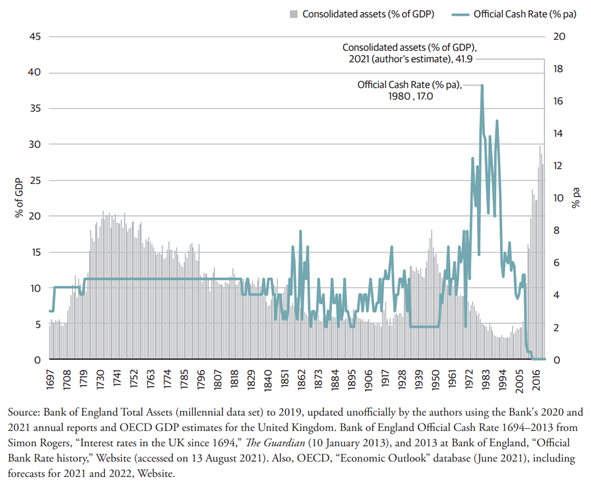

The Bank of England is the world’s oldest central bank. Never since 1697 has its control interest rate been as low as it is today (0.1% pa). Never has its balance sheet relative to gross domestic product (GDP) been as bloated from creating money as it is today. (See the following figure)

The US Federal Reserve, the European Central Bank, and the Bank of Japan have progressively also adopted historically extreme levels for monetary policy settings.

Simultaneously, many governments have pushed their public debt ratios up to an extraordinary degree. Federal public debt held by the public was a historic high relative to GDP at the end of World War II. Congress’s Office of Management and Budget now forecasts that this high will be exceeded in 2024 – a war-time like debt in peace time. This is unprecedented, and it is because of large ongoing budget deficits. The US Federal government’s projected fiscal deficit for 2021 is an astonishing 16.7% of GDP.

In September, US Treasury Secretary Janet Yellen warned the US was heading for sovereign default if the government’s debt ceiling was not lifted. Eventually, Congress agreed to increase the limit, but this merely kicks the debt can down the road – again.

In Europe, a condition set in 1992 for monetary union was that member countries’ gross public debt ratios should not exceed 60% of GDP. According to the latest official forecasts, only 7 of 22 countries will comply in 2021. All the largest economies now exceed 60%. The debt ratios for the seven worst cases exceed 100% – for Italy it is a crippling 166%.

Italy’s high debt ratio is a serious risk to the stability of the Euro currency block. This is because its economy looks to be too large for the rest of Europe to bail out.

Lower interest rates invite governments to borrow more. The utter perversity of the current situation is epitomised by the fact that the Eurozone’s overall government net financial indebtedness has never been higher and the net interest cost lower relative to GDP.

China is also a potential source of instability. Serious debt problems have emerged in its housing market – which accounts for 29% of its economy. This makes it of potential global significance. The debt crisis at Evergrande – the second largest property developer illustrates the concern.

Globally, persistently low interest rates encourage firms and households to borrow excessively to buy assets that would otherwise be over-priced. That contains the seeds for that next crash.

Low interest rates also prolong the existence of “zombie” companies that should be wound up. Healthy companies could use their resources more productively.

High public debt ratios not backed by assets of comparable value give governments a conflict of interest. As economic managers, government should be leaning against excessive borrowing rather than fuelling it by low interest rates and quantitative easing.

Being heavily indebted compromises government’s willingness to act.

This problem of excessive borrowing and over-priced assets has been made worse by the signal the major central banks have been sending to investors – that the authorities will ‘do whatever it takes’to prevent any major collapse.

Professor Arthur Grimes, former chair of the Reserve Bank’s board, wrote the foreword to the report. He succinctly identified that perverse incentive problem:

“Governments, central banks and private sector financial institutions have together created the seeds of the next crisis on the assumption that policy actions will protect borrowers and lenders from downside risks. The result has been a one-way bet for those positioned for asset price rises, while those who have acted prudently have been left behind.”

The perversity of the current situation is further illustrated by the US. In 2020, it recorded the greatest decline in economic activity (real GDP) in at least 60 years. Its unemployment rate more than doubled.

Yet US household wealth rose by a record amount (26%). In dollar terms, it rose by much more than if households had saved 100 percent of national income in 2020.

So, how could US households overall become far more prosperous amidst the biggest downturn in over 60 years? The answer is capital gains and more money in the bank because of the Federal Reserve’s credit creation and low interest rates. US sharemarkets have boomed along with property prices.

The Initiative’s report traces the path to the current government ‘debt trap’ situation, first under the gold standard and subsequently with fiat money.

There is an optimistic scenario. It requires continuing near zero interest rates; low inflation, strong growth that lifts tax revenues; and firm resolve to reduce government budget deficits.

One can hope, but each step in this scenario looks implausible. Consumer price inflation has emerged this year that can only put upwards pressure on interest rates; pressure that central banks have been resisting.

In the past, periods of excessive debt and money creation have tended to end badly. Our report considers two much less rosy, low growth, high unemployment scenarios and one disastrous one of ‘Great Depression’ dimensions.

We leave it for readers to decide what probabilities to put on these and other possible scenarios. Nor does the report speculate about the timing of the next global crisis.

New Zealanders can only take precautionary measures. Being a small and globally integrated economy, New Zealand cannot prevent the next financial crisis.

Reducing debt to prudent levels is important both for governments and households. A fiscal council could help Parliament to hold government to account for the quality of its spending.

Firms and households should avoid borrowing to excess to buy over-priced assets. A narrower and more prudent focus for the Reserve Bank is desirable.

The temptation in the face of such extremes in the major economies is to hope that somehow this global episode will not end in tears – that “this time really is different”. That is mere wishful thinking.

Dr Bryce Wilkinson and Leonard Hong of The New Zealand Initiative co-wrote Walking the Path to the Next Global Financial Crisis.

Both the global financial crisis (GFC) of 2007-2008 and the Covid-19 pandemic caused disruptions to the world economy.

During the GFC, stock markets plummeted, and millions of people became unemployed. Business and bank failures resulted in financial pain.

Covid-19 did not cause as much economic destruction as experts predicted. So far, at least.

During this recession, bankruptcies declined during the pandemic, while prices of assets such as cryptocurrencies, stocks, and houses reached record levels. The net worth of US households increased by USD$26 trillion in 2020.

These developments are extraordinary and unusual. Usually, recessions mean severe losses rather than wealth gains. Are our current financial circumstances sustainable?

Our new report Walking the path to the next global financial crisis explains how skyrocketing public debt and monetary policy easing threaten global financial stability.

In the wake of the GFC, government bailouts of financial institutions ratcheted up public debt ratios dramatically. That was not reversed before Covid struck.

Governments and central banks in developed economies now face tough choices regarding interest rates and debt.

Raising interest rates or ending quantitative easing could destabilise asset markets and the economy. Governments, meanwhile, struggle to wind down stimulus spending and fear higher interest payments on debt.

By printing money and maintaining low-interest rates, it also fuels consumer price inflation. In New Zealand, consumer price inflation hit 4.9% – the highest level in over a decade. Inflation in the US and the EU is also approaching 6%.

The authorities are not showing a determination to return settings to more normal levels before the next economic shock occurs. They have led investors to believe that the government will underwrite high asset prices such as cryptocurrencies, stocks and housing.

It is now common to hear terms like “too big to fail” and “whatever it takes” in financial market jargon. Such beliefs are dangerous for financial stability.

For the government, it is prudent to repair the roof while the sun is still shining. Financial support packages were necessary during Covid-19. But the government should have a credible plan for reducing net debt to more sustainable levels once the pandemic is over.

The financial well-being of citizens is at greater risk when governments are less financially prudent.

As a small, globally integrated economy, New Zealand cannot prevent the next financial crisis.

We do not know when the next financial crisis will hit. But we can prepare for it when it does.

이 보고서의 제목인 “글로벌 금융위기로 가는 길(Walking the Path to the Next Global Financial Crisis)”은 얼마나 가까운 미래에 금융위기가 발생할 것인지에 논란에 대한 질문을 던진다. 그리고 상당히 근미래에 글로벌 금융위기가 발생할 수 있는 이유가 있다고 본다.

지난 25년간 뉴질랜드를 비롯한 많은 국가들은 아시아금융위기와 글로벌금융위기(GFC)라는 두 번의 전세계적인 위기의 영향을 받아 왔다. 이 두번의 금융위기는 부채 문제를 심각하게 받아들이지 않고 지속가능하지 않은 방법으로 무리한 확장을 해왔던 것이 그 원인이라고 할 수 있는데, 정부의 재정적자, 중앙은행의 안일한 통화정책, 그리고 민간금융기관의 무분별한 대출관행이 맞물려 이러한 위기를 초래했다.

코로나19팬데믹으로 인한 위기 상황에 대해 금융기관이 취한 결정들은 앞서 발생한 두 금융위기를 초래한 문제들을 답습하고 있다. 각국 정부는 활발한 경제 활동과 경기부양을 위해 위해 돈 쏟아붓기를 감행하여 부채 후유증 가능성을 높이고 있고, 중앙은행 이러한 적자 보전을 위해 자금을 마련해주었으며, 민간기관은 그로 인한 유동성이 막대한 투기적 자산 구매를 위한 대출로 이어지게 방관하고 있다.

금융시장 버블에 대해 금융정책기관들이 근시안적인 행동을 취하고 있는 것 역시 과거를 답습하고 있다. 예를 들면, 미국연방준비은행(Federal Reserve)은 1998년 장외파생상품(LTCM: Long Term Capital Management) 시장의 붕괴 이후 금융기관을 구제해 주는 결정을 내린 바있다. 그러한 개입직후, 미국회계감사원(GAO)는 그 같은 구제에 대하여 다음과 같이 평가했다.

… 연방준비은행이 대형금융기관을 대신하여 개입 할 것이라는 믿음을 줌으로서, 그 기관들이 더 많은 리스크를 감수하도록 장려한 셈이 되었다 … 연방준비은행의 개입으로 인해 사람들은 “대마불사(too big to fail)”의 신조가 확대 되었다고 우려했다 … 연방정부의 안전망이 확보되었다고 기업들이 믿게 된다면 이들이 더 리스크가 큰 사업을 추구하는 행태를 조장하게 된다.

무분별한 확장에 대한 이러한 예측은 글로벌 금융위기 이전에 이미 쓰여진 것이다. 정부, 중앙은행 및 민간부문 금융기관의 정책 방안은 대출기관과 채무자의 손해 리스크를 줄이도록 개입하는 것에 초점을 맞추어 왔는데, 이것은 자산가격 상승에 올인하는 사람들을 유리한 입장에, 반대로 보다 신중하게 접근하는 사람들은 불리한 입장에 놓이게 하는 것이다.

1984년 경제개혁 이전 뉴질랜드에서도 유사한 방향의 움직임들이 있었다. 그리고 1994년부터 2008년까지 중도좌파와 중도우파 정부들은 후속조치로 15년 연속 재정흑자를 실현한 바 있다. 그리고 뉴질랜드 중앙은행은 물가안정 또는 최소한의 낮은 인플레이션을 목표로 삼았기 때문에 정부가 막대한 재정 적자를 초래한 타국가들과는 다르게 아시아금융위기와 글로벌 금융위기를 상대적으로 잘 해결할 수 있는 위치에 있었다.

뉴질랜드정부는 글로벌 금융 위기와 코로나위기에 대한 대응으로 확장 재정정책을 실행하였고 이러한 조치는 불가피한 측면이 있었다. 글로벌금융위기 이후, 재정정책은 신중한 자세를 견지 하였으며, 또 마땅히 그렇게 했어야 했다. 다만, 앞선 두 위기와 현재의 코로나-19 대응은 중요한 차이점이 있는데, 바로 코로나 대응을 위한 중앙은행의 조치는 유동성 및 자산가격의 큰 상승을 초래했다는 점이다. 이러한 조치는 뉴질랜드를 자산가격의 붕괴 위험에 노출시키는 것이고 이것은 향후 경제적 고통을 야기할 수 있다. 지속이 불가능한 재정정책과 및 통화정책으로 인하여 금융위기 리스크에 적신호가 켜졌다.

지난 40년 동안 공공정책에 대한 경제학자들의 가르침은 “이번에도 다르지 않다(this time is not different)”는 이 보고서의 통찰력있는 메시지와도 일맥상통하다.

보고서요약

이 보고서는 글로벌 금융시스템의 안정성에 대해 경고하고, 이에 대한 근거를 제시한다. 특히 미국, 유럽연합, 영국, 일본 등의 세계 주요국가들의 최근 행보는 또 한번의 글로벌 금융위기를 초래할 수 있다. 중국의 불투명한 부채 문제에 대해서도 우려가 크다.

각 국의 주요 중앙은행들은 전례 없는 수준으로 금리를 인하하고 자산을 매입하는 양적 완화를 단행하고 있다. 1694년 이후 영국중앙은행(Bank of England: BOE)의 재할인금리가 지금처럼 낮았던 적이 없다. GDP대비 자산가치도 전례없이 높다.

대규모 정부재정적자와 극심한 국가부채가 일상화되고 있다. 재정적자와 국가부채 문제는 금리가 예년 수준으로 올라갈 경우에 훨씬 더 심각해질 것이다.

역사적으로 보면 국가부채비율은 전쟁을 치룬다든지 하는 특별한 필요에 의해서 높아졌지만, 평화 시에는 천천히 감소하는 경향을 보여왔다. 그러나 평화 시기라고 할 수 있는 지금 현재, 국가부채비율은 충격적인 수준이다.

주요 선진국에서 국가부채는 공공부문의 자산 가치를 넘어서고 있다. 이들 정부들은 납세자인 국민들의 미래를 저당잡고 있는 것이나 마찬가지이다.

현재 각국의 금융당국의 대응을 보면 2007년 글로벌금융위기(GFC) 당시의 이례적인 수준의 대응보다도 더 극단적이다. 중앙은행은 금리를 대폭 인하하고 아주 이례적인 수준으로 대출을 확대하고 있다. 다시 말해, 정부가 그들의 금융기관들에게 긴급구제금융(bail out)을 제공하고 있는 셈이다.

이러한 조치는 일견 이해가능한 면도 있으나, 미래의 큰 리스크를 야기한다. 정책결정자들은 시장원칙을 무시하고, 여론을 악화시키고, 국가부채비율 증가를 부채질하고 있다. 당국에서 이러한 비용을 고려하지 않은 것은 아니다. 다만, 그들의 절실한 과제는 고용과 경제활동의 유지였다.

Covid-19 팬데믹 이전에도 세계 주요국들은 글로벌금융위기 이전 수준으로 금융정책이 정상화되지 못한 상태였다. (예외적으로 뉴질랜드는 대부분 글로벌금융위기 이전 수준으로 정상화되었다고는 하지만, 뉴질랜드를 세계 주요국이라고 하기 어렵다). 코로나 팬데믹으로 인해 국가부채비율과 순 금융 부채(net financial liabilities)는 전례없는 수준으로 증가하였다. 이것은 톱니바퀴 효과처럼 한쪽 방향으로만 움직이게 되기 때문에 우리를 미래의 글로벌금융위기로 이끌 가능성이 크다.

인위적으로 낮춘 금리는 역효과를 낳게 된다. 인위적으로 낮은 금리는 사람들로 하여금 과대평가되고 리스크가 큰 자산을 매입하기 위해 대출을 받도록 부추긴다. 그러한 결정은 암울한 결말을 맞이하게 될 가능성이 크다. 이러한 조치들은 또한 “좀비 기업(zombie firm)”이라고 불리는 기업들, 즉 미래는 없고 부채만 많은 기업도 근근히 생명을 연장하게 할 것이다. 이 좀비 기업들은 다른 기업들이 더 잘 활용할 수 있는 자원을 점유하고 있다. 그들은 또한 정부로 하여금 더 많이 빌리고, 덜 신중하게 지출하도록 조장한다. 이것은 다 미래에 큰 비용을 치루게 된다.

이러한 최근의 현상들은 다음과 같은 질문을 낳는다. 글로벌 금융시스템이 어떻게 하다가 이 지경까지 오게 되었는가? 앞으로는 어떻게 될 것인가? 뉴질랜드 정부와 국민들은 어떻게 책임 있는 행동을 할 것인가?

첫 번째 질문에 대한 간단명료한 대답은 우리의 시스템이 정부, 금융기관 및 투자자를 금융 리스크로부터 과도하게 보호했기 때문이라는 것이다. 정부를 포함해 모든 이들은, 납세자인 국민들이 리스크에 대해 계약심사(underwriting)를 하고 있다고 여길 때 덜 주의하게 된다. 이러한 행태는 소위 도덕적 해이(moral hazard)라고 불리기도 한다.

이 문제의 원인은 애초에 설계가 잘못되었다기 보다는 상황변화로 인한 것이라고 볼 수 있다. 평화 시기의 인플레이션은 고전적 금본위제를 고수하는 국가들에서는 미미한 수준이었다. 불황 속 물가상승 현상인 스태그플레이션(stagflation)은 1971년 미국이 금본위제를 폐지한 후 발생했다. 그리고 인플레이션을 줄여야 하는 고통스러운 디스인플레이션 과정이 뒤따랐다.

1990년대에 각국정부들은 0-2% 대의 낮은 인플레이션을 목표로 하는 통화정책에 집중했고 이러한 시도들은 꽤 성공적이었다. 이 시기에는 낮은 인플레이션과 함께 완만한 경제성장이 이어졌다.

그러나 1990년대에 글로벌 금융위기의 씨앗이 뿌려지고 있었다. 정부정책은 지나치게 리스크가 큰 부동산담보대출을 조장했다. 투자자들은 자산가격이 폭락할 경우에는 미국연방준비은행이 금융기관을 지원하기 위해 기꺼이 나선다는 것을 목격했다.

‘대마불사(too big to fail)’ 및 ‘그린스펀 풋(Greenspan Put)’과 같은 용어들은 금융업계의 일반적인 문법이 되었다. 거대한 미국정부 후원기관은 모기지 관련 보안위험을 감수했다. 신용평가기관들은 리스크를 제대로 파악하는데 실패했다. 심지어는 유럽중앙은행(European Central Bank)조차도 금융시장의 추락을 피하기 위해 모든 것을 감수하겠다고 약속하였다.

반면, 일본은 다른 경로로 글로벌 금융위기를 겪었다. 일본은 1970년대 스태그플레이션을 경험하지 않은 국가이다. 다만, 일본은 급격한 부동산가격 상승을 1980년대에 겪었으며, 1990초반에는 일본 경제침체와 함께 부동산가격이 폭락하게 되었다.

일본정부는 재정적자를 감수하고서도 경제활동을 활성화하기 위해 금융정책을 폈다. 일본중앙은행(Bank of Japan)은 점점 더 극단적인 통화정책을 실시했다. 경제성장은 여전히 취약했다.

일본은 글로벌금융위기 이후에도 이와 같은 정책경로를 고수해왔으며 다른 많은 선진국들도 동일한 조치를 많이 실시했다. 자산가치가 뒷받침되지 않는 국가부채의 급증은 일상화되었다.

앞서 말한 세가지 질문 중 두 번째 질문과 관련하여서는, 앞으로 자산가격, 인플레이션, 생산량 및 실업과 관련하여 굉장히 안좋은 일들이 펼쳐질 것으로 예상한다.

정부와 중앙은행의 극단적인 조치들을 어떻게 정상화할 수 있을 것인지 대책이 없다. 일본이 먼저 이런 상황에 빠졌고 스스로 빠져나올 수 없음을 보여주었다.

정부는 재정적자를 줄일 경우 실업이 증가할 것을 걱정한다. 중앙은행들도 금리 인상을 할 경우 실업에 미칠 영향을 우려한다. 소위 “좀비 기업” 들은 분명히 도산할 것이다. 금리가 높아지면 재정적자도 증가하는데, 이는 국가부도로 이어질 우려가 있다.

통화정책은 재정정책과 점점 더 밀접하게 연결되고 있다. 이러한 통화정책의 정치화(politicisation)는 금융시장의 안정성을 크게 위협한다. 다급해진 정부는 중앙은행이 낮은 이자율로 그들의 재정적자 문제를 해결하기 원한다. 유럽 중앙은행의 국채매입은 상당한 기간 동안 이탈리아와 일부 다른 국가의 정부재정적자 수준을 초과했다. 이러한 행보는 법적으로, 도덕적으로, 경제적으로 지속 가능하지 않다.

또 한번의 글로벌 금융위기가 시작되면 자산가격이 폭락하고 금융공황상태가 야기될 것이다. 실업과 대규모파산 사태가 이어질 것이다. 극단적인 인플레이션에 이어 디플레이션 상황이 오게되면 은행예금과 현금의 가치가 파괴될 수 있다. 많은 사람들이 부의 상당부분을 잃게 될 것이다.

미래에 글로벌 금융위기가 발생하면 모든 사람들은 정부에게 파산만을 막아주도록 경기부양(keep the economy afloat)을 하도록 기대할 것이다. 정부는 정치적으로 어렵지만 꼭 필요할 결단을 하기 어려워진다. 아쉽게도 정부가 그렇게 할 수 있는 역량도 줄어들고 있다.

그렇게 되면, 유권자들은 불행한 정권을 퇴진시킬 것이다. 유권자들은 포퓰리스트 또는 독재주의 정부로 기존의 정권을 대체할 수도 있다. 실망과 불안이 따를 것이다. 예측불가능한 미래가 펼쳐질 것이다.

이것은 선진국 경제의 최악의 시나리오이다.

이보다 더 낙관적인 시나리오가 있을 수 있다. 이자율과 인플레이션이 낮게 유지되는 동안 강력하고 지속적인 경제성장이 필요하다. 또한 정부는 지출을 늘리기보다는 재정적자를 줄이기 위한 세입 증가노력을 기울여야 한다. 안타깝게도 이 시나리오는 모든 면에서 문제가 있다. 그로 인해 낙관적인 시나리오는 단순히 희망사항(wishful thinking)일 수 있다.

이 보고서는 두 가지 다른 시나리오를 고려하고 있다. 하나는 선진국 경제는 일반적으로 절뚝거리게 될 것이라는 시나리오로, 1990년대 초반 이후 일본과 같은 상황이라고 보면 된다. 경제침체가 계속되고 순공공부채비율은 GDP의 200%를 넘게 된다. 인플레이션은 최소한으로, 이자율도 낮은 수준을 유지한다.

인플레이션이 문제가 된다면 금리를 올려 채무자에게 부담을 줄 수 있다. 글로벌 금융위기를 어떻게든 피하게 되더라도 1970년대의 스태그플레이션 사태와 비슷한 시나리오가 전개될 수 있다.

뉴질랜드가 글로벌 금융폭풍으로부터 스스로를 가장 잘 보호 할 수 있는 방법은 무엇인가? 뉴질랜드 국민들은 이상적인 상황을 원할 수 있겠지만, 그런 낙관론에만 의존해서는 안된다. 앞서 설명한 세계적인 흐름는 전례가 없었다.

소국 경제(small economies)의 경우 신중한 방어조치가 거의 유일한 대안이다. 뉴질랜드정부는 다음 금융위기가 닥치기 전에 국영기관(Crown)의 순자산과 공공 순부채를 합리적인 수준까지 회복시킬 계획을 세워야 한다. 이러한 조지들은 계속적인 지출증가를 억제한다는 것을 의미한다. 독립적으로 운영되는 재정위원회가 의회에 보고하는 것이 도움이 될 수 있다. 뉴질랜드의 외환보유고 상황이 검토될 수 있는데, 특히 금 보유고에 관해 그러한 검토가 필요할 수 있다. 준비은행은 긴급구제금융을 정상화하고 금리를 인상하는 명확한 계획을 가지고 있어야 한다.

뉴질랜드 정부가 덜 신중할수록 개인차원에서 뉴질랜드 국민 개개인은 더 신중해야 한다. 현재의 가격으로 부동산이나 주식을 매수하기 위해 무리하게 대출을 감행하는 것은 개인의 미래를 가지고 러시안룰렛 게임을 하는 것과 마찬가지로 위험하다. 포트폴리오를 분산투자해야 한다. 디플레이션과 인플레이션 문제가 발생할 가능성이 모두 존재한다.

New Zealand must prepare for the next global financial crisis

New Zealand’s economy suffered less damage from the pandemic than analysts expected.

But new research warns, however, that just as we are emerging from the COVID-19, a new crisis is already on the horizon.

Walking the path to the next global financial crisis highlights the danger of an economic crash which could see asset prices collapse, businesses fail, and KiwiSaver funds and investment portfolios destroyed. Recent homebuyers may find themselves owing more on their mortgage than their home is worth.

According to the report, governments’ and central banks’ responses to the Global Financial Crisis of 2008 laid the groundwork for the next financial crisis.

With zero interest rates and money printing, asset prices have soared, consumer prices have risen, and public debt has reached dangerous levels globally.

The world’s politicians and central bank governors are now struggling to return to more normal policies. The result is an economically perilous future.

Former Reserve Bank of New Zealand chair Arthur Grimes warns in the foreword to the report there may be only a short time before the next financial crisis. “Central bank actions through the pandemic … have placed New Zealand at greater risk of an asset price collapse with ensuing economic pain; the risk is heightened by the unsustainable fiscal and monetary policies globally,” Grimes writes.

The Government must prepare for the next global financial crisis, even though New Zealand is too small to prevent it. The prudent course is to reduce debt, both public and private.

The Covid-19 financial support package has kept Kiwis off of the dole queue and saved many businesses from bankruptcy. However, the government should promptly repay those debts in order to be prepared for the next financial shock.

Failing to prepare now for the next financial crisis could destroy New Zealanders’ nest eggs and threaten their livelihoods.