NZ Herald

Against the predictions of most economists early last year, the housing market has boomed through Covid-19. Since March last year, house prices have risen by 20%, rents by 12%. During the period, the economy suffered its worst-ever quarterly fall in GDP, and net migration has been virtually zero. Low-interest rates and limited land supply make a powerful combination.

But there is even more trouble on the horizon for housing. An ageing population results in declining average household sizes – this will add fuel to the housing fire. These demographic changes will be with us for decades, long after the Bitcoin becomes the primary global currency.

If you think the current housing circumstances are dire, wait till you see the potential long-run implications – you ain’t seen anything yet.

The housing crisis is a core supply problem. For decades, housing construction has not kept up with the growing population, which means house prices have gone through the roof.

Analysis by Infometrics shows more construction in a region slows down the rate of housing inflation. Auckland and Wellington’s stagnant building resulted in rapid inflation of 20% for the last decade. In comparison, Christchurch and Hamilton’s construction building surge resulted in prices increasing by only 13%.

Gross construction rates across New Zealand have increased substantially in recent times. According to Statistics New Zealand, residential completion numbers peaked at 38,624 in November 2020, the highest number since the 1970s.

This is great news, except that the population in the 1970s was 3 million and today it is 5.1 million. On a per-capita basis, we are nowhere near historical peaks. There were 13.2 new builds per thousand people in 1973, but only 7.6 per thousand people in 2020.

New Zealand’s housing construction rate is nowhere near adequate in proportion to population, let alone the long run effects of an ageing population.

The Initiative’s new report, ‘The Need to Build’, shows that long-term housing demand in New Zealand is set to rise as New Zealand’s population becomes larger and older, adding fuel to the ‘housing crisis’ fire.

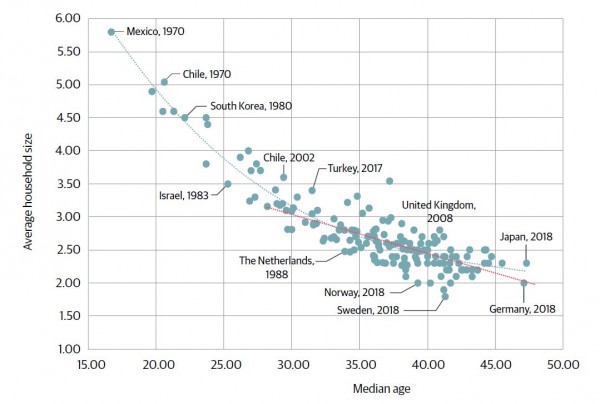

An older population results in fewer people living per dwelling and a larger population further increases housing needs. Across all the OECD countries, including New Zealand, the average household size has declined, which means more houses are needed per capita regardless of net migration levels.

In the report, we consider a range of housing for the period 2038 to 2060.

Under all the six most realistic scenarios, from 2019, we will need between 26,246 and 34,556 per year by 2038, and we will need between 15,319 and 29,052 additional dwellings per year by 2060.

The point is that cutting migration entirely would stop new housing demand – it does not because we still have an ageing population.

Even in extreme scenarios where net migration is zero for the next few decades, it does not stop new housing demand. By 2038, New Zealand would still need between 20,933 and 24,665 per year under medium life expectancy.

The report’s figures exclude the annual housing replacement rate, and the ongoing undersupply of 40,000 – estimated by Infometrics – adds to the chronic housing shortage.

What does all this mean for the outlook for housing in New Zealand?

The projected figures in the reports are well above the average annual construction rate of 21,445 since 1992. The implication is that house prices will rise a lot more unless house construction is much greater.

Fortunately, New Zealand is relatively young, with a median age of 37 years. Older countries across the OECD provide a window to the future. Kiwi policymakers have a unique opportunity to prepare what we can do now regarding housing policy.

In countries like Germany, the country is ageing, and the average household size has already been decreasing. Germany’s median age went from 37.6 in 1990 to 45.9 in 2020 and the average household size dropped from 2.3 to 2.0.

Since 1990, Germany’s population has been roughly stable at just above 80 million, but the household numbers went from 35 million in 1990 to 42 million in 2020 – 7 million more households in 30 years.

New Zealand is on a similar trajectory. New Zealand’s median age is currently close to 37 and is expected to increase to around 43 by 2038 and 50 by 2060. Our household size is also likely to drop from 2.6 to 2.4 by 2038 and even lower afterwards. The German illustration shows a potential image of New Zealand’s future, albeit with a far smaller total population size.

Even if annual construction increased closer to the 1970s, it would likely struggle to meet a more extensive and older population’s housing demand.

And estimating housing demand just on population growth is insufficient. On our projections, the dwelling stock in 2060 will be between 64% (‘low’ migration and ‘low’ fertility) and 26% (‘high’ migration and ‘high’ fertility), below what is needed to cater for the projected population need.

Tinkering the edges of demand will do little to address the chronic shortage in housing supply. Once the border opens, housing demand will continue to escalate, and the problem could become even worse.

All of this is fuel to the house fire, especially considering the revival of an open international economy after the global pandemic ends.

The housing crisis affects all Kiwis, but especially the millennials and Generation Z. There has been a growing intergenerational inequality preventing younger Kiwis from fulfilling their Kiwi Dream. The younger generation’s homeownership prospects are close to nil unless their parents are homeowners. Housing supply must expand substantially to give the younger generations a chance.